Instructions on Utilizing 14653

Completing Form 14653 is a crucial step in your journey towards compliance with U.S. tax obligations while residing outside the United States. This form requires detailed information about your tax situation, residency status, and reasons for any reporting failures. Ensure that you gather all necessary documents and information before you begin filling out the form.

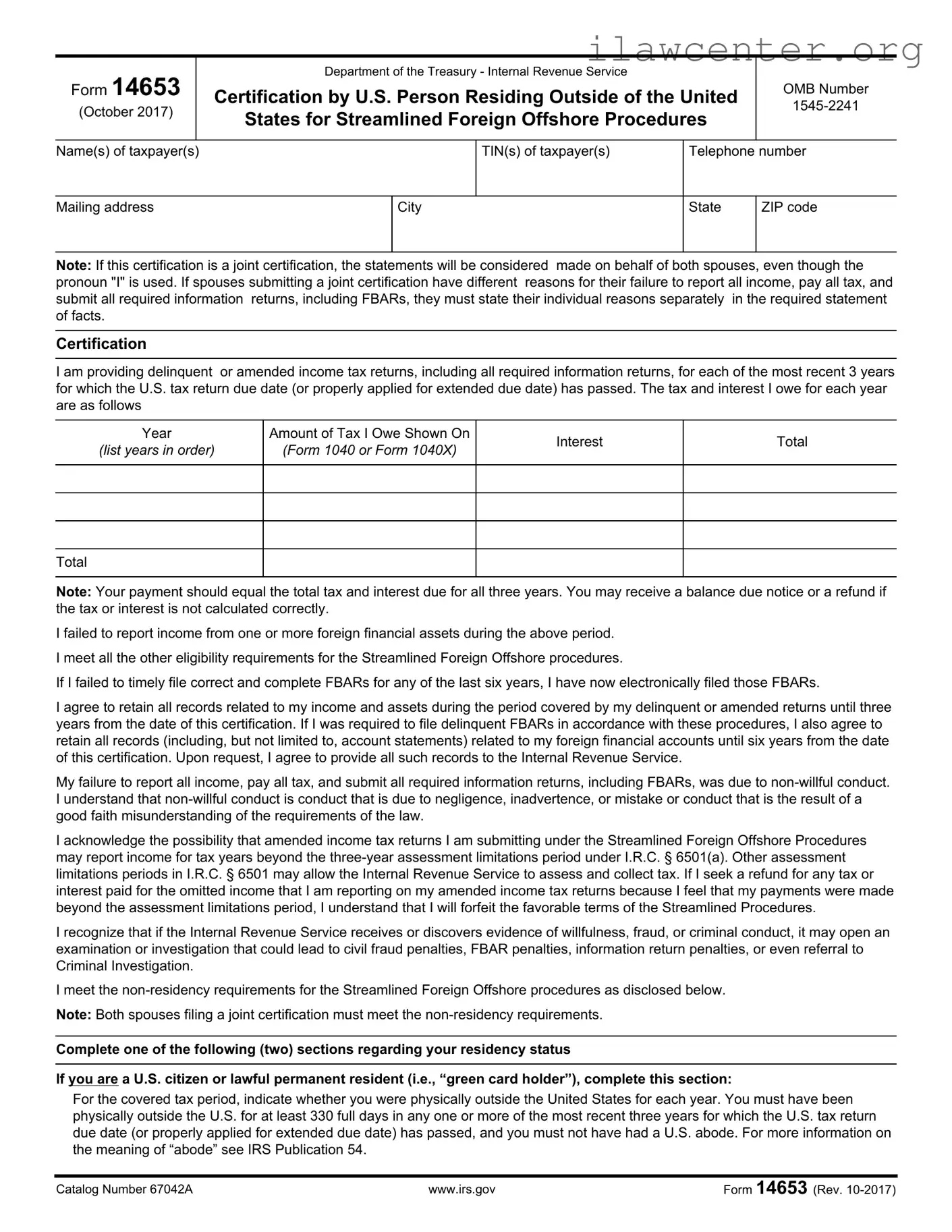

- Begin by entering your name(s) in the designated field for taxpayer(s).

- Provide your Tax Identification Number(s) (TIN) in the appropriate section.

- Fill in your telephone number and mailing address, including city, state, and ZIP code.

- If applicable, indicate whether this is a joint certification. If so, be aware that both spouses must provide individual reasons for any reporting failures.

- In the certification section, confirm that you are providing delinquent or amended income tax returns for the last three years.

- List the years for which you owe tax, along with the amount of tax owed, interest, and total for each year.

- Indicate whether you failed to report income from foreign financial assets and confirm your eligibility for the Streamlined Foreign Offshore procedures.

- Check the box to confirm that you have electronically filed any delinquent FBARs, if required.

- Acknowledge your agreement to retain all records related to your income and assets for the specified periods.

- State that your failure to report income and pay taxes was due to non-willful conduct.

- Complete the residency status section based on whether you are a U.S. citizen or lawful permanent resident, or not. Answer the questions about your physical presence in the U.S. for the past three years.

- Provide specific reasons for your failure to report all income and pay taxes. Include personal and financial background information.

- Detail the source of funds in your foreign financial accounts/assets and any relevant transactions.

- If you relied on a professional advisor, include their contact information and a summary of the advice received.

- Sign and date the form, ensuring all required signatures are included if it is a joint certification.

- If applicable, have your paid preparer complete their section, including their signature and contact information.

- Indicate if you want to allow another person to discuss this form with the IRS by providing their name and telephone number, if applicable.