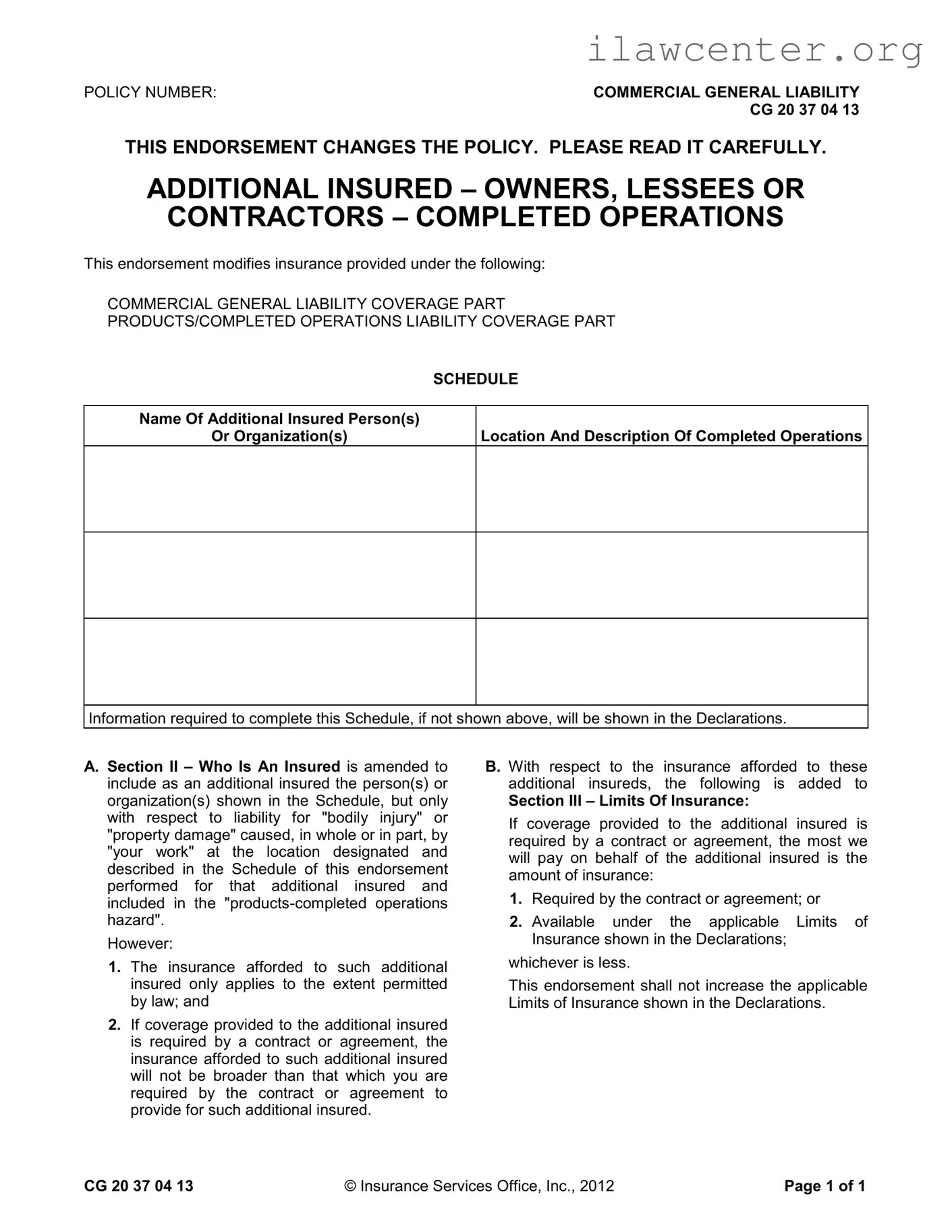

Instructions on Utilizing Additional Insured

Filling out the Additional Insured form is a straightforward process. This document ensures that specific individuals or organizations are covered under your insurance policy for certain liabilities. Follow the steps below to complete the form accurately.

- Locate the POLICY NUMBER section at the top of the form. Write down your policy number clearly.

- In the Name Of Additional Insured Person(s) Or Organization(s) section, provide the full name of the individual or organization you are adding as an additional insured.

- Next, fill in the Location And Description Of Completed Operations section. Be specific about the location and give a brief description of the operations completed for the additional insured.

- Review the information you entered to ensure accuracy. Double-check the spelling of names and details of the operations.

- Sign and date the form at the bottom. This indicates your agreement to the terms outlined in the endorsement.

- Submit the completed form to your insurance provider or the relevant party as instructed.