Instructions on Utilizing Business Credit Application

Filling out the Business Credit Application form is an important step in establishing a credit line for your business. Completing this form accurately will help facilitate the approval process, allowing you to access the financial resources you need. Follow these steps to ensure that you provide all necessary information clearly and concisely.

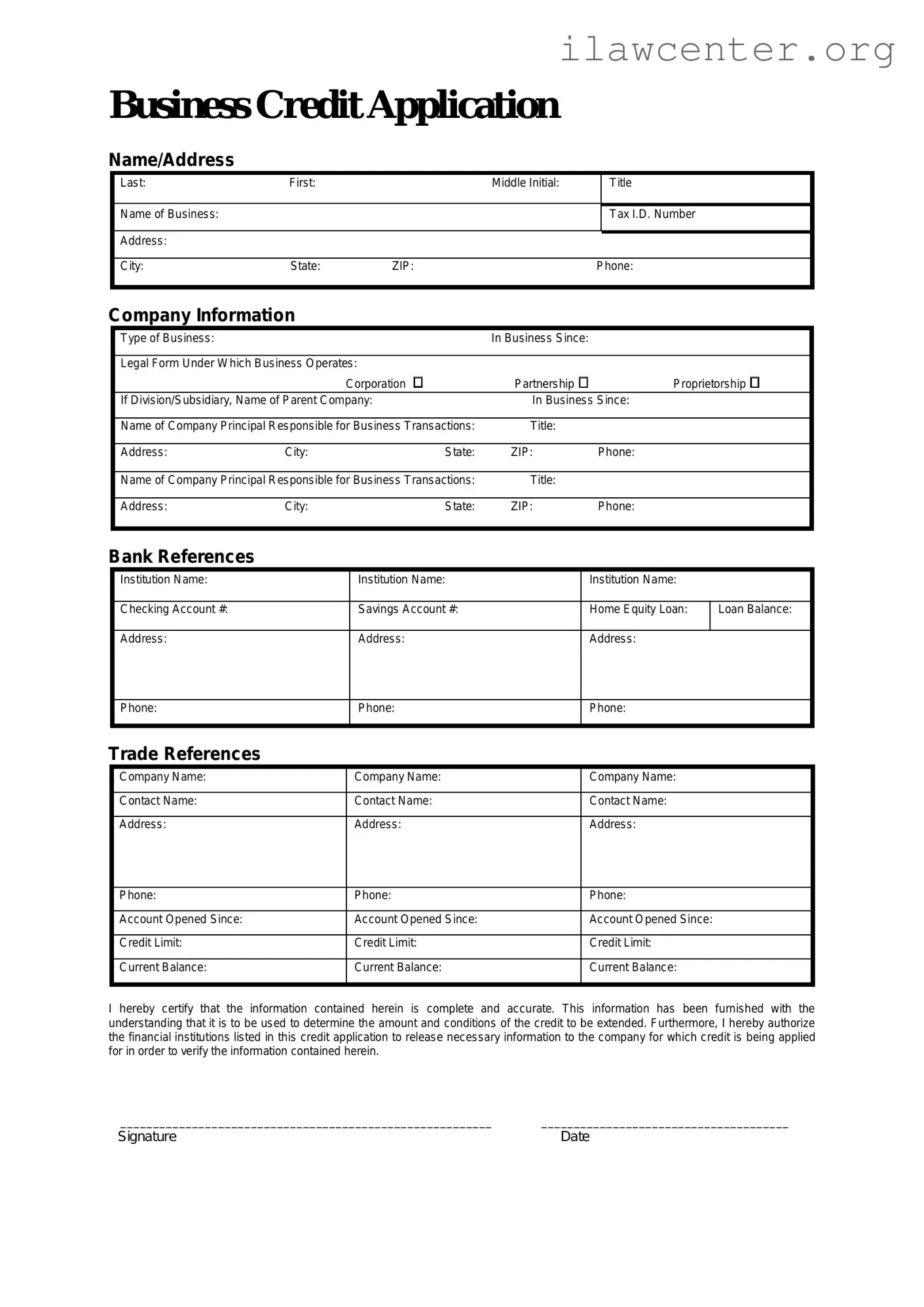

- Start with the basic information. Fill in your business name, address, and contact information. Make sure these details are correct to avoid any delays.

- Provide your business structure. Indicate whether your business is a sole proprietorship, partnership, corporation, or LLC.

- List your business tax ID number or Social Security number if applicable. This information is crucial for credit verification.

- Include the years in business. This helps lenders assess the stability and experience of your company.

- Detail your annual revenue. Provide an accurate estimate to give a clear picture of your business's financial health.

- Identify the primary business activity. Describe what your business does to help lenders understand your operations.

- List any previous credit relationships. Mention banks or financial institutions you have worked with in the past.

- Sign and date the application. Ensure that you are authorized to apply for credit on behalf of your business.

Once you have completed the form, review it for any errors or omissions. Submitting a well-prepared application can significantly improve your chances of obtaining the credit you seek.