What is the purpose of the Business Debt Schedule form?

The Business Debt Schedule form is designed to provide a clear overview of a company's outstanding debts. It includes details about loans, contracts, notes payable, and lines of credit. This form helps businesses track their financial obligations and can be essential for financial reporting, loan applications, or when seeking investors.

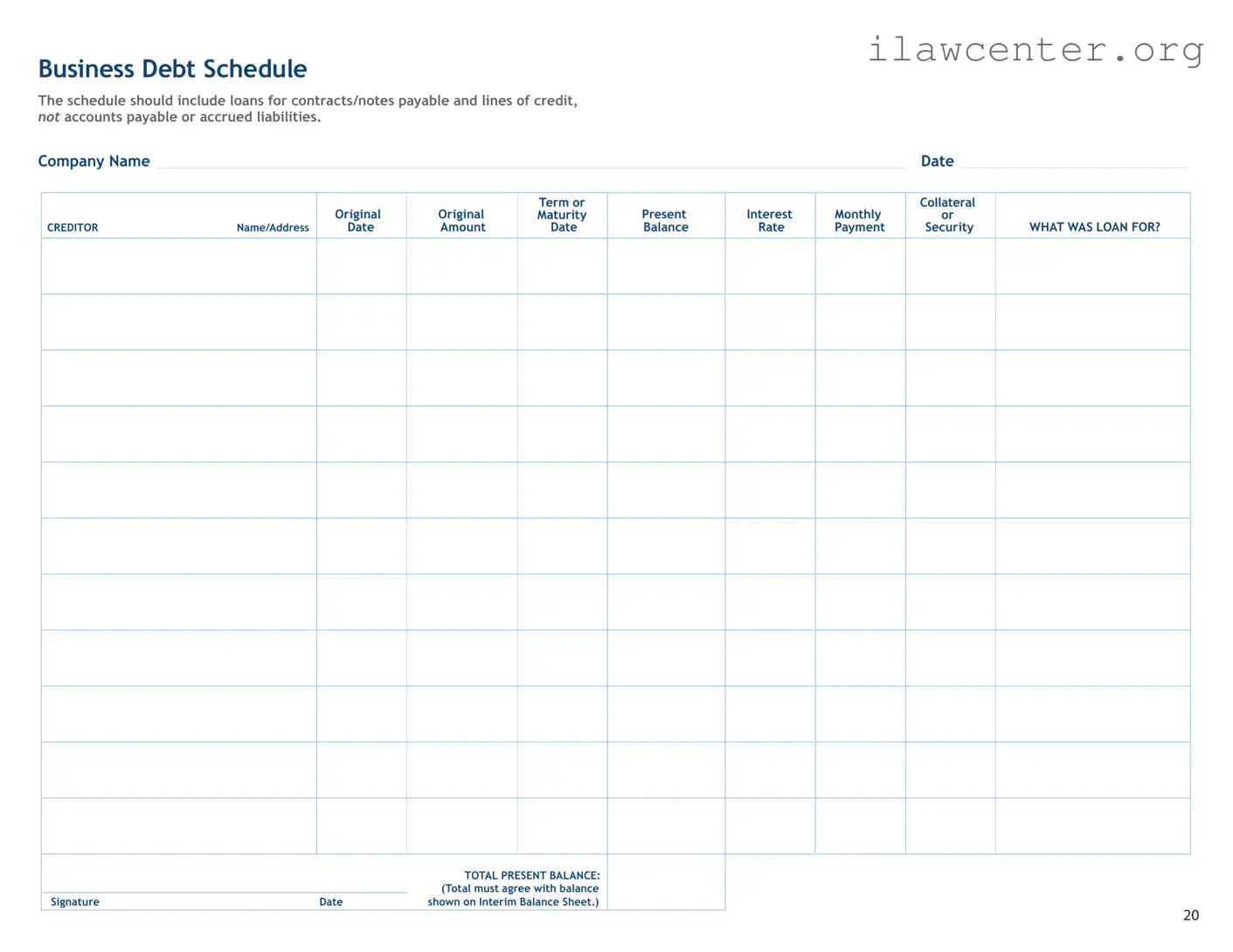

What types of debts should be included in the Business Debt Schedule?

The schedule should only include loans for contracts, notes payable, and lines of credit. It is important to note that accounts payable and accrued liabilities should not be included in this form. The focus is on formal loans and credit lines that require repayment.

What information is required for each creditor listed?

For each creditor, the form requires the following information: the creditor's name and address, the original date of the loan, the original amount borrowed, the term or maturity date, the present balance of the loan, the interest rate, the monthly payment amount, collateral or security associated with the loan, and a description of what the loan was used for. This comprehensive information helps in assessing the company's debt position.

How is the total present balance calculated?

The total present balance is the sum of all outstanding debts listed on the schedule. It is crucial that this total agrees with the balance shown on the interim balance sheet. Ensuring consistency between these documents is vital for accurate financial reporting.

Why is collateral or security information important?

Including collateral or security information is important because it indicates what assets are pledged against the loans. This information can affect the company’s creditworthiness and potential risk to lenders. It also provides transparency regarding the company's financial obligations and the assets at stake.

When should the Business Debt Schedule be updated?

The Business Debt Schedule should be updated regularly, particularly when new debts are incurred or existing debts are paid down. Regular updates ensure that the information remains accurate and reflects the current financial situation of the business. This practice is essential for effective financial management and planning.

Who is responsible for completing the Business Debt Schedule?

The responsibility for completing the Business Debt Schedule typically falls on the financial officer or accountant of the business. However, it can also involve collaboration with other team members who manage finances. Accurate completion of the form is crucial for maintaining a clear picture of the company's financial obligations.