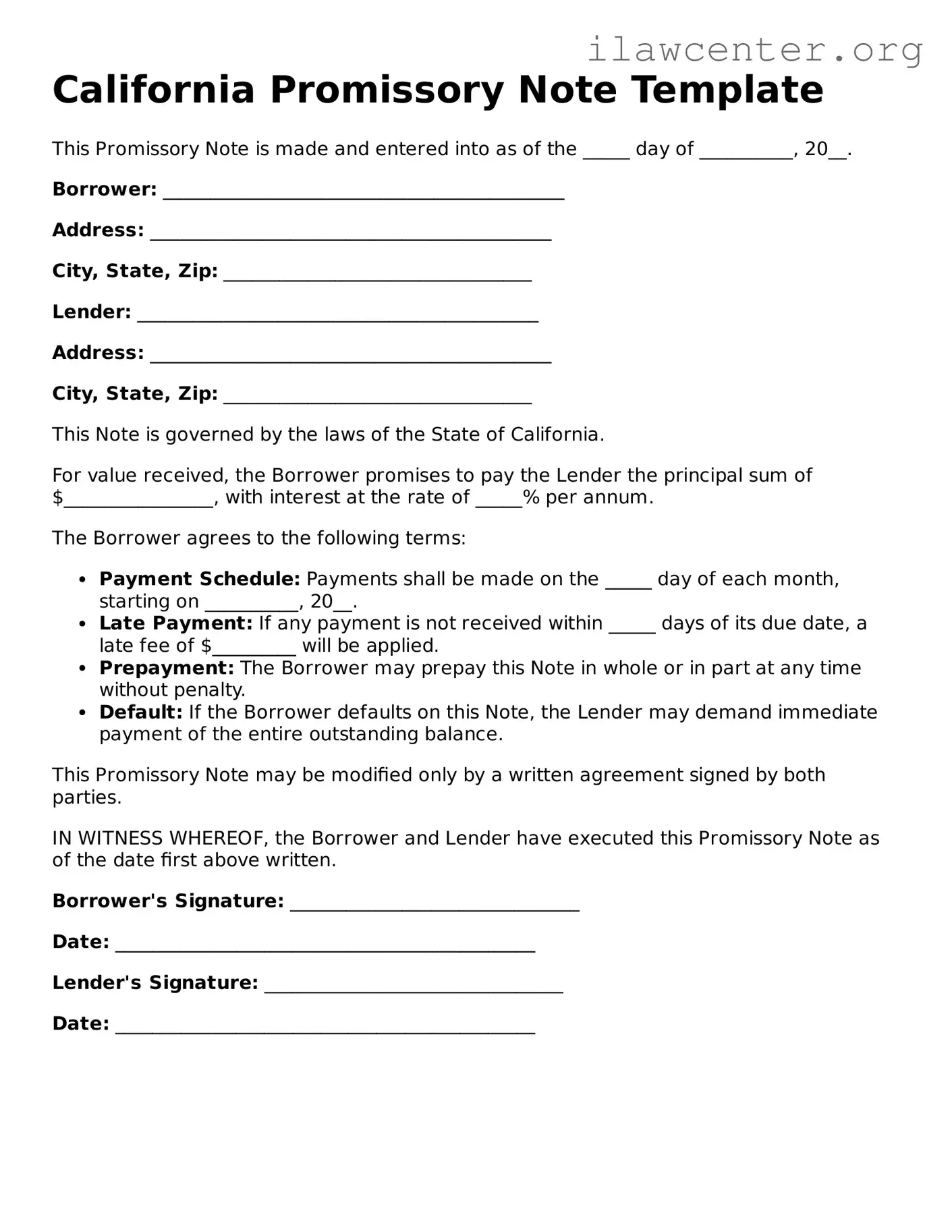

What is a California Promissory Note?

A California Promissory Note is a written agreement where one party promises to pay a specific amount of money to another party at a defined time or on demand. This document outlines the terms of the loan, including the interest rate, repayment schedule, and any penalties for late payment. It serves as a legal record of the debt and protects both the lender and borrower.

Who can use a Promissory Note in California?

Anyone can use a Promissory Note in California, whether you're an individual, a business, or an organization. It's commonly used in personal loans, business loans, or even informal agreements between friends and family. As long as the terms are clear and both parties agree, a Promissory Note can be a useful tool for managing financial transactions.

What are the essential components of a California Promissory Note?

A well-drafted Promissory Note should include the names and addresses of both the borrower and lender, the principal amount borrowed, the interest rate, repayment terms, and any additional terms such as late fees or prepayment options. It’s also important to include a signature line for both parties to sign, indicating their agreement to the terms.

Is a Promissory Note legally binding?

Yes, a Promissory Note is legally binding as long as it meets the necessary requirements of a contract. This includes mutual agreement, consideration (something of value exchanged), and the capacity of both parties to enter into a contract. If either party fails to uphold their end of the agreement, the other party may seek legal recourse.

Do I need a lawyer to create a Promissory Note?

While it’s not required to have a lawyer draft your Promissory Note, consulting with one can be beneficial, especially for larger loans or complex agreements. Many templates are available online, but a legal professional can ensure that your document meets all legal requirements and adequately protects your interests.

Can a Promissory Note be modified after it’s signed?

Yes, a Promissory Note can be modified, but both parties must agree to the changes. It’s advisable to document any modifications in writing and have both parties sign the revised agreement. This helps avoid misunderstandings and ensures that everyone is on the same page regarding the new terms.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, meaning they fail to make payments as agreed, the lender has several options. They can attempt to collect the debt through negotiation, hire a collection agency, or take legal action. The terms outlined in the Promissory Note will guide the lender on how to proceed in the event of a default.

Is a Promissory Note the same as a loan agreement?

While both documents serve similar purposes, they are not the same. A Promissory Note is a simple promise to pay back a loan, whereas a loan agreement is a more detailed contract that may include additional terms and conditions, such as collateral, warranties, and obligations of both parties. Depending on your needs, you may choose one over the other or use both together.