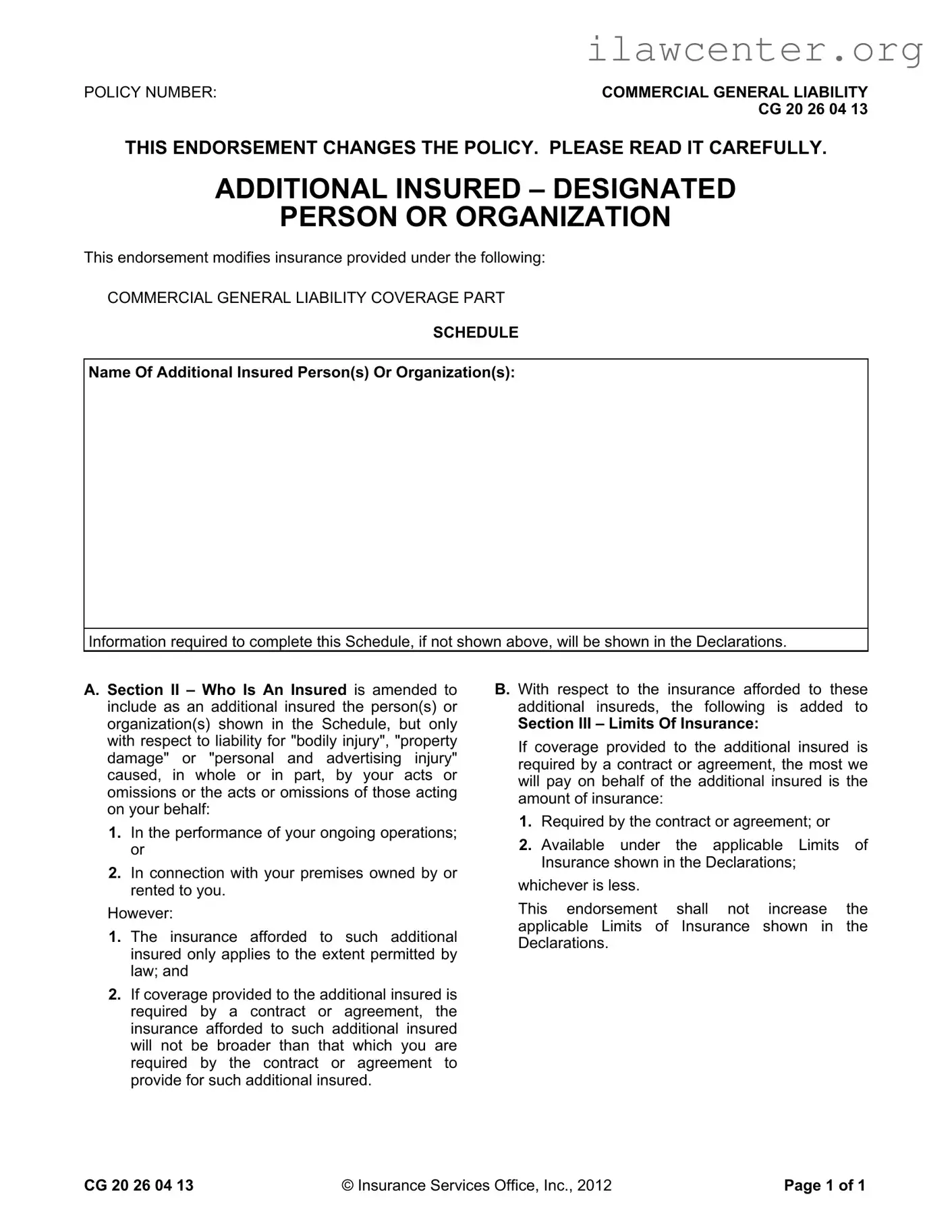

Instructions on Utilizing Cg 20 26 04 13

After you have gathered the necessary information, you can begin filling out the Cg 20 26 04 13 form. This form is essential for adding an additional insured to your commercial general liability policy. Follow these steps carefully to ensure that all required information is accurately provided.

- Locate the form titled "CG 20 26 04 13". Ensure you have the most current version.

- Fill in the Policy Number at the top of the form. This number is usually found on your insurance documents.

- In the section labeled Name Of Additional Insured Person(s) Or Organization(s), write the full name of the individual or organization you wish to add as an additional insured.

- If the name of the additional insured is not already shown in the Declarations, ensure you provide any necessary details that may be required.

- Review the information you have entered for accuracy. Make sure there are no spelling errors or omissions.

- Sign and date the form at the bottom. This indicates that you have completed the form and agree to its terms.

- Submit the completed form to your insurance provider according to their instructions. Keep a copy for your records.

Once you have submitted the form, your insurance provider will process the request. You should receive confirmation once the additional insured has been added to your policy. It’s important to follow up if you do not receive confirmation within a reasonable time frame.