_________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________

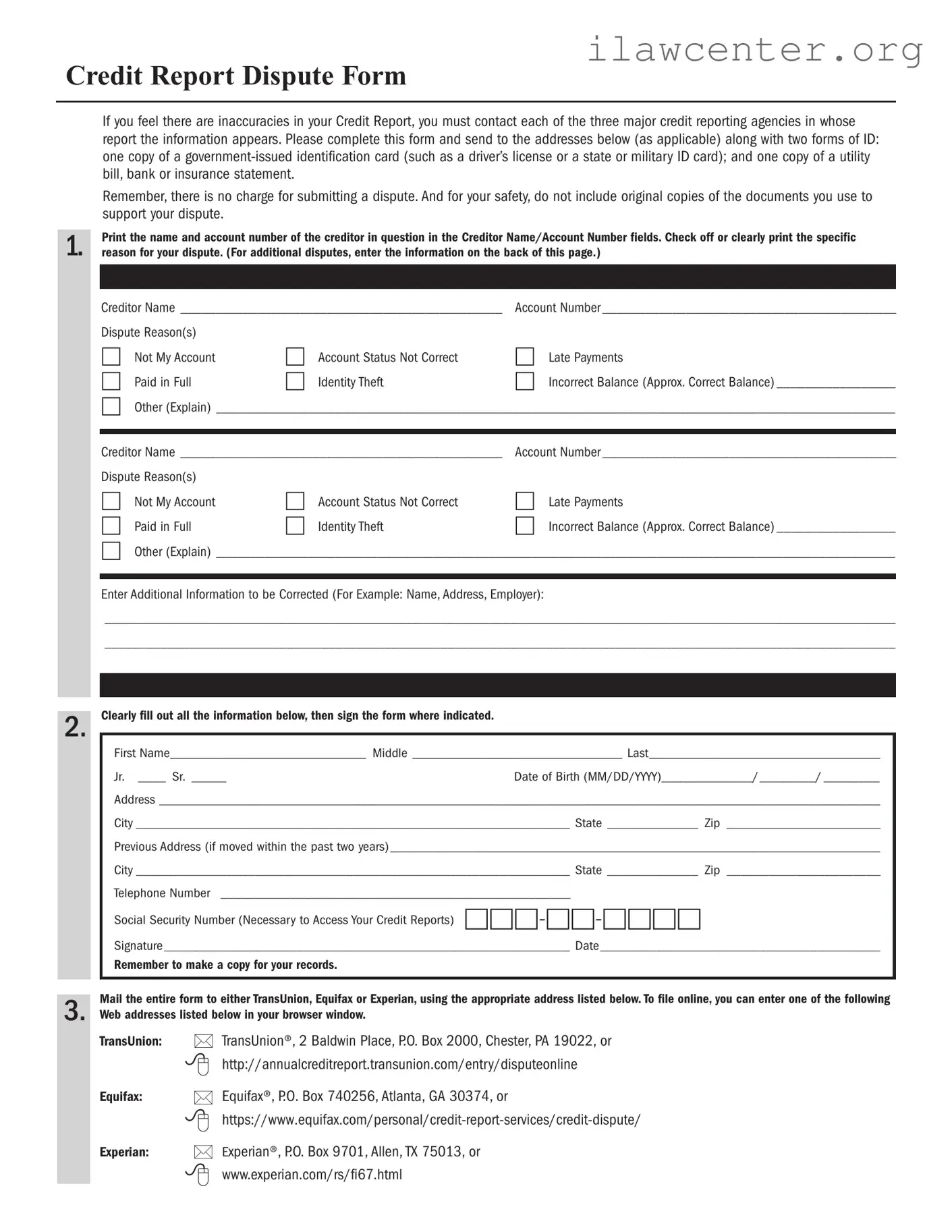

Credit Report Dispute Form

If you feel there are inaccuracies in your Credit Report, you must contact each of the three major credit reporting agencies in whose

report the information appears. Please complete this form and send to the addresses below (as applicable) along with two forms of ID:

one copy of a government-issued identification card (such as a driver’s license or a state or military ID card); and one copy of a utility

bill, bank or insurance statement.

Remember, there is no charge for submitting a dispute. And for your safety, do not include original copies of the documents you use to

support your dispute.

1.

Print the name and account number of the creditor in question in the Creditor Name/Account Number fields. Check off or clearly print the specific

reason for your dispute. (For additional disputes, enter the information on the back of this page.)

Creditor Name ______________________________________________ Account Number __________________________________________

Dispute Reason(s)

□ Not My Account □ Account Status Not Correct □ Late Payments

□ Paid in Full □ Identity Theft □ Incorrect Balance (Approx. Correct Balance) _________________

□ Other (Explain) _________________________________________________________________________________________________

Creditor Name ______________________________________________ Account Number __________________________________________

Dispute Reason(s)

□ Not My Account □ Account Status Not Correct □ Late Payments

□ Paid in Full □ Identity Theft □ Incorrect Balance (Approx. Correct Balance) _________________

□ Other (Explain) _________________________________________________________________________________________________

Enter Additional Information to be Corrected (For Example: Name, Address, Employer):

Clearly fill out all the information below, then sign the form where indicated.

2.

First Name____________________________ Middle ______________________________ Last_________________________________

Jr. ____ Sr. _____ Date of Birth (MM/DD/YYYY)_____________/________/ ________

Address _______________________________________________________________________________________________________

City ______________________________________________________________ State _____________ Zip ______________________

Previous Address (if moved within the past two years)______________________________________________________________________

City ______________________________________________________________ State _____________ Zip ______________________

Telephone Number __________________________________________________

Social Security Number (Necessary to Access Your Credit Reports)

□□□-□□-□□□□

Signature__________________________________________________________ Date________________________________________

Remember to make a copy for your records.

Mail the entire form to either TransUnion, Equifax or Experian, using the appropriate address listed below. To file online, you can enter one of the following

3.

Web addresses listed below in your browser window.

TransUnion:

TransUnion®, 2 Baldwin Place, P.O. Box 2000, Chester, PA 19022, or

http://annualcreditreport.transunion.com/entry/disputeonline

Equifax:

Equifax®, P.O. Box 740256, Atlanta, GA 30374, or

https://www.equifax.com/personal/credit-report-services/credit-dispute/

Experian:

Experian®, P.O. Box 9701, Allen, TX 75013, or

www.experian.com/rs/fi67.html