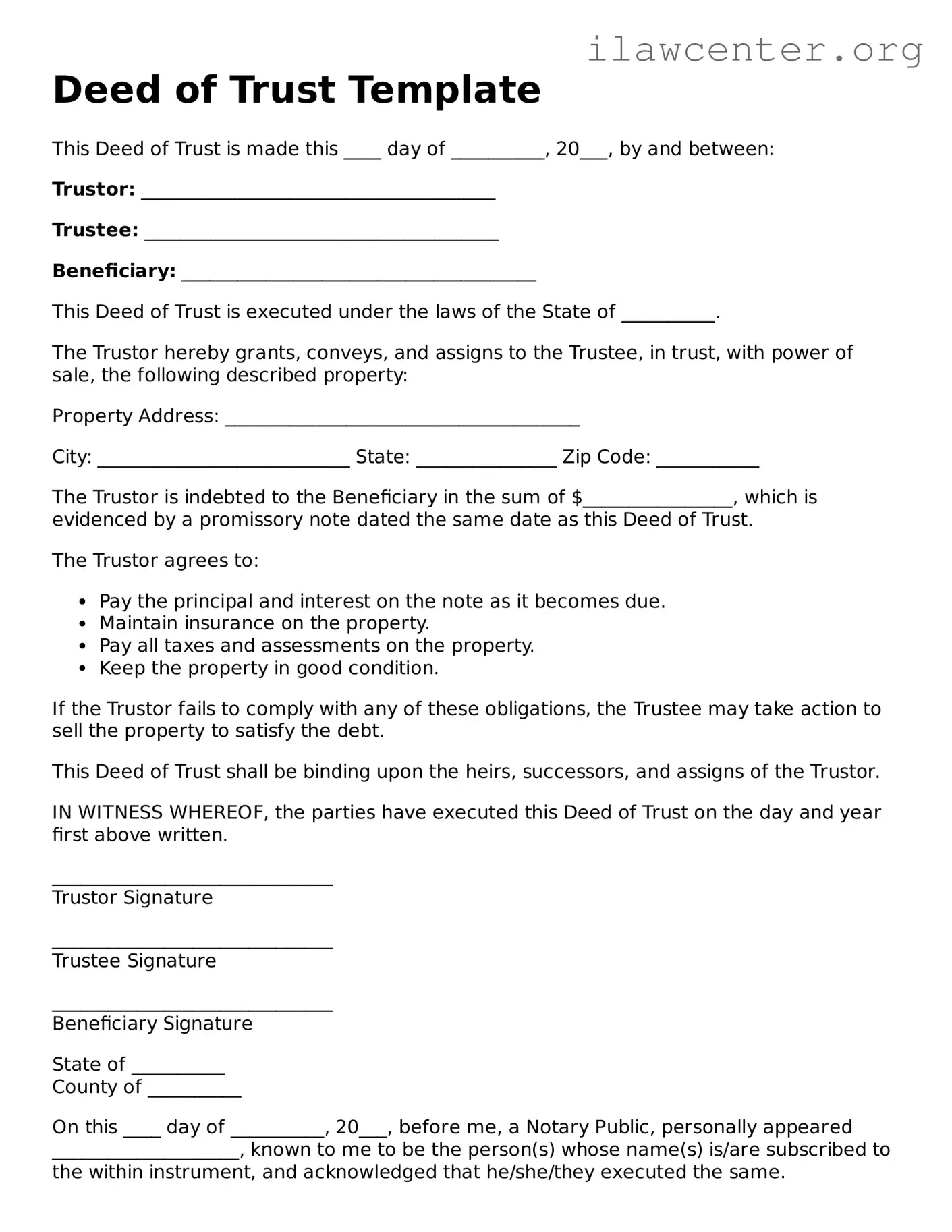

What is a Deed of Trust?

A Deed of Trust is a legal document used in real estate transactions. It secures a loan by transferring the title of the property to a third party, known as a trustee, until the borrower repays the loan. This arrangement protects the lender's interest in the property while allowing the borrower to maintain possession and use of it.

Who are the parties involved in a Deed of Trust?

There are typically three parties involved: the borrower (also known as the trustor), the lender (beneficiary), and the trustee. The borrower receives the loan, the lender provides the funds, and the trustee holds the title to the property until the loan is fully paid off.

How does a Deed of Trust differ from a mortgage?

While both a Deed of Trust and a mortgage serve the same purpose of securing a loan, they differ in structure. A mortgage involves two parties—the borrower and the lender. In contrast, a Deed of Trust involves three parties and places the title with a trustee, which can simplify the foreclosure process if the borrower defaults.

What happens if the borrower defaults on the loan?

If the borrower fails to make payments, the lender can initiate foreclosure proceedings. In a Deed of Trust, the trustee can sell the property without going through the court system, making the process generally faster than with a mortgage. The proceeds from the sale go to pay off the loan balance.

Is a Deed of Trust recorded?

Yes, a Deed of Trust is typically recorded in the county where the property is located. Recording the document provides public notice of the lender's interest in the property and helps establish the priority of claims against the property in case of default.

Can a Deed of Trust be modified?

Yes, a Deed of Trust can be modified, but both the lender and borrower must agree to the changes. This might involve altering the loan terms, such as the interest rate or payment schedule. A written amendment should be executed to document any modifications.

What are the benefits of using a Deed of Trust?

A Deed of Trust offers several benefits. It can streamline the foreclosure process, providing quicker resolution for lenders. For borrowers, it can allow for more flexible terms. Additionally, it can provide a clear legal framework for both parties, reducing potential disputes.

Do I need a lawyer to create a Deed of Trust?

While it is not strictly necessary to have a lawyer draft a Deed of Trust, it is highly recommended. Legal professionals can ensure that the document complies with state laws and accurately reflects the intentions of both parties, reducing the risk of future complications.