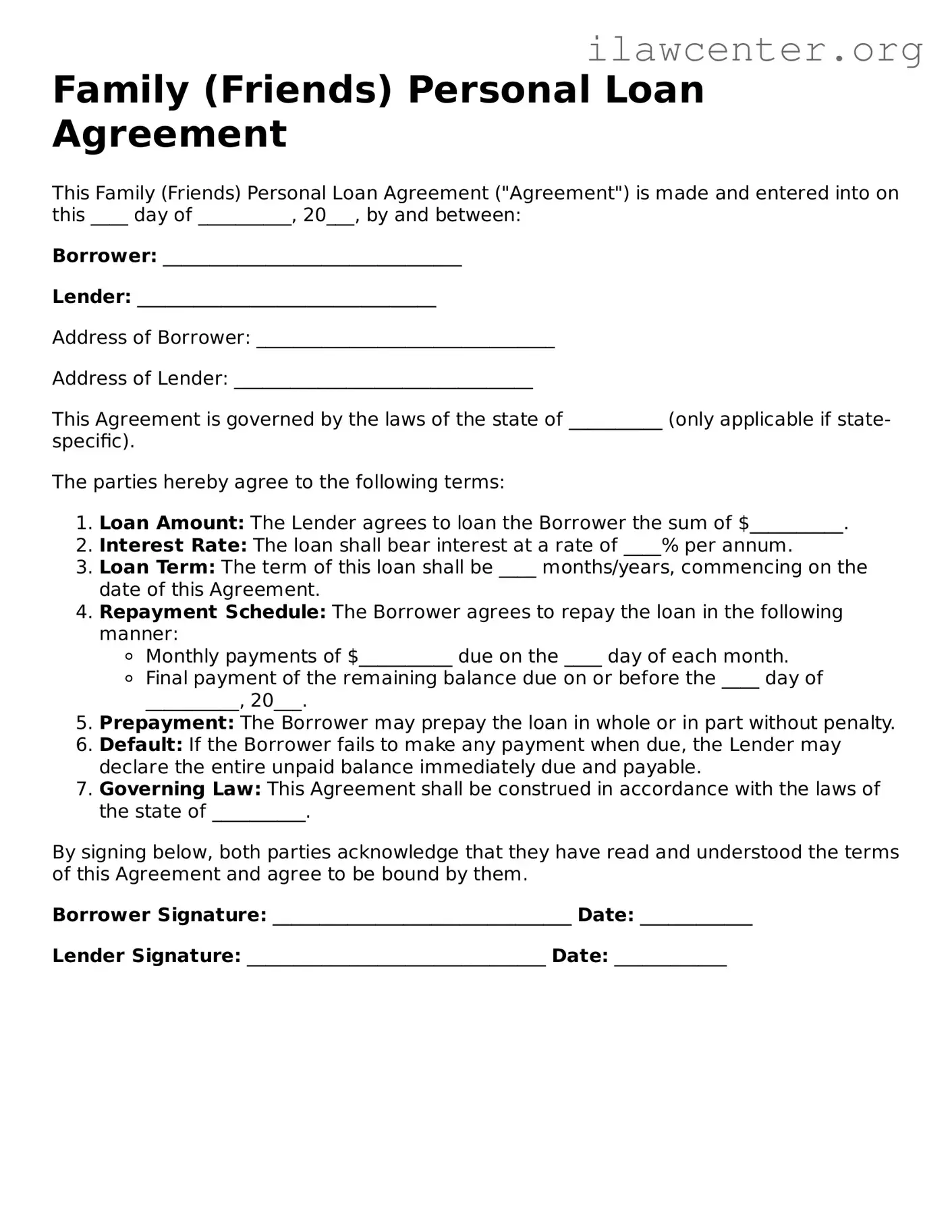

What is a Family (Friends) Personal Loan Agreement?

A Family (Friends) Personal Loan Agreement is a written document that outlines the terms of a loan made between family members or friends. It serves to clarify the expectations of both the lender and the borrower, helping to prevent misunderstandings and potential conflicts in the future.

Why should I use a written agreement for a personal loan?

Using a written agreement provides a clear record of the loan terms, including the amount borrowed, interest rates, repayment schedule, and any other conditions. This can help protect both parties and provide legal recourse if issues arise. It also reinforces the seriousness of the transaction, even when dealing with loved ones.

What key elements should be included in the agreement?

The agreement should include the loan amount, interest rate (if applicable), repayment schedule, and due dates. Additionally, it should specify what happens in case of default, any collateral involved, and any fees or penalties. Both parties should sign and date the document to make it official.

Can I charge interest on a personal loan to family or friends?

Yes, you can charge interest on a personal loan. However, it’s essential to ensure that the interest rate complies with state usury laws, which regulate the maximum interest rates that can be charged. Charging a fair interest rate can help cover inflation and make the loan more formal.

What happens if the borrower cannot repay the loan?

If the borrower cannot repay the loan, the agreement should outline the consequences. This might include a grace period, renegotiation of terms, or even legal action if necessary. It’s crucial to discuss these scenarios upfront to avoid tension later on.

Is it necessary to notarize the agreement?

While notarization is not required for a personal loan agreement to be valid, it can add an extra layer of security. Having the agreement notarized can help prove its authenticity and may be beneficial if disputes arise in the future.

Can the terms of the loan be modified after the agreement is signed?

Yes, the terms can be modified, but any changes should be documented in writing and signed by both parties. This helps maintain clarity and ensures that both the lender and borrower are on the same page regarding the new terms.

What should I do if there is a dispute regarding the loan?

If a dispute arises, it’s best to address it directly and calmly with the other party. Review the agreement together to clarify misunderstandings. If the issue cannot be resolved amicably, consider mediation or legal advice as a last resort.

Can I use this agreement for loans between non-family members?

While the Family (Friends) Personal Loan Agreement is designed for loans between family and friends, it can be adapted for use between non-family members. However, it’s wise to ensure that both parties are comfortable with the terms and that the agreement reflects the nature of the relationship.

Where can I find a template for a Family (Friends) Personal Loan Agreement?

Templates for Family (Friends) Personal Loan Agreements can be found online through legal websites, or you can consult with a legal professional to create a customized agreement that meets your specific needs. Always ensure that the template complies with your state’s laws.