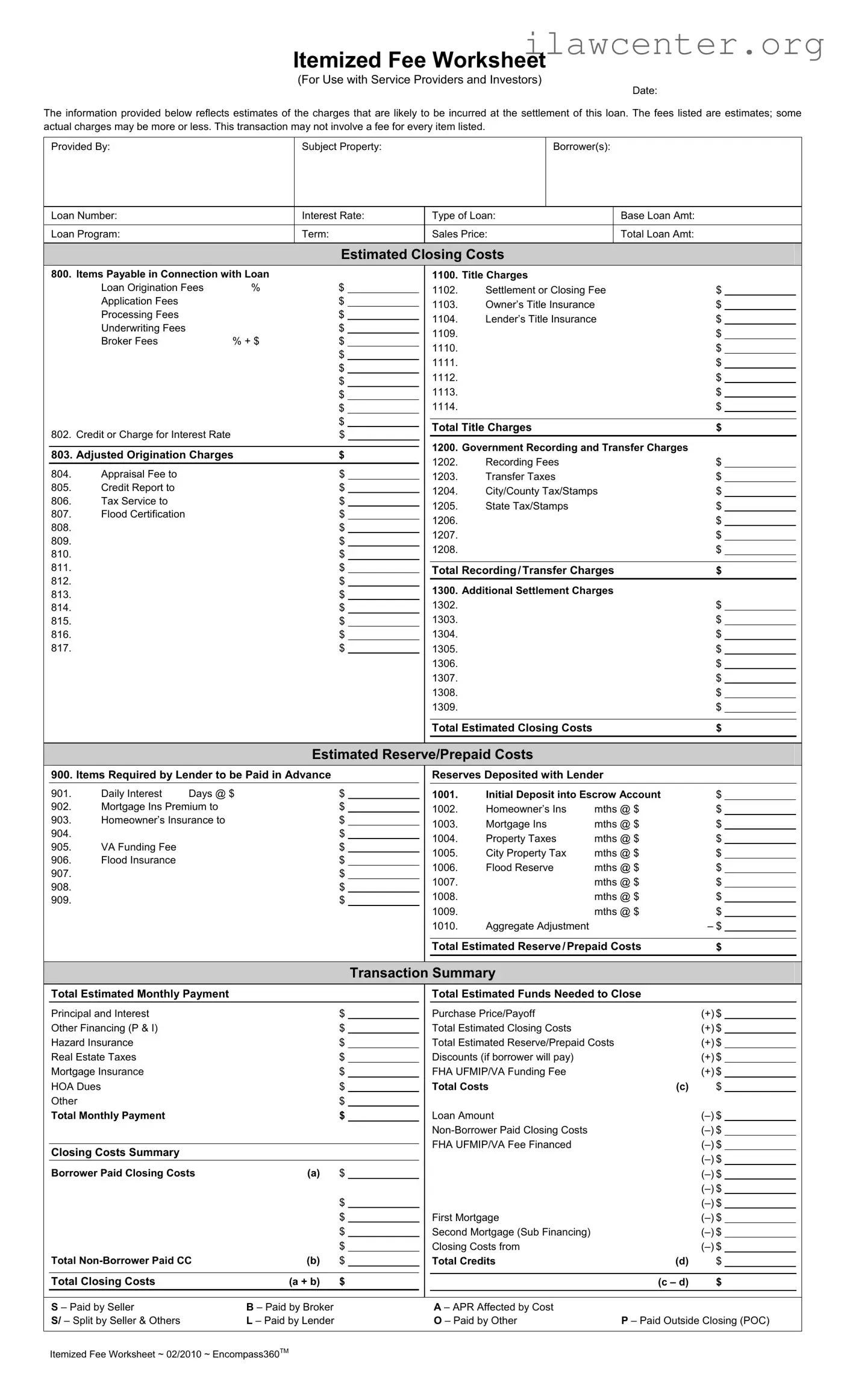

Instructions on Utilizing Fee Worksheet

Filling out the Fee Worksheet form accurately is essential for understanding the costs associated with your loan. This guide provides clear steps to help you complete the form efficiently.

- Enter the Date: Write the date when you are completing the form at the top.

- Fill in Provided By: Include the name of the person or organization providing the worksheet.

- Subject Property: Write the address of the property involved in the loan.

- Borrower(s): List the names of all borrowers on the loan.

- Loan Number: Enter the specific loan number assigned to this transaction.

- Interest Rate: Fill in the interest rate for the loan.

- Type of Loan: Specify the type of loan you are applying for.

- Base Loan Amount: Enter the total amount of the loan before any fees.

- Loan Program: Indicate the loan program you are using.

- Term: Write the term length of the loan (e.g., 15 years, 30 years).

- Sales Price: Enter the sales price of the property.

- Total Loan Amount: Calculate and write the total loan amount.

- Estimated Closing Costs: Fill in the estimated closing costs based on the provided categories.

- Items Payable in Connection with Loan: List all applicable fees, including loan origination fees, title charges, and any other costs.

- Estimated Reserve/Prepaid Costs: Include any costs required by the lender to be paid in advance.

- Transaction Summary: Summarize the total estimated monthly payment and funds needed to close.

After completing the Fee Worksheet, review all entries for accuracy. This will ensure a smooth process moving forward. Make sure to keep a copy for your records and submit it as required.