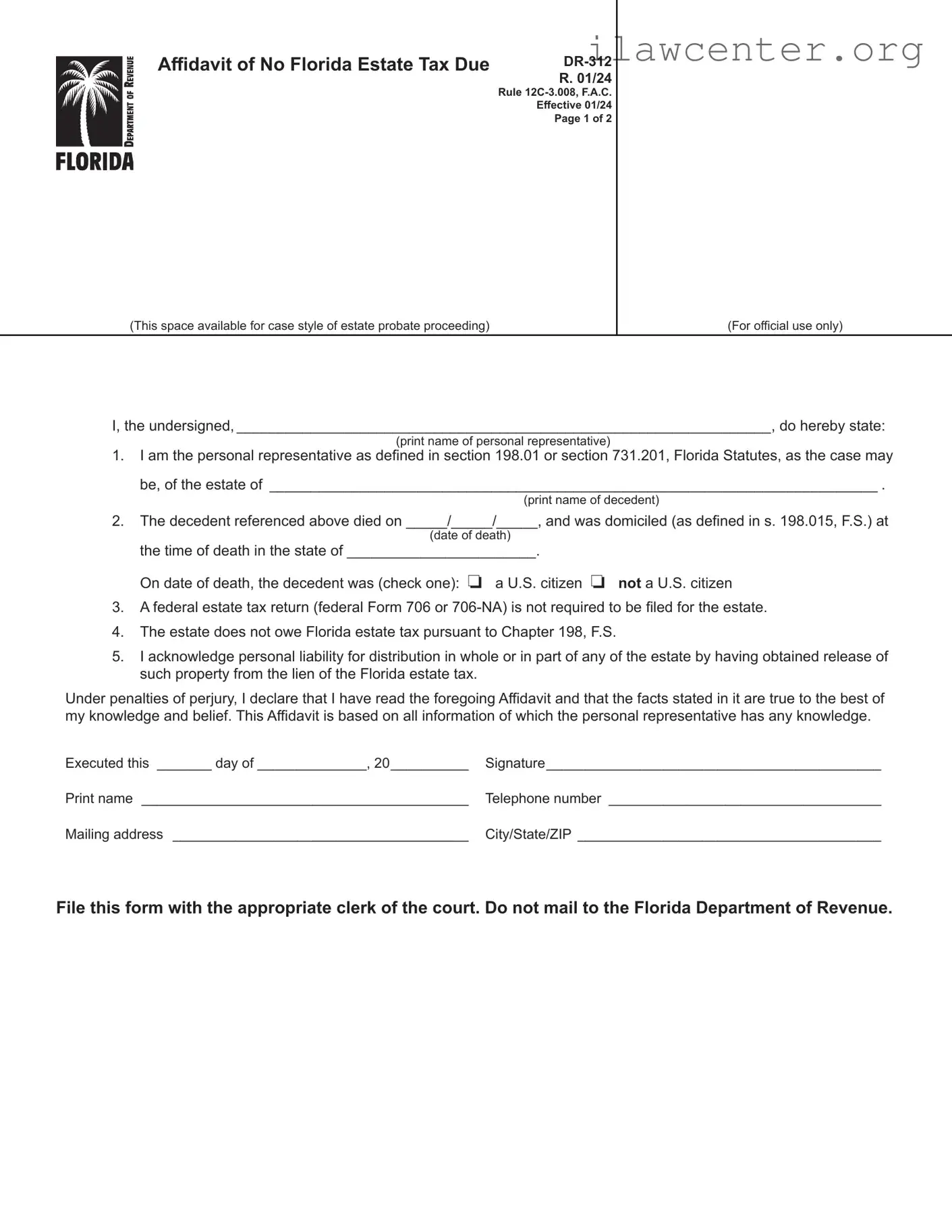

Instructions for Completing Form DR-312

File this form with the appropriate clerk of the court if necessary. Do not mail to the Florida Department

of Revenue.

DR-312

R. 01/24

Page 2 of 2

General Information

If Florida estate tax is not due and a federal estate tax

return (federal Form 706 or 706-NA) is not required to be

led, the personal representatives of such estates may

complete Florida Form DR-312, Adavit of No Florida

Estate Tax Due. Note that the denition of “personal

representative” in Chapter 198, F.S., includes any

person who is in actual or constructive possession.

Therefore, this adavit may be used by “persons

in possession” of any property included in the

decedent’s gross estate.

Form DR-312 is admissible as evidence of nonliability

for Florida estate tax and will remove the Department’s

estate tax lien. The Florida Department of Revenue will

not issue Nontaxable Certicates for estates for which

the DR-312 has been duly led and no federal Form 706

or 706-NA is due.

The 3-inch by 3-inch space in the upper right corner of

the form is for the exclusive use of the clerk of the court.

Do not write, mark, or stamp in that space.

Where to File Form DR-312

Form DR-312 may be recorded directly with the clerk

of the circuit court in the county or counties where the

decedent owned property. Do not send this form to the

Florida Department of Revenue.

When to Use Form DR-312

Form DR-312 should be used when an estate is not

subject to Florida estate tax under Chapter 198, F.S., a

federal estate tax return (federal Form 706 or

706-NA) is not required to be led, and the

administrative proceedings commenced before

July 1, 2023.

NOTE: This form may NOT be used for estates that are

required to le federal form 706 or 706-NA.

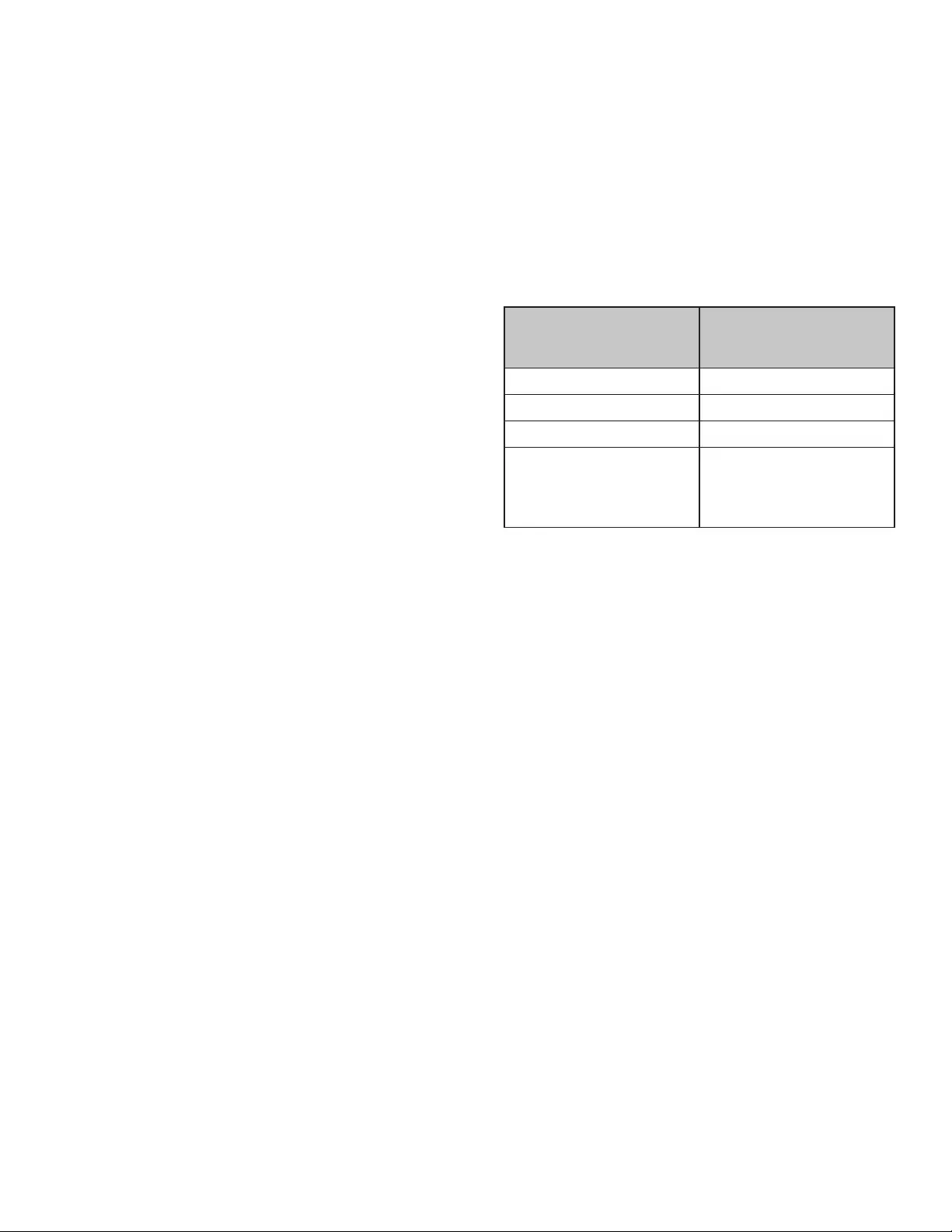

Federal thresholds for ling federal Form 706 only:

(For informational purposes only. Please conrm with

Form 706 instructions.)

Date of Death

(year)

Dollar Threshold

for Filing Form 706

(value of gross estate)

2000 and 2001 $675,000

2002 and 2003 $1,000,000

2004 and 2005 $1,500,000

For 2006 and forward

go to the IRS website at

www.irs.gov to obtain

thresholds.

For thresholds for ling federal Form 706-NA

(nonresident alien decedent), contact your local Internal

Revenue Service oce.

If an administration proceeding which commenced

before July 1, 2023 is pending for an estate, Form

DR-312 may be led in that proceeding. The case style

of the proceeding should be added in the large blank

space in the upper left portion of the DR-312. Form

DR-312 should be led with the clerk of the court and

duly recorded in the public records of the county or

counties where the decedent owned property.

Contact Us

Information and tutorials are available at oridarevenue.com/taxes/education.

Tax forms and brochures are available at oridarevenue.com/forms.

To speak with a Department of Revenue representative, call Taxpayer Services at 850-488-6800, Monday through

Friday, excluding holidays.

Reference Material

Rules are available at rules.org.

Rule Chapter 12C-3, Florida Administrative Code and Chapter 198, Florida Statutes.

Subscribe to Receive Email Alerts from the Department.

Subscribe to receive an email for ling due date reminders, Tax Information Publications (TIPs), or proposed rules.

Subscribe today at oridarevenue.com/dor/subscribe.