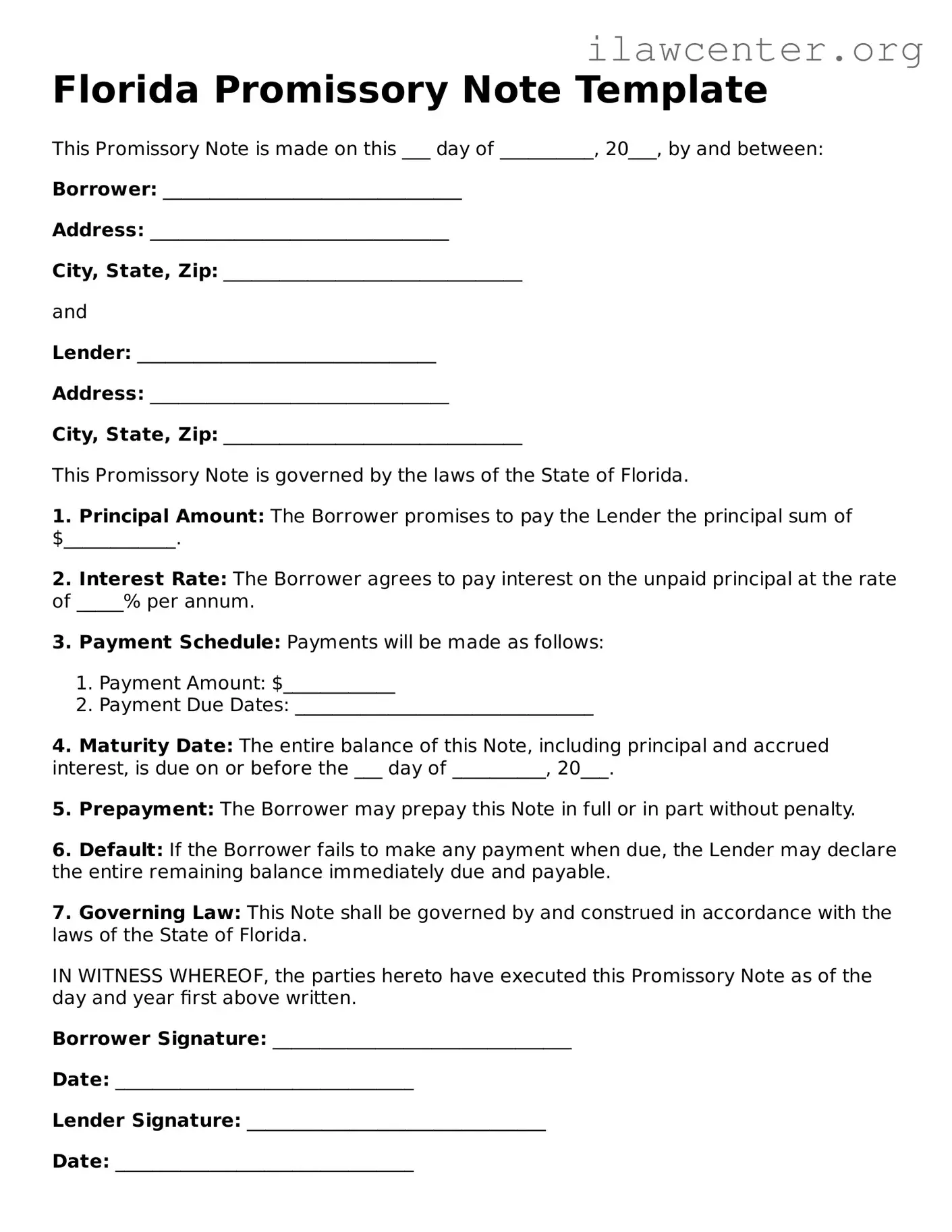

What is a Florida Promissory Note?

A Florida Promissory Note is a legal document that outlines a borrower's promise to repay a specified amount of money to a lender under agreed-upon terms. It serves as a written acknowledgment of the debt and includes details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments.

Who can use a Florida Promissory Note?

Anyone can use a Florida Promissory Note, including individuals, businesses, and organizations. It is commonly used for personal loans, business financing, or any situation where one party lends money to another and wants a formal agreement in place.

What information is typically included in a Florida Promissory Note?

A typical Florida Promissory Note includes the names and addresses of the borrower and lender, the loan amount, interest rate, repayment terms, due dates, and any collateral involved. It may also specify what happens in the event of default, such as late fees or legal action.

Is a Florida Promissory Note legally binding?

Yes, a Florida Promissory Note is legally binding as long as it meets certain requirements. Both parties must agree to the terms, and the document should be signed and dated. It’s advisable to have witnesses or notarization to strengthen its enforceability.

Can a Florida Promissory Note be modified?

Yes, a Florida Promissory Note can be modified if both parties agree to the changes. It’s best to document any modifications in writing and have both parties sign the amended agreement to avoid disputes later.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, the lender has the right to take legal action to recover the owed amount. This may include filing a lawsuit or pursuing collection efforts. The specific remedies available will depend on the terms outlined in the Promissory Note.

Is it necessary to have a lawyer draft a Florida Promissory Note?

While it is not strictly necessary to have a lawyer draft a Florida Promissory Note, doing so can help ensure that the document complies with state laws and adequately protects both parties' interests. Consulting with a legal professional is recommended, especially for larger loans or complex situations.

Can a Florida Promissory Note be used for business loans?

Yes, a Florida Promissory Note can be used for business loans. It can formalize the terms of the loan between business partners, investors, or financial institutions. Clear terms help prevent misunderstandings and provide a legal framework for repayment.

Are there any specific state laws governing Florida Promissory Notes?

Florida law does govern Promissory Notes, particularly regarding interest rates, default procedures, and enforcement. It’s important to be aware of these laws to ensure compliance and avoid potential legal issues.

Where can I find a template for a Florida Promissory Note?

Templates for Florida Promissory Notes can be found online through legal document services, or you can consult a legal professional who can provide a customized template tailored to your specific needs.