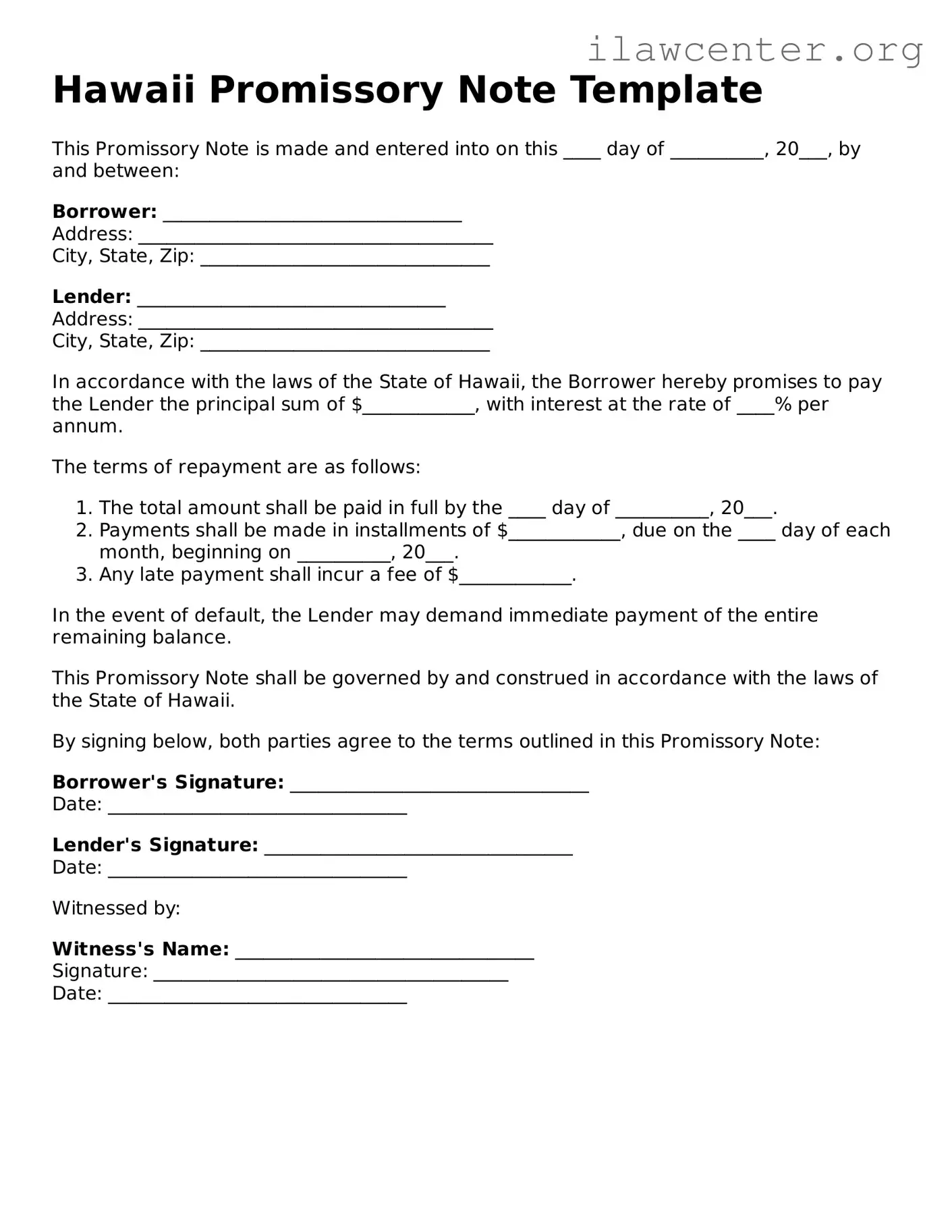

What is a Hawaii Promissory Note?

A Hawaii Promissory Note is a legal document that outlines a borrower's promise to repay a loan to a lender. It specifies the amount borrowed, the interest rate, repayment schedule, and any other terms agreed upon by both parties. This document serves as evidence of the debt and can be enforced in a court of law if necessary.

Who can use a Promissory Note in Hawaii?

Any individual or business in Hawaii can use a Promissory Note. It is commonly used in personal loans, business loans, or real estate transactions. Both lenders and borrowers should ensure they understand the terms outlined in the document before signing.

What are the essential components of a Hawaii Promissory Note?

A comprehensive Promissory Note typically includes the names and addresses of the borrower and lender, the principal amount, interest rate, repayment terms, due dates, and any late fees. It may also contain clauses regarding prepayment, default, and governing law.

Is a Promissory Note legally binding in Hawaii?

Yes, a properly executed Promissory Note is legally binding in Hawaii. For it to be enforceable, both parties must sign the document, and it should clearly outline the terms of the loan. If a borrower fails to repay as agreed, the lender can take legal action to recover the owed amount.

Do I need a lawyer to create a Promissory Note in Hawaii?

While it is not legally required to have a lawyer draft a Promissory Note, consulting with one can be beneficial. A legal professional can ensure that the document complies with state laws and adequately protects the interests of both parties involved.

Can a Promissory Note be modified after it is signed?

Yes, a Promissory Note can be modified, but both parties must agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended terms to avoid future disputes.

What happens if the borrower defaults on the Promissory Note?

If a borrower defaults, the lender has the right to take legal action to recover the outstanding amount. This may involve filing a lawsuit or seeking a judgment against the borrower. The lender may also have the option to negotiate a repayment plan or settlement.

Is it necessary to notarize a Promissory Note in Hawaii?

Notarization is not required for a Promissory Note to be valid in Hawaii. However, having the document notarized can provide an extra layer of protection and help verify the identities of the parties involved. It can also strengthen the enforceability of the note in court.

Can a Promissory Note be secured or unsecured?

A Promissory Note can be either secured or unsecured. A secured note is backed by collateral, such as property or assets, which the lender can claim if the borrower defaults. An unsecured note, on the other hand, does not have collateral backing it, making it riskier for the lender.

What should I do if I lose my Promissory Note?

If you lose your Promissory Note, it is important to act quickly. Notify the other party involved and consider drafting a replacement note. You may also want to consult with a legal professional to discuss the best course of action to protect your rights and interests.