Instructions on Utilizing Idaho Promissory Note

Once you have your Idaho Promissory Note form ready, it’s time to fill it out carefully. Each section of the form requires specific information, and accuracy is key to ensure that the document serves its purpose effectively.

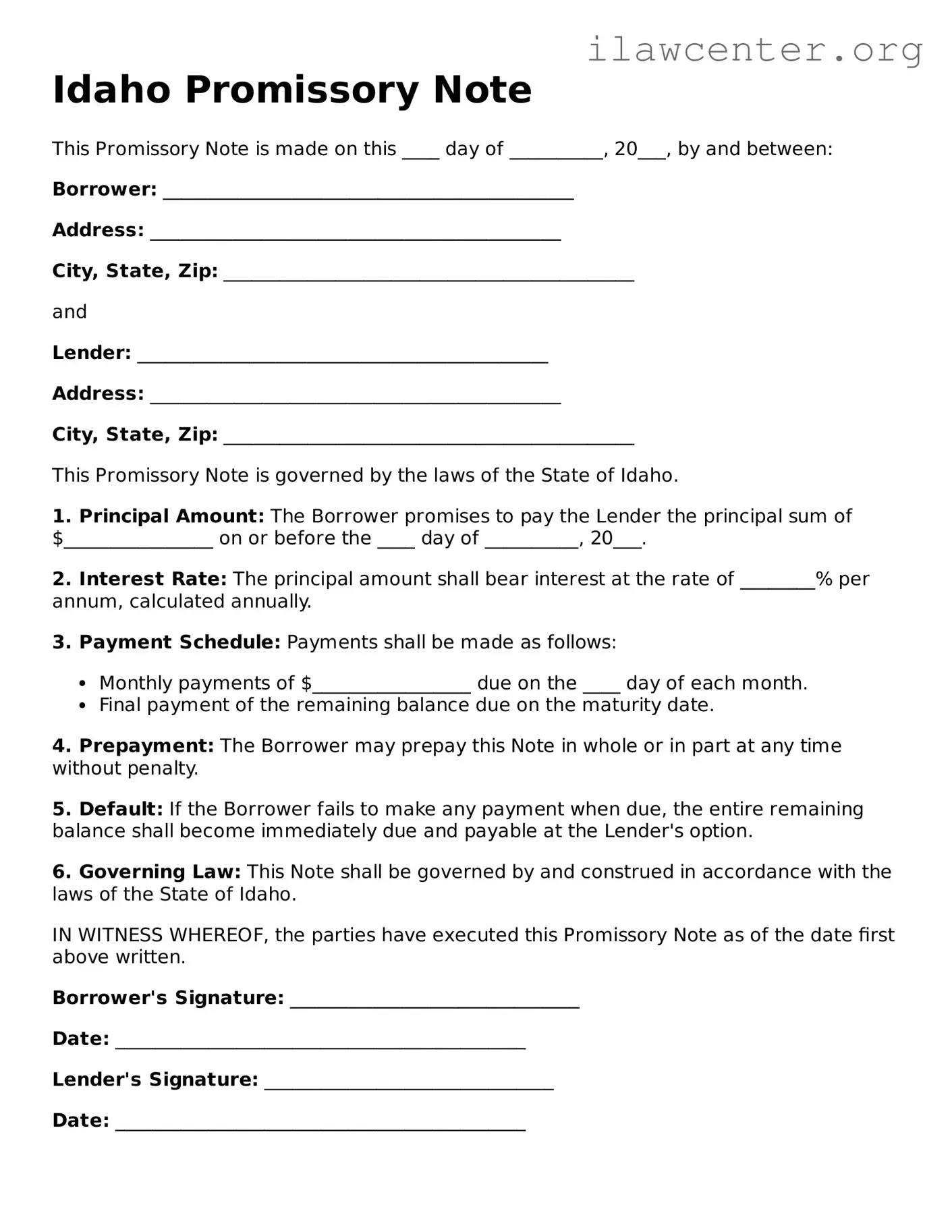

- Obtain the Form: Start by downloading the Idaho Promissory Note form from a reliable source or obtain a physical copy.

- Fill in the Date: Write the date on which the note is being created at the top of the form.

- Identify the Borrower: Clearly state the full name and address of the borrower. This is the individual or entity receiving the loan.

- Identify the Lender: Next, provide the full name and address of the lender. This is the person or organization providing the loan.

- Loan Amount: Enter the total amount of money being borrowed. This should be written both in numbers and in words to avoid any confusion.

- Interest Rate: Specify the interest rate applicable to the loan. Make sure to indicate whether it is fixed or variable.

- Payment Terms: Outline the payment schedule, including the frequency of payments (monthly, quarterly, etc.) and the due date for each payment.

- Late Fees: If applicable, detail any late fees that will be charged if payments are not made on time.

- Signatures: Finally, both the borrower and lender must sign and date the document to make it legally binding.

After completing the form, keep a copy for your records and provide a copy to the other party involved. This ensures that everyone has access to the same information and terms outlined in the agreement.