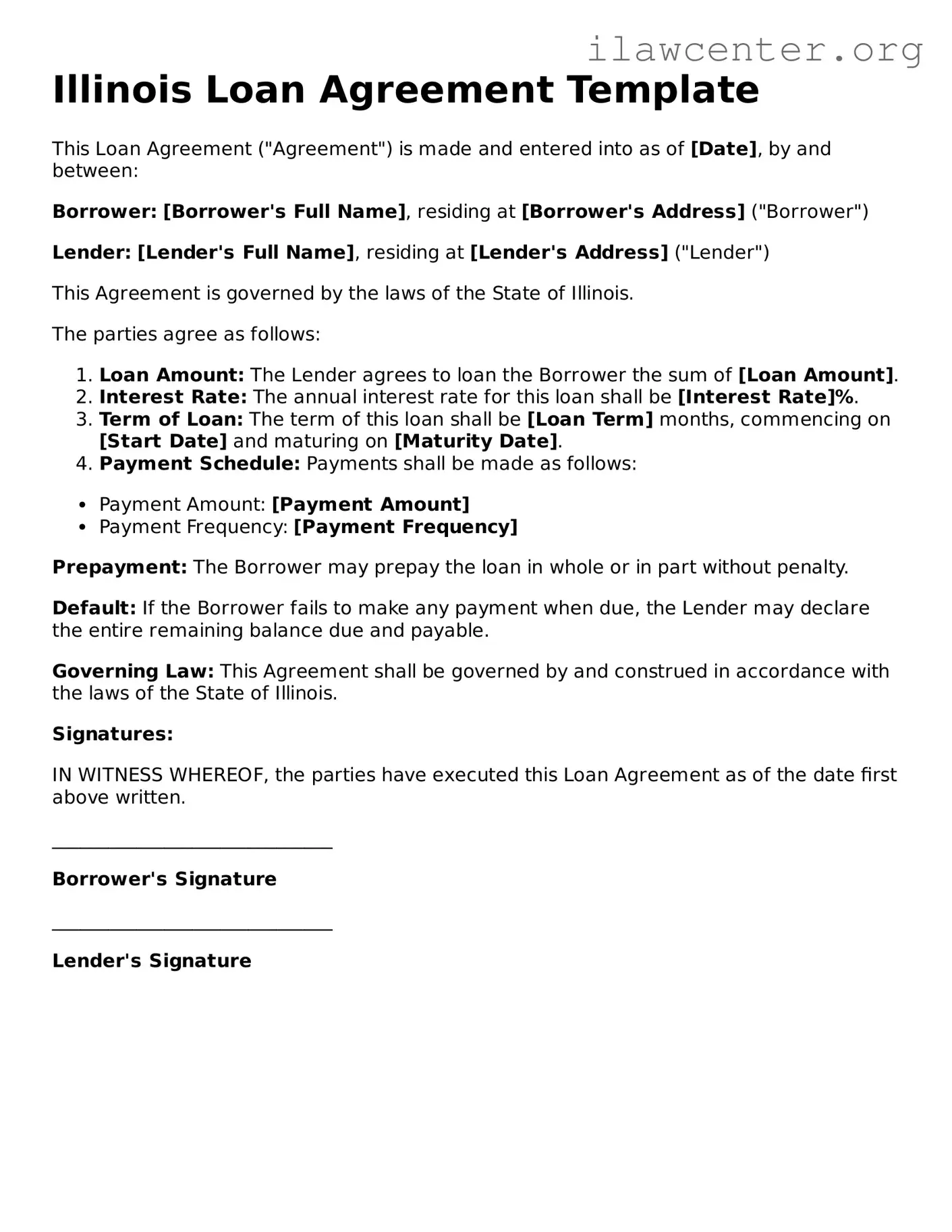

Instructions on Utilizing Illinois Loan Agreement

Once you have the Illinois Loan Agreement form in hand, you are ready to complete it. Follow these steps to ensure that all required information is accurately provided.

- Begin by entering the date at the top of the form.

- Fill in the names and addresses of both the borrower and the lender. Ensure that all details are correct.

- Specify the loan amount clearly. This should be a numerical figure.

- Indicate the interest rate applicable to the loan. Be precise to avoid any misunderstandings.

- Outline the repayment terms, including the schedule and duration of the loan. Include any grace periods if applicable.

- Provide details regarding any collateral, if required. Clearly describe the items or assets involved.

- Both parties should sign and date the form at the designated areas. Ensure that signatures are legible.

- Make a copy of the completed form for your records before submission.

After filling out the form, it is important to review all entries for accuracy. This will help prevent any future disputes or misunderstandings regarding the loan agreement.