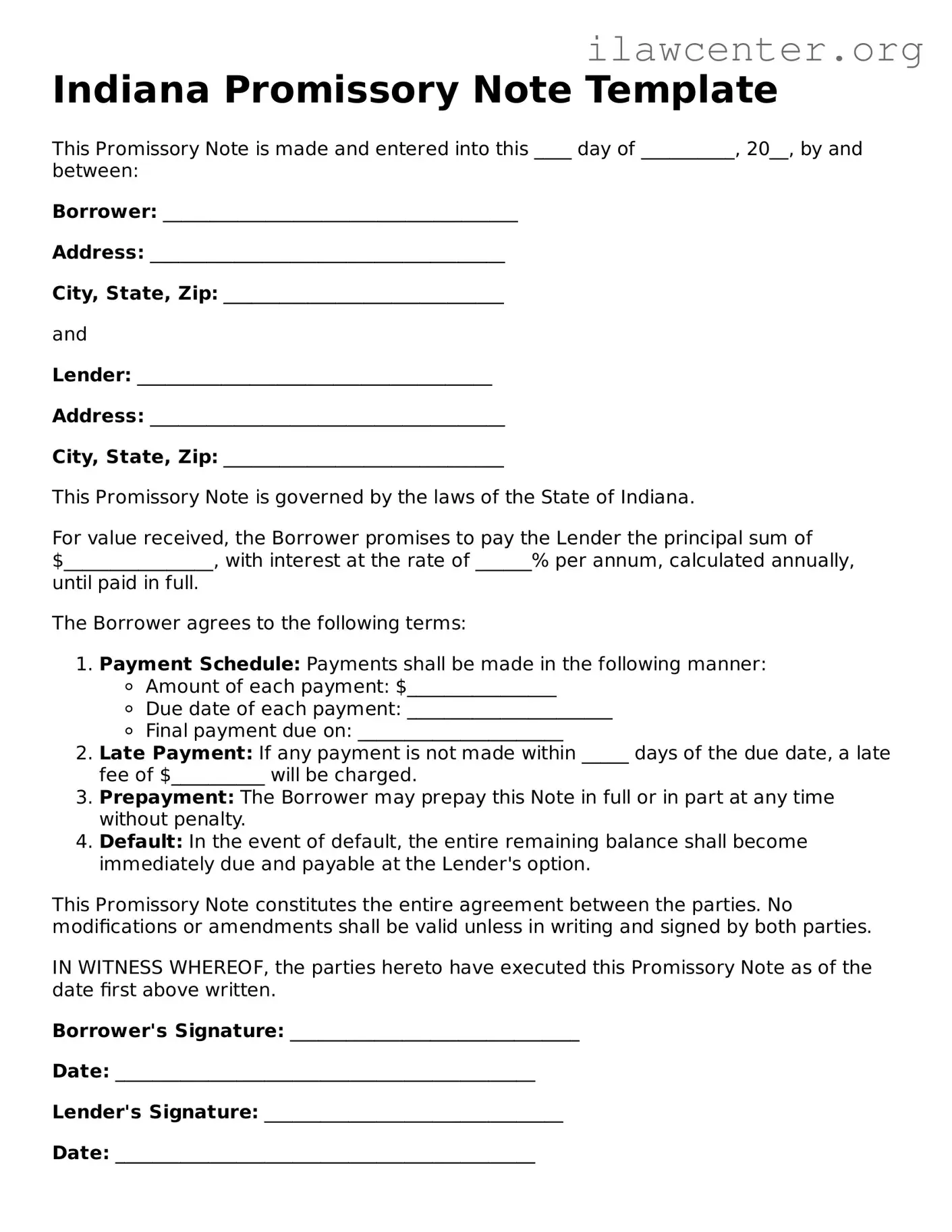

Instructions on Utilizing Indiana Promissory Note

Once you have the Indiana Promissory Note form in hand, you will need to complete it accurately to ensure that all necessary information is captured. This form typically requires details about the borrower, lender, and the terms of the loan. After filling it out, both parties should review the document before signing.

- Begin by entering the date at the top of the form.

- Fill in the name and address of the borrower in the designated section.

- Provide the name and address of the lender in the appropriate area.

- Specify the principal amount of the loan clearly.

- Indicate the interest rate, if applicable, and specify whether it is fixed or variable.

- Detail the repayment terms, including the payment schedule (monthly, quarterly, etc.).

- Include any late fees or penalties for missed payments, if applicable.

- State any prepayment terms, allowing for early repayment without penalties.

- Sign and date the document at the bottom, ensuring both borrower and lender do the same.