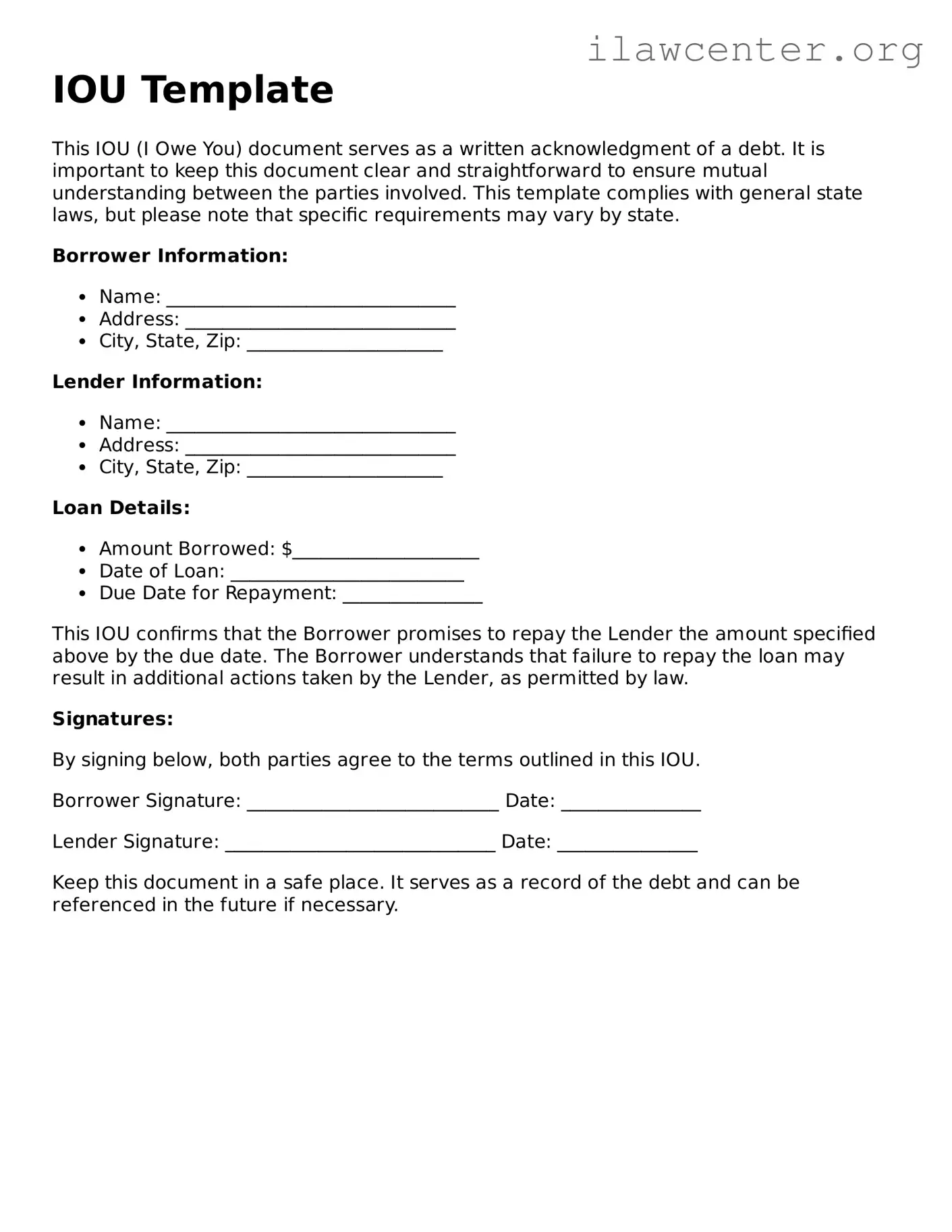

Common mistakes

Filling out an IOU form can seem straightforward, but many people make common mistakes that can lead to confusion or disputes later on. One frequent error is failing to include the full names of both parties involved. It is essential to clearly identify who owes the money and who is owed to avoid any misunderstandings.

Another mistake is omitting the amount owed. Without a specific dollar figure, the IOU lacks clarity. This can create problems if the borrower and lender have different expectations about the amount. Always write the amount clearly and double-check it for accuracy.

People often forget to include the date of the transaction. The date is crucial as it establishes when the debt was incurred. Not having a date can lead to disputes about when repayment is due.

Additionally, some individuals neglect to specify the repayment terms. Whether the borrower will pay back the debt in full or in installments should be clearly stated. This helps both parties understand the expectations regarding repayment.

Another common oversight is not signing the form. An unsigned IOU can be difficult to enforce. Both parties should sign the document to confirm their agreement and acknowledge the debt.

In some cases, people fail to provide contact information. Including phone numbers or email addresses can facilitate communication if any issues arise regarding the repayment.

Some individuals write the IOU in a vague or informal manner. Using clear and precise language is vital. Ambiguities can lead to different interpretations, which can cause conflicts down the line.

Another mistake is not keeping a copy of the signed IOU. Both parties should retain a copy for their records. This ensures that everyone has access to the same information regarding the debt.

People may also overlook the importance of witnesses. Having a neutral third party sign the IOU can add an extra layer of credibility and serve as proof of the agreement.

Finally, failing to review the completed form before finalizing it is a common error. A thorough review can help catch any mistakes or omissions, ensuring that the IOU is accurate and enforceable.