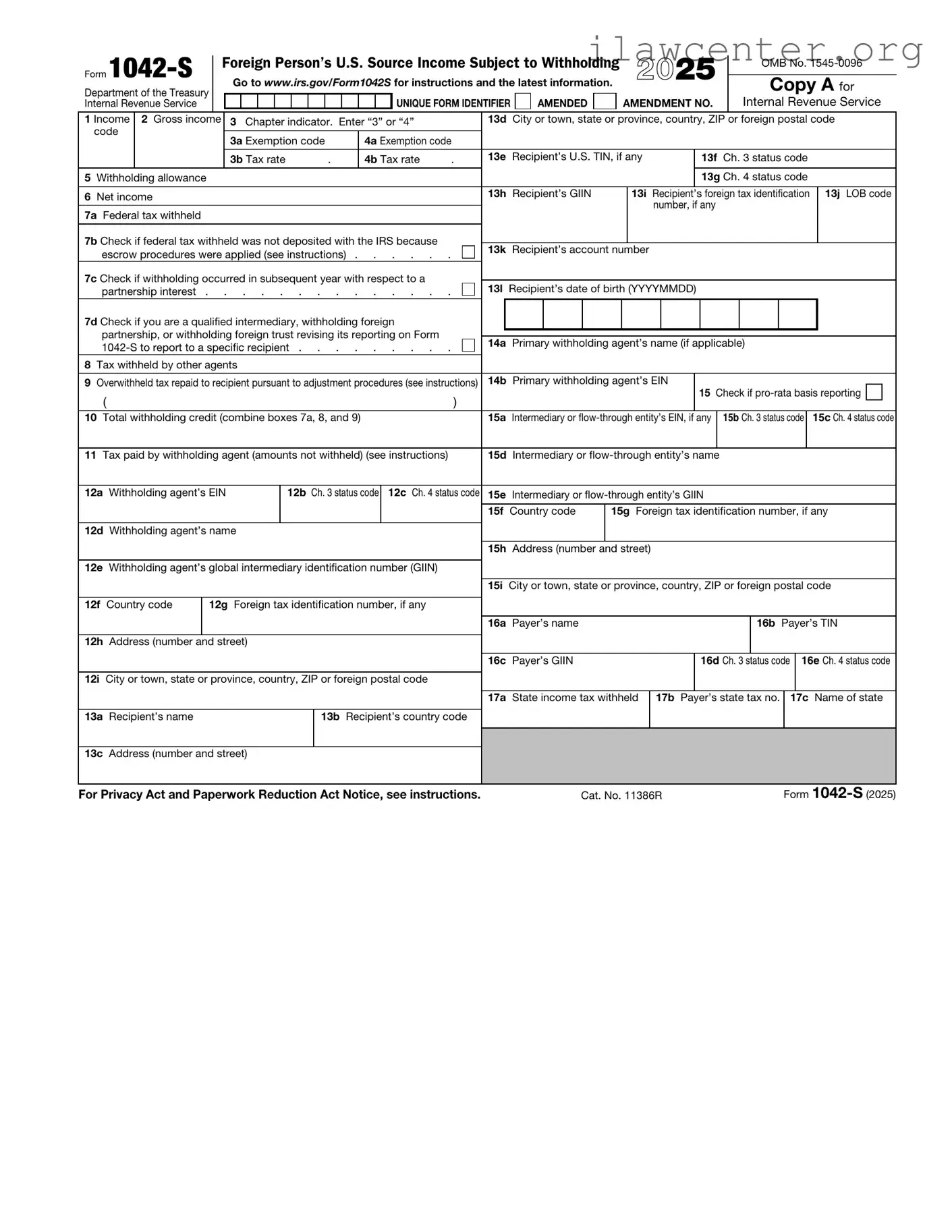

Instructions on Utilizing IRS 1042-S

After gathering the necessary information, you can begin filling out the IRS 1042-S form. This form is used for reporting income and withholding for foreign persons. Ensure that all details are accurate to avoid any issues with the IRS.

- Obtain a copy of the IRS 1042-S form. This can be downloaded from the IRS website or obtained from a tax professional.

- Fill in the recipient's name in the designated field. This should be the name of the foreign person receiving the income.

- Provide the recipient's address. Include the street address, city, state, and postal code.

- Enter the recipient's country of residence. This should be the country where the recipient is a tax resident.

- In the payer's information section, fill in your name or the name of the business that is making the payment.

- Complete the payer's address section with the appropriate details, including street address, city, state, and postal code.

- Indicate the type of income being reported. This could include amounts like dividends, interest, or royalties.

- Report the gross income amount in the appropriate box. This should reflect the total income paid to the recipient.

- Enter the withholding tax amount in the designated box. This is the amount withheld from the gross income.

- Complete any additional fields as required, such as the tax treaty information if applicable.

- Review the form for accuracy. Ensure all information is correct and complete.

- Sign and date the form at the bottom. This certifies that the information provided is true and correct.

- Submit the form to the IRS and provide a copy to the recipient.