Instructions on Utilizing IRS 709

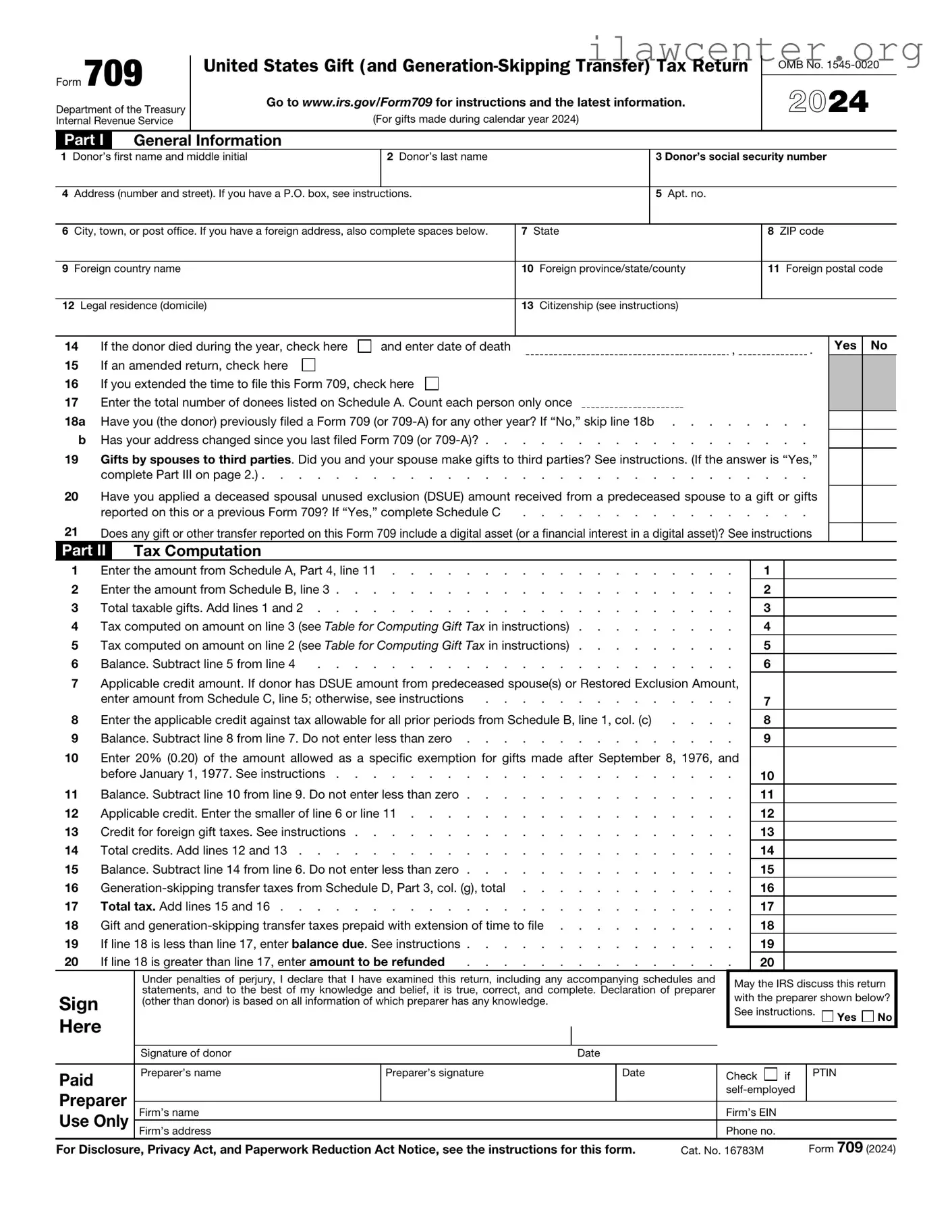

Filling out the IRS 709 form is an important step if you are making a gift that exceeds the annual exclusion limit. Completing this form correctly helps ensure that your tax obligations are met. Here’s how to fill it out step by step.

- Begin by downloading the IRS 709 form from the IRS website or obtain a physical copy.

- At the top of the form, enter your name, Social Security number, and address. Make sure this information is accurate.

- In Part 1, indicate the year for which you are filing the form. This is typically the year the gift was made.

- In Part 2, list the gifts you made during the year. Include the recipient's name, their relationship to you, and the date of the gift.

- Next, provide the fair market value of each gift at the time it was given. This is crucial for accurate reporting.

- If you made multiple gifts, continue listing them until all are accounted for.

- In Part 3, calculate the total value of all gifts. Add up the amounts from Part 2.

- If any gifts qualify for exclusions or deductions, make sure to note those in the appropriate sections.

- After completing the form, review it for any errors or missing information. Accuracy is key.

- Finally, sign and date the form. If you're filing jointly, your spouse should also sign if applicable.

Once you have completed the form, make copies for your records. Then, mail it to the address specified in the form instructions. Keep in mind that this is a key part of your financial documentation.