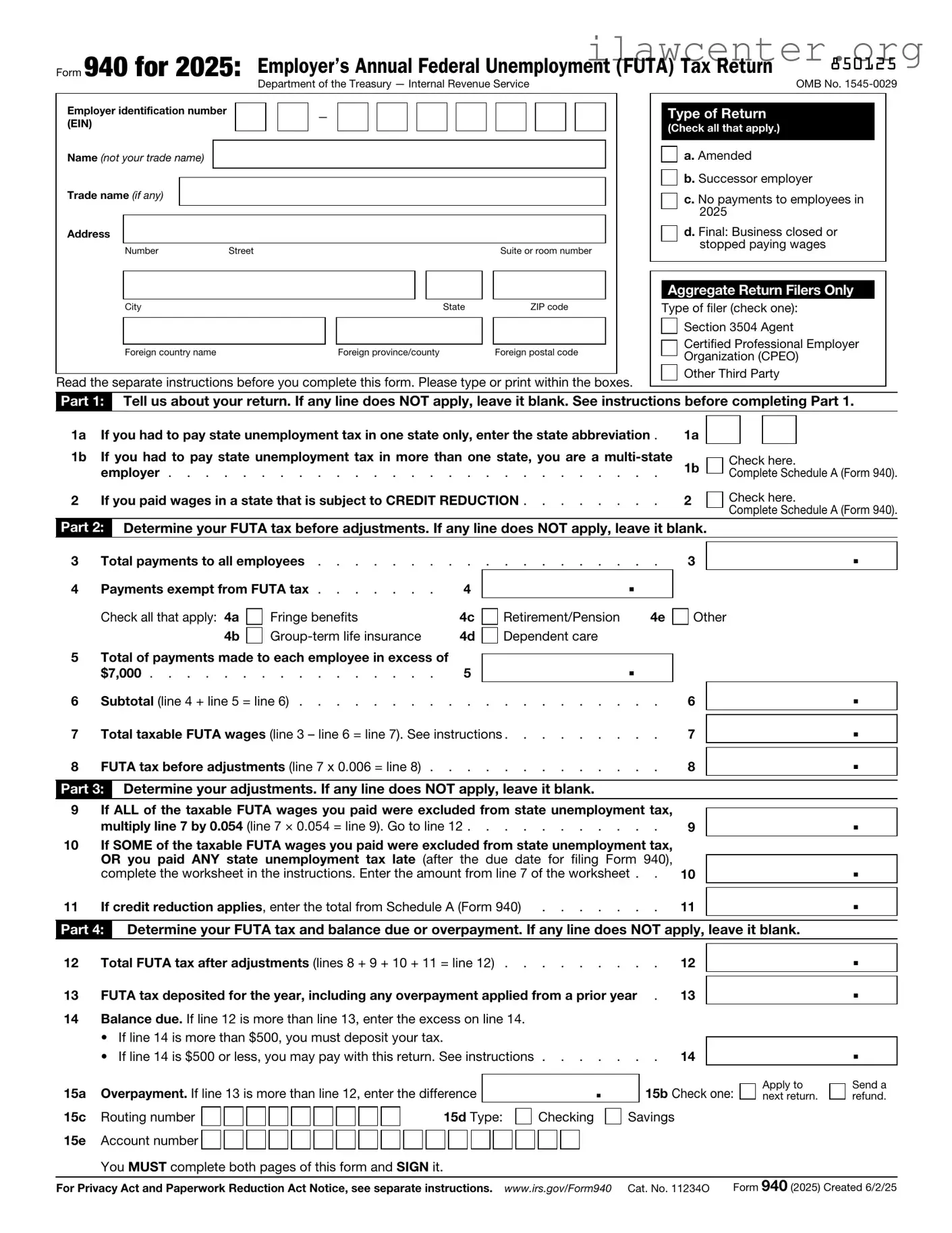

Instructions on Utilizing IRS 940

Completing the IRS 940 form is a crucial step for employers who need to report their annual Federal Unemployment Tax Act (FUTA) tax. By accurately filling out this form, you ensure compliance with federal tax regulations. Follow these steps to fill out the form correctly.

- Gather necessary information. Collect your business details, including your Employer Identification Number (EIN), business name, and address.

- Download the IRS 940 form from the IRS website or obtain a physical copy.

- Begin with Part 1 of the form. Enter your business name and address as it appears on your tax records.

- Fill in your EIN in the designated box. This number is essential for identifying your business with the IRS.

- In Part 1, indicate whether you are a seasonal employer by checking the appropriate box.

- Move to Part 2. Report the total payments made to employees during the year. This includes wages and any other compensation subject to FUTA tax.

- Calculate the FUTA tax owed. Use the applicable tax rate on the total payments reported in Part 2.

- Complete Part 3 if you had any adjustments or credits to report. This could include state unemployment tax credits.

- Review the form for accuracy. Ensure that all numbers are correct and that you have signed and dated the form.

- Submit the completed form. You can file it electronically or mail it to the appropriate IRS address based on your location.

After submitting the form, keep a copy for your records. This documentation will be important for future reference and potential audits. Ensure you stay informed about any updates to tax laws that may affect your filing requirements in the future.