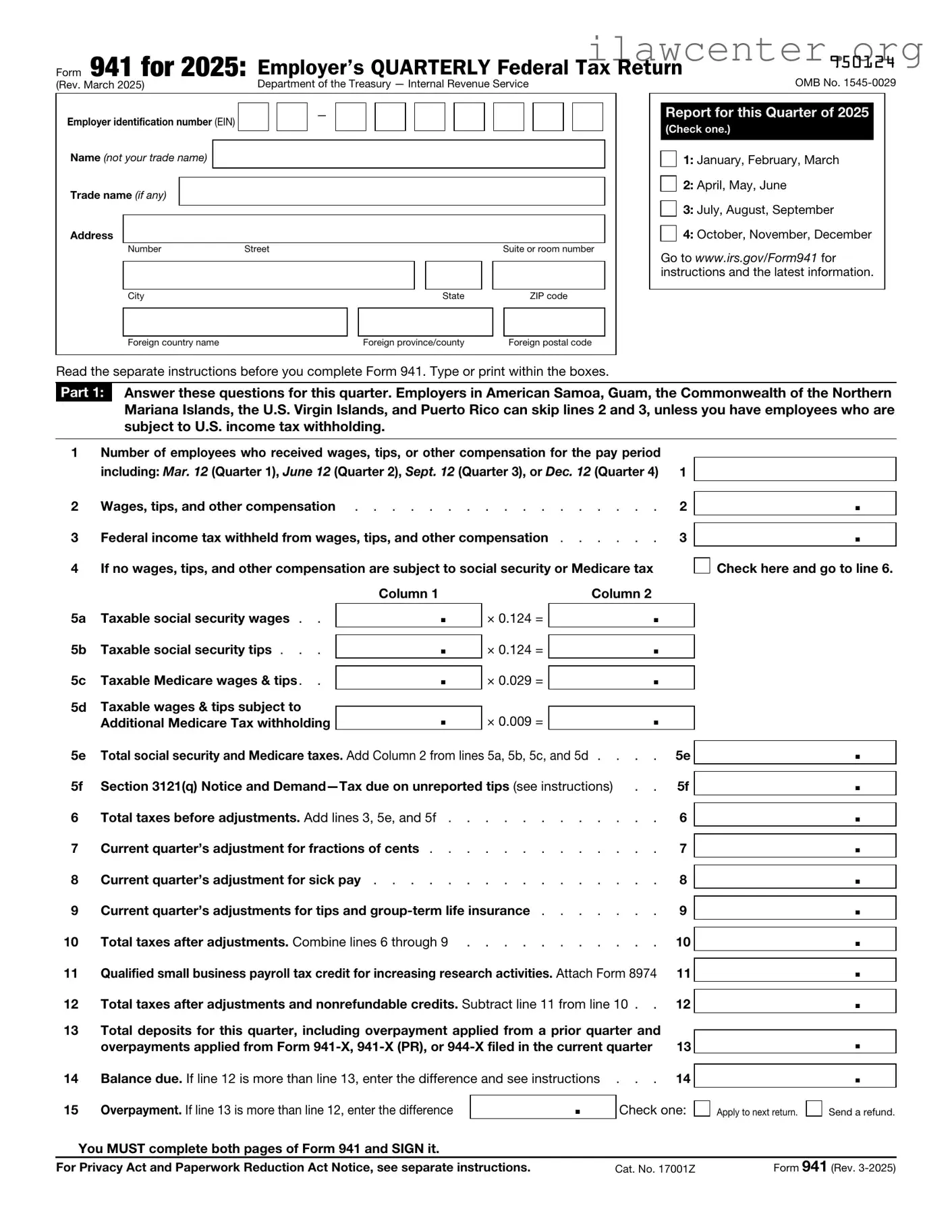

Instructions on Utilizing IRS 941

Filling out the IRS Form 941 is an important task for employers who need to report payroll taxes. Completing this form accurately is essential for compliance with federal tax obligations. After you fill it out, you will submit it to the IRS, usually on a quarterly basis, to report wages paid, tips received, and taxes withheld from employees.

- Obtain the IRS Form 941. You can download it from the IRS website or request a physical copy.

- Enter your employer identification information at the top of the form, including your name, address, and EIN (Employer Identification Number).

- Fill in the quarter for which you are reporting. This will be indicated in the designated box on the form.

- Report the number of employees you paid during the quarter in the appropriate section.

- Calculate total wages, tips, and other compensation paid to employees during the quarter. Enter this amount in the specified box.

- Determine the total taxes withheld from employees’ wages and report this figure as well.

- Complete the sections regarding adjustments for fractions of cents and any other adjustments you need to make.

- Calculate the total tax liability for the quarter by adding the amounts from the previous sections.

- Determine the amount of tax deposits you have made for the quarter. Enter this information in the appropriate section.

- Calculate any balance due or overpayment and enter it in the designated area.

- Sign and date the form. Ensure that the person signing is authorized to do so.

- Make a copy of the completed form for your records before submitting it to the IRS.

Once the form is filled out, review it for accuracy. Double-check all calculations and ensure that all required fields are completed. After confirming everything is correct, submit the form to the IRS by the appropriate deadline to avoid penalties.