Instructions on Utilizing IRS Schedule E 1040

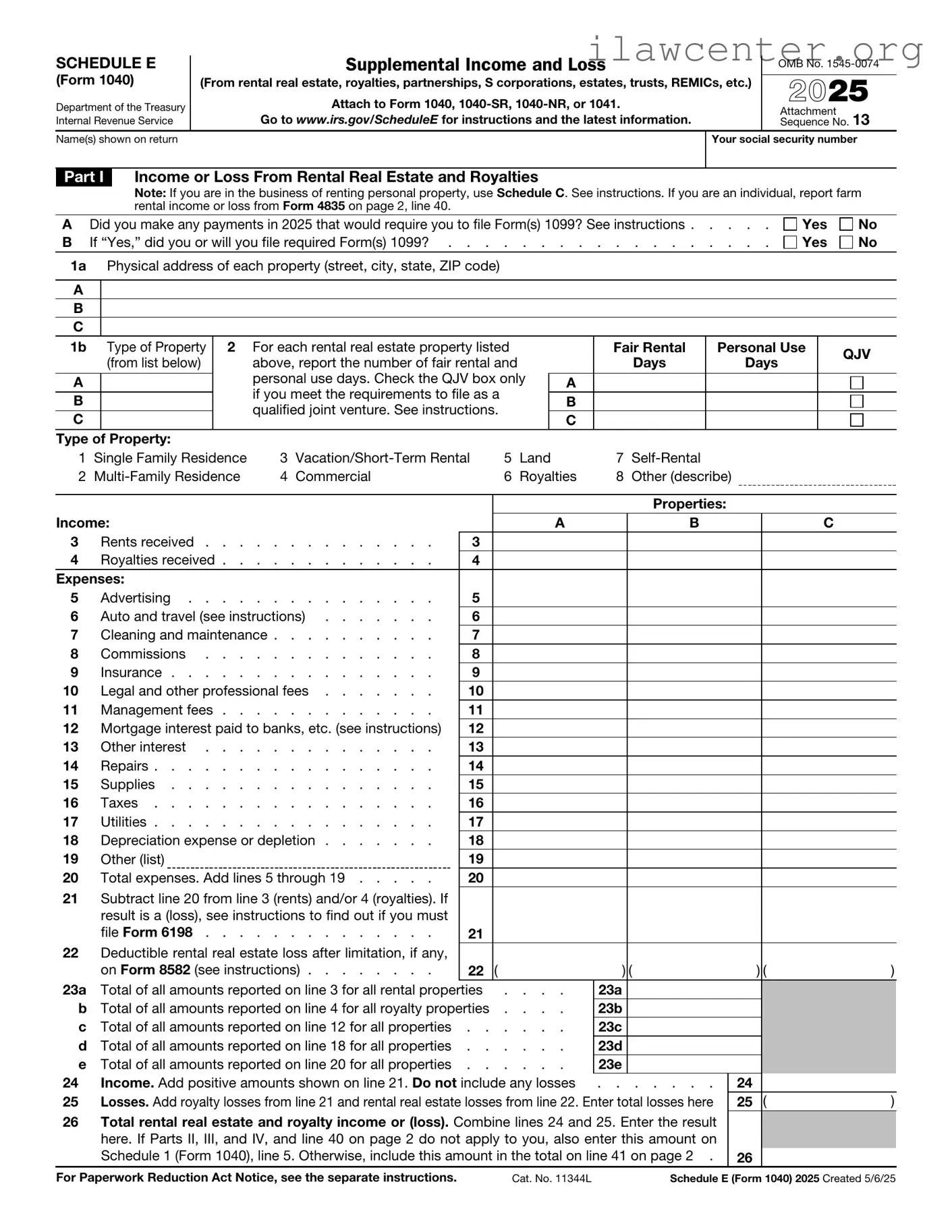

Filling out the IRS Schedule E (Form 1040) can seem daunting at first, but breaking it down into manageable steps makes the process easier. This form is used to report income or loss from rental real estate, royalties, partnerships, S corporations, estates, trusts, and more. Let’s dive into the steps needed to complete this form.

- Gather your documents. Collect all relevant information, including income statements, expenses, and any other necessary financial records.

- Obtain the Schedule E form. You can download it from the IRS website or get a physical copy from a local IRS office.

- Fill out your personal information. At the top of the form, enter your name, Social Security number, and address.

- Complete Part I for rental real estate. List each property separately. Include the address, the type of property, and the income received.

- Report your expenses. In the same section, detail the expenses associated with each property, such as repairs, maintenance, and management fees.

- Calculate the net income or loss. Subtract your total expenses from your total income for each property.

- Move to Part II if you have partnerships or S corporations. Report your share of income or loss from these entities.

- Fill out Part III for royalties, if applicable. Provide information about any royalties you earned during the tax year.

- Review your entries for accuracy. Double-check all numbers and ensure that all required information is included.

- Sign and date the form. Make sure to sign it before submitting it to the IRS.

Once you have completed the form, keep a copy for your records. Then, submit it along with your Form 1040 when you file your taxes. Remember, accuracy is key to avoid any issues with the IRS.