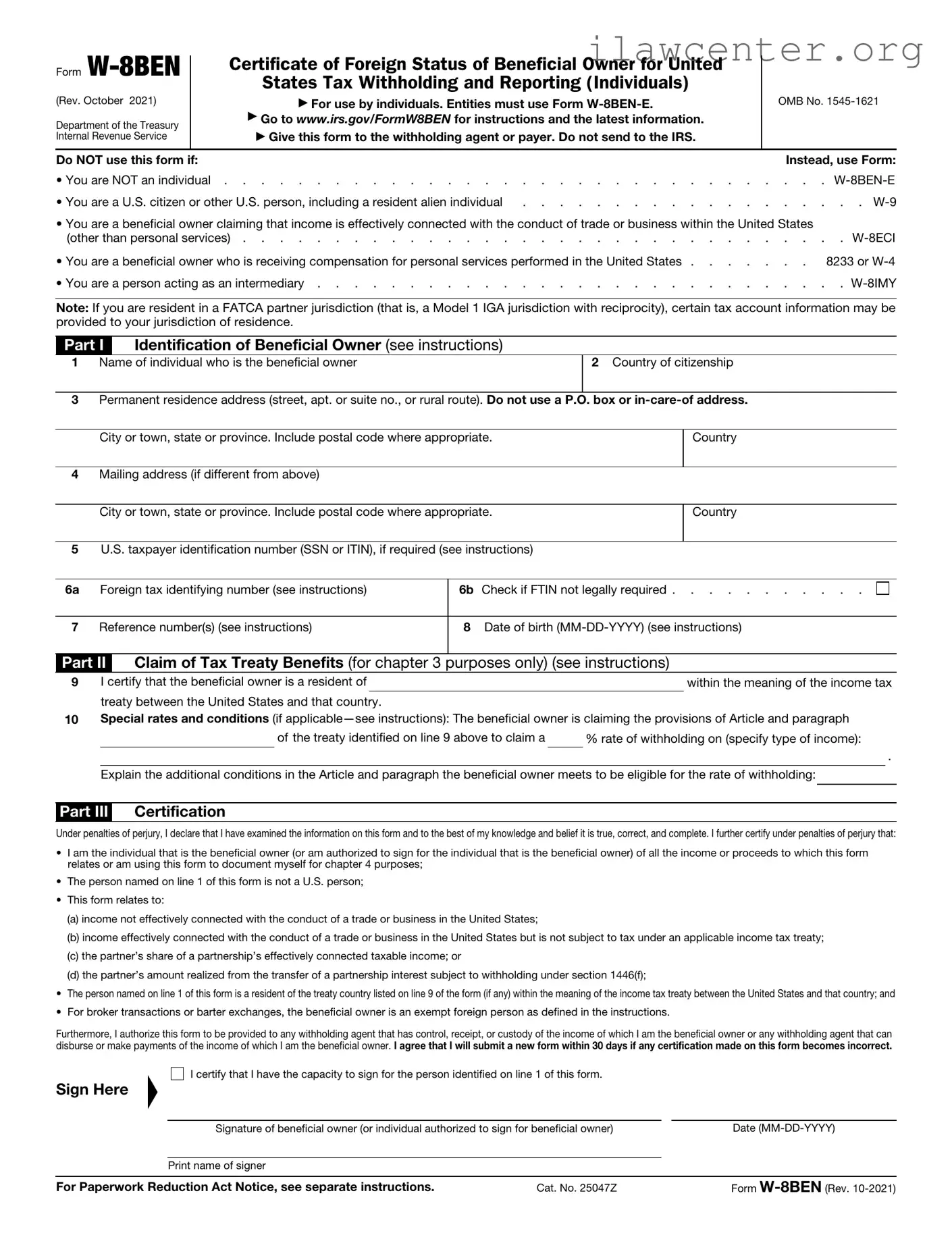

Form W-8BEN

(Rev. October 2021)

Department of the Treasury

Internal Revenue Service

Certificate of Foreign Status of Beneficial Owner for United

States Tax Withholding and Reporting (Individuals)

▶

For use by individuals. Entities must use Form W-8BEN-E.

▶

Go to www.irs.gov/FormW8BEN for instructions and the latest information.

▶

Give this form to the withholding agent or payer. Do not send to the IRS.

OMB No. 1545-1621

Do NOT use this form if: Instead, use Form:

• You are NOT an individual . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . W-8BEN-E

• You are a U.S. citizen or other U.S. person, including a resident alien individual . . . . . . . . . . . . . . . . . . . W-9

• You are a beneficial owner claiming that income is effectively connected with the conduct of trade or business within the United States

(other than personal services) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . W-8ECI

• You are a beneficial owner who is receiving compensation for personal services performed in the United States . . . . . . . 8233 or W-4

• You are a person acting as an intermediary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . W-8IMY

Note: If you are resident in a FATCA partner jurisdiction (that is, a Model 1 IGA jurisdiction with reciprocity), certain tax account information may be

provided to your jurisdiction of residence.

Part I Identification of Beneficial Owner (see instructions)

1 Name of individual who is the beneficial owner 2 Country of citizenship

3 Permanent residence address (street, apt. or suite no., or rural route). Do not use a P.O. box or in-care-of address.

City or town, state or province. Include postal code where appropriate. Country

4 Mailing address (if different from above)

City or town, state or province. Include postal code where appropriate. Country

5 U.S. taxpayer identification number (SSN or ITIN), if required (see instructions)

6a Foreign tax identifying number (see instructions)

6b Check if FTIN not legally required . . . . . . . . . . .

7 Reference number(s) (see instructions)

8 Date of birth (MM-DD-YYYY) (see instructions)

Part II Claim of Tax Treaty Benefits (for chapter 3 purposes only) (see instructions)

9

I certify that the beneficial owner is a resident of

within the meaning of the income tax

treaty between the United States and that country.

10

Special rates and conditions (if applicable—see instructions): The beneficial owner is claiming the provisions of Article and paragraph

of the treaty identified on line 9 above to claim a

% rate of withholding on (specify type of income):

.

Explain the additional conditions in the Article and paragraph the beneficial owner meets to be eligible for the rate of withholding:

Part III Certification

Under penalties of perjury, I declare that I have examined the information on this form and to the best of my knowledge and belief it is true, correct, and complete. I further certify under penalties of perjury that:

• I am the individual that is the beneficial owner (or am authorized to sign for the individual that is the beneficial owner) of all the income or proceeds to which this form

relates or am using this form to document myself for chapter 4 purposes;

• The person named on line 1 of this form is not a U.S. person;

• This form relates to:

(a) income not effectively connected with the conduct of a trade or business in the United States;

(b) income effectively connected with the conduct of a trade or business in the United States but is not subject to tax under an applicable income tax treaty;

(c) the partner’s share of a partnership’s effectively connected taxable income; or

(d) the partner’s amount realized from the transfer of a partnership interest subject to withholding under section 1446(f);

•

The person named on line 1 of this form is a resident of the treaty country listed on line 9 of the form (if any) within the meaning of the income tax treaty between the United States and that country; and

• For broker transactions or barter exchanges, the beneficial owner is an exempt foreign person as defined in the instructions.

Furthermore, I authorize this form to be provided to any withholding agent that has control, receipt, or custody of the income of which I am the beneficial owner or any withholding agent that can

disburse or make payments of the income of which I am the beneficial owner. I agree that I will submit a new form within 30 days if any certification made on this form becomes incorrect.

Sign Here

▲

I certify that I have the capacity to sign for the person identified on line 1 of this form.

Signature of beneficial owner (or individual authorized to sign for beneficial owner)

Date (MM-DD-YYYY)

Print name of signer

For Paperwork Reduction Act Notice, see separate instructions.

Cat. No. 25047Z

Form W-8BEN (Rev. 10-2021)