What is a Kansas Promissory Note?

A Kansas Promissory Note is a written agreement in which one party promises to pay a specific amount of money to another party at a designated time or on demand. It serves as a legal document that outlines the terms of the loan, including interest rates, repayment schedules, and any collateral involved. This form is commonly used in personal loans, business transactions, and real estate deals in Kansas.

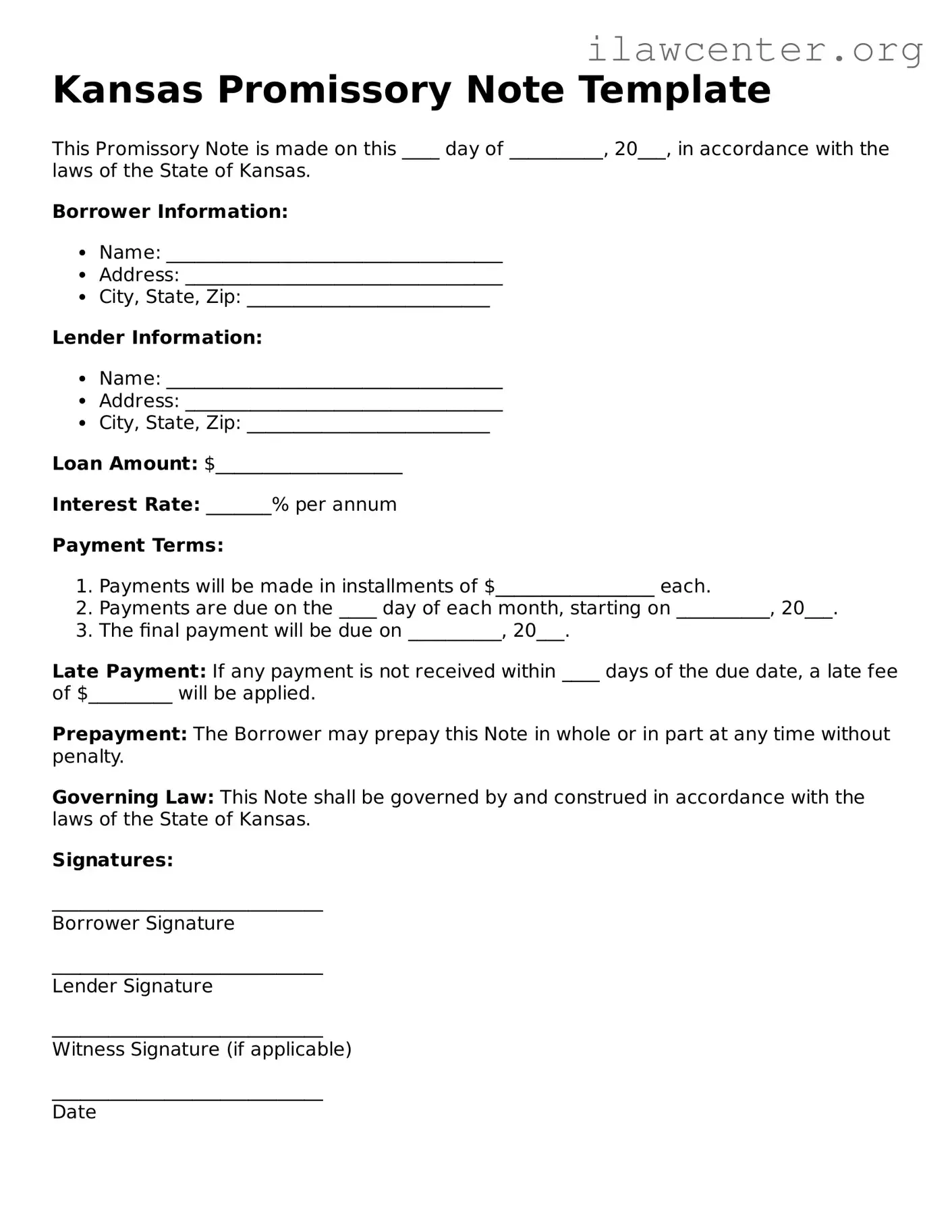

What are the key components of a Kansas Promissory Note?

Essential components include the names and addresses of the borrower and lender, the principal amount, the interest rate, the repayment terms, and the date of the agreement. Additionally, any penalties for late payments or default, as well as provisions for prepayment, should be clearly stated. Including these details ensures clarity and protects the rights of both parties.

Is a Kansas Promissory Note legally binding?

Yes, a properly executed Kansas Promissory Note is legally binding. This means that if one party fails to uphold their end of the agreement, the other party can take legal action to enforce the terms. To be enforceable, the note must meet specific legal requirements, such as being signed by the borrower and containing all necessary details.

Do I need to notarize a Kansas Promissory Note?

Notarization is not required for a Kansas Promissory Note to be valid. However, having the document notarized can add an extra layer of security and credibility. It provides proof that the parties involved willingly signed the document, which can be beneficial in case of a dispute.

What happens if the borrower defaults on the loan?

If the borrower defaults, the lender has several options. They may choose to initiate legal proceedings to recover the owed amount. The terms of the promissory note should outline the steps the lender can take in the event of a default, including any late fees or interest that may accrue. Understanding these terms beforehand can help both parties navigate potential issues.

Can a Kansas Promissory Note be modified?

Yes, a Kansas Promissory Note can be modified if both parties agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended note. This ensures that there is a clear record of the new terms and helps prevent misunderstandings in the future.

Where can I obtain a Kansas Promissory Note form?

Kansas Promissory Note forms can be obtained from various sources. Many legal websites offer templates that can be customized to fit specific needs. Additionally, local legal offices or financial institutions may provide forms. It is important to ensure that the form complies with Kansas state laws and includes all necessary information.