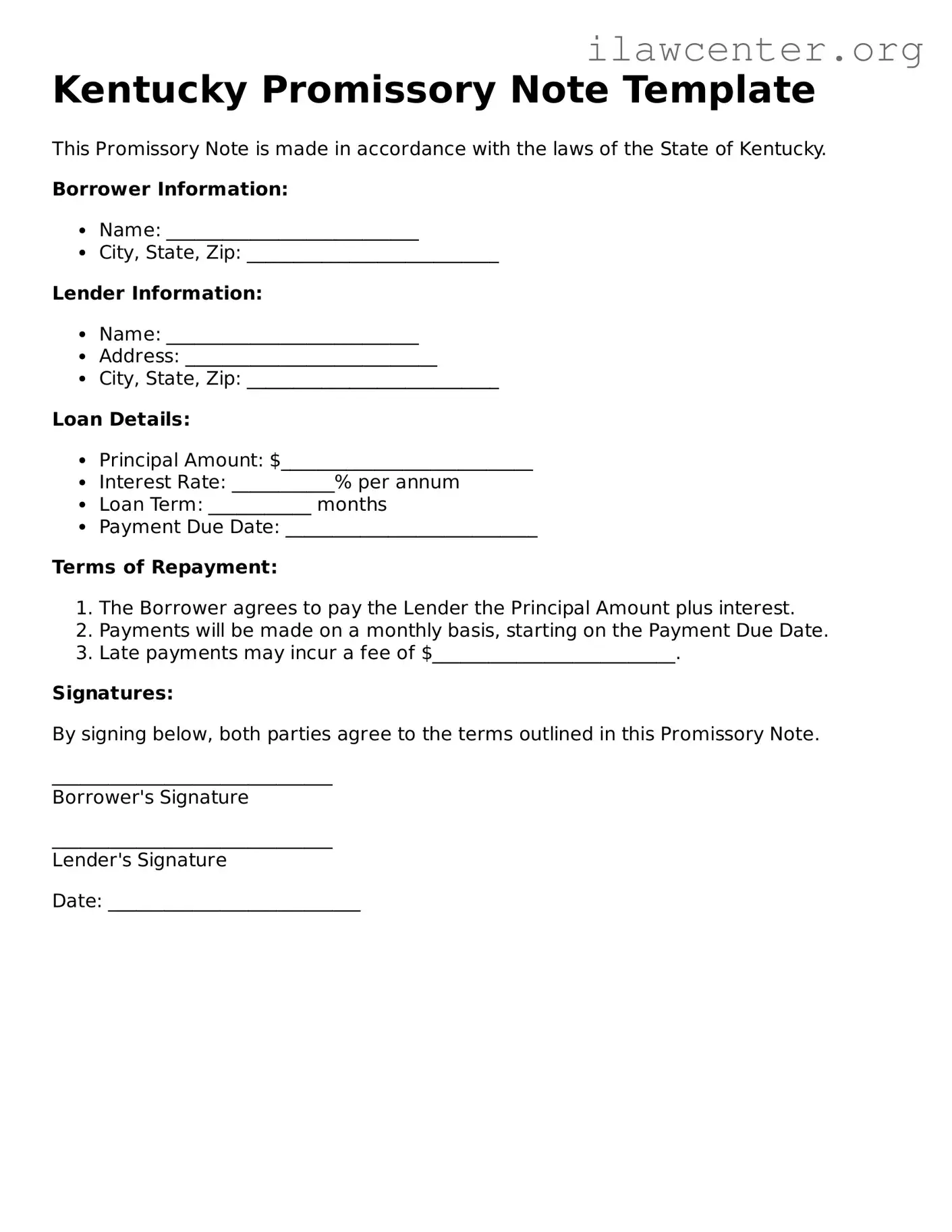

Instructions on Utilizing Kentucky Promissory Note

Once you have your Kentucky Promissory Note form ready, it's time to fill it out accurately. This form is essential for documenting a loan agreement between a borrower and a lender. Completing it correctly helps ensure that both parties understand their obligations and rights under the agreement.

- Title the Document: At the top of the form, write "Promissory Note" to clearly indicate the purpose of the document.

- Enter the Date: Write the date when the note is being created. This is important for record-keeping purposes.

- Identify the Borrower: Clearly state the full name and address of the borrower. This identifies who is responsible for repaying the loan.

- Identify the Lender: Write the full name and address of the lender. This indicates who is providing the loan.

- Loan Amount: Specify the total amount of money being borrowed. This should be a clear numerical figure.

- Interest Rate: If applicable, include the interest rate for the loan. This can be expressed as a percentage.

- Payment Terms: Outline how and when the borrower will repay the loan. Include details such as the payment schedule (monthly, quarterly, etc.) and due dates.

- Late Fees: If there are penalties for late payments, specify the amount or percentage that will be charged.

- Signatures: Both the borrower and lender should sign and date the form to make it legally binding.

After completing the form, make sure both parties keep a copy for their records. This helps ensure that everyone is on the same page regarding the terms of the loan and can refer back to the agreement if needed.