Instructions on Utilizing Loan Estimate

Filling out the Loan Estimate form is a crucial step in understanding your mortgage options. This document provides important information about the terms of your loan, helping you make informed decisions. Here’s how to complete the form effectively.

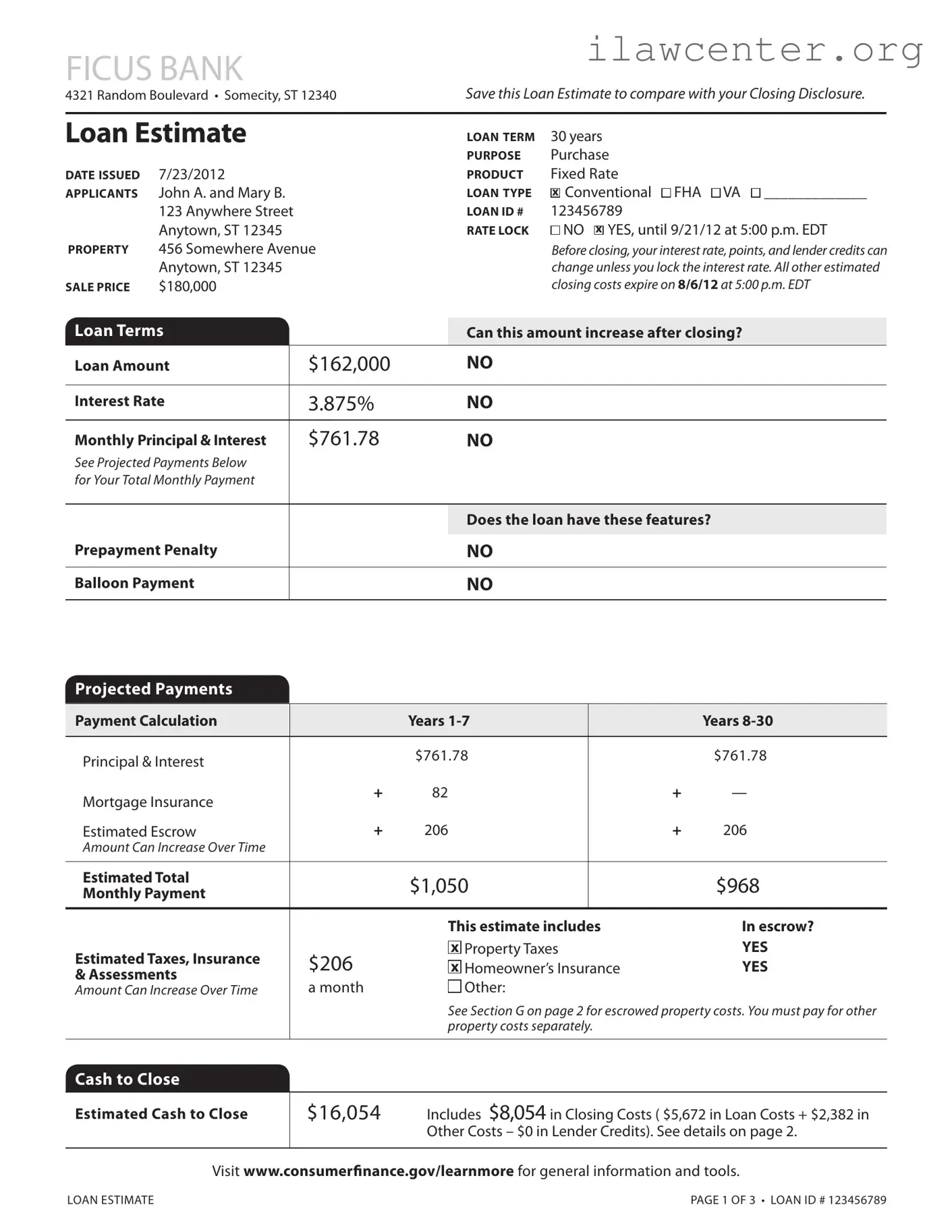

- Identify the Lender: At the top of the form, write the name of the lender, which in this case is Ficus Bank, along with their address.

- Enter Loan Information: Fill in the loan term, purpose, and product type. For example, you might select a 30-year fixed-rate loan.

- List the Applicants: Write the names of all applicants, such as John A. and Mary B.

- Provide Loan Type: Indicate the type of loan you are applying for, such as Conventional, FHA, or VA.

- Fill in Property Address: Enter the address of the property you intend to purchase.

- Complete Loan ID: Write the loan identification number, which is essential for tracking your application.

- Rate Lock Information: Specify whether you have locked in your interest rate and the expiration date for that lock.

- Enter Sale Price: Fill in the estimated sale price of the property you wish to buy.

- Provide Loan Amount: Write the amount you are borrowing.

- Fill in Interest Rate: Enter the interest rate you expect to receive on the loan.

- Calculate Monthly Payments: Estimate your monthly principal and interest payment based on the loan amount and interest rate.

- Detail Projected Payments: Include any additional costs such as mortgage insurance and property taxes.

- Calculate Cash to Close: Provide an estimate of the cash needed at closing, including closing costs and down payment.

- List Closing Cost Details: Break down the closing costs into categories such as loan costs and other costs.

- Complete Additional Information: Fill in any additional information about the loan, including the lender's contact details and your loan officer's information.

After completing the Loan Estimate form, review it carefully to ensure all information is accurate. This document will serve as a valuable reference as you proceed with your mortgage process.