|

|

|

|

|

|

|

|

|

|

|

|

Reset Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

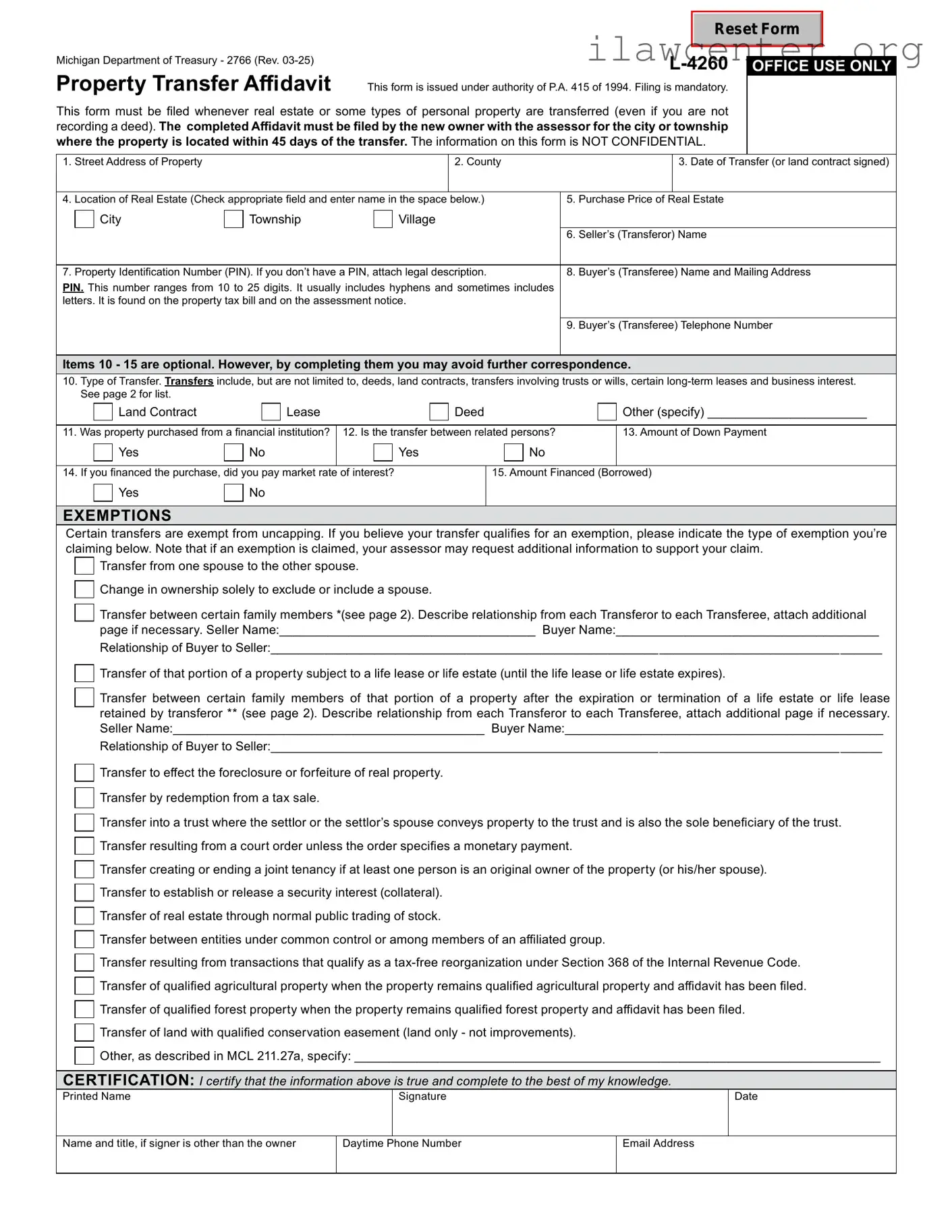

Michigan Department of Treasury - 2766 (Rev. 03-25) |

|

|

|

|

|

L-4260 |

OFFICE USE ONLY |

|

|

|

|

|

|

|

|

|

|

Property Transfer Affidavit |

This form is issued under authority of P.A. 415 of 1994. Filing is mandatory. |

|

|

|

|

This form must be filed whenever real estate or some types of personal property are transferred (even if you are not |

|

|

recording a deed). The completed Affidavit must be filed by the new owner with the assessor for the city or township |

|

|

where the property is located within 45 days of the transfer. The information on this form is NOT CONFIDENTIAL. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1. Street Address of Property |

|

|

|

|

|

2. County |

|

|

3. Date of Transfer (or land contract signed) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. Location of Real Estate (Check appropriate field and enter name in the space |

below.) |

5. |

Purchase Price of |

Real Estate |

|

|

|

|

City |

|

Township |

|

|

Village |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6. |

Seller’s (Transferor) Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7. Property Identification Number (PIN). If you don’t have a PIN, attach legal description. |

8. |

Buyer’s (Transferee) Name and Mailing Address |

PIN. This number ranges from 10 to 25 digits. It usually includes hyphens and sometimes includes |

|

|

|

|

|

|

letters. It is found on the property tax bill and on the assessment notice. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9. |

Buyer’s (Transferee) Telephone Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Items 10 - 15 are optional. However, by completing them you may avoid further correspondence.

10.Type of Transfer. Transfers include, but are not limited to, deeds, land contracts, transfers involving trusts or wills, certain long-term leases and business interest.

See page 2 for list.

Other (specify) _______________________

11. Was property purchased from a financial institution? |

12. Is the transfer between related persons? |

13. Amount of Down Payment |

|

|

Yes |

|

No |

|

|

Yes |

|

|

No |

|

|

|

|

|

|

|

|

|

|

|

|

|

14. If you financed the purchase, did you pay market rate |

of interest? |

15. Amount Financed (Borrowed) |

|

|

Yes |

|

No |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

EXEMPTIONS

Certain transfers are exempt from uncapping. If you believe your transfer qualifies for an exemption, please indicate the type of exemption you’re claiming below. Note that if an exemption is claimed, your assessor may request additional information to support your claim.

Transfer from one spouse to the other spouse.

Change in ownership solely to exclude or include a spouse.

Transfer between certain family members *(see page 2). Describe relationship from each Transferor to each Transferee, attach additional page if necessary. Seller Name:_____________________________________ Buyer Name:______________________________________

Relationship of Buyer to Seller:________________________________________________________________________________________

Transfer of that portion of a property subject to a life lease or life estate (until the life lease or life estate expires).

Transfer between certain family members of that portion of a property after the expiration or termination of a life estate or life lease retained by transferor ** (see page 2). Describe relationship from each Transferor to each Transferee, attach additional page if necessary. Seller Name:_____________________________________________ Buyer Name:______________________________________________

Relationship of Buyer to Seller:________________________________________________________________________________________

Transfer to effect the foreclosure or forfeiture of real property.

Transfer by redemption from a tax sale.

Transfer into a trust where the settlor or the settlor’s spouse conveys property to the trust and is also the sole beneficiary of the trust.

Transfer resulting from a court order unless the order specifies a monetary payment.

Transfer creating or ending a joint tenancy if at least one person is an original owner of the property (or his/her spouse).

Transfer to establish or release a security interest (collateral).

Transfer of real estate through normal public trading of stock.

Transfer between entities under common control or among members of an affiliated group.

Transfer resulting from transactions that qualify as a tax-free reorganization under Section 368 of the Internal Revenue Code.

Transfer of qualified agricultural property when the property remains qualified agricultural property and affidavit has been filed. Transfer of qualified forest property when the property remains qualified forest property and affidavit has been filed.

Transfer of land with qualified conservation easement (land only - not improvements).

Other, as described in MCL 211.27a, specify: ____________________________________________________________________________

CERTIFICATION: I certify that the information above is true and complete to the best of my knowledge.

Name and title, if signer is other than the owner

2766, Page 2

Instructions:

This form must be filed when there is a transfer of real property or one of the following types of personal property:

•Buildings on leased land.

•Leasehold improvements, as defined in MCL Section 211.8(h).

•Leasehold estates, as defined in MCL Section 211.8(i) and (j).

Transfer of ownership means the conveyance of title to or a present interest in property, including the beneficial use of the property. For complete descriptions of qualifying transfers, please refer to MCL Section 211.27a(6)(a-j).

Excerpts from Michigan Compiled Laws (MCL), Chapter 211

**Section 211.27a(7)(d): Beginning December 31, 2014, a transfer of that portion of residential real property that had been subject to a life estate or life lease retained by the transferor resulting from expiration or termination of that life estate or life lease, if the transferee is the transferor’s or transferor’s spouse’s mother, father, brother, sister, son, daughter, adopted son, adopted daughter, grandson, or granddaughter and the residential real property is not used for any commercial purpose following the transfer. Upon request by the department of treasury or the assessor, the transferee shall furnish proof within 30 days that the transferee meets the requirements of this subdivision. If a transferee fails to comply with a request by the department of treasury or assessor under this subdivision, that transferee is subject to a fine of $200.00.

*Section 211.27a(7)(u): Beginning December 31, 2014, a transfer of residential real property if the transferee is the transferor’s or the transferor’s spouse’s mother, father, brother, sister, son, daughter, adopted son, adopted daughter, grandson, or granddaughter and the residential real property is not used for any commercial purpose following the conveyance. Upon request by the department of treasury or the assessor, the transferee shall furnish proof within 30 days that the transferee meets the requirements of this subparagraph. If a transferee fails to comply with a request by the department of treasury or assessor under this subparagraph, that transferee is subject to a fine of $200.00.

Section 211.27a(10): “... the buyer, grantee, or other transferee of the property shall notify the appropriate assessing office in the local unit of government in which the property is located of the transfer of ownership of the property within 45 days of the transfer of ownership, on a form prescribed by the state tax commission that states the parties to the transfer, the date of the transfer, the actual consideration for the transfer, and the property’s parcel identification number or legal description.”

Section 211.27(6): “Except as otherwise provided in subsection (7), the purchase price paid in a transfer of property is not the presumptive true cash value of the property transferred. In determining the true cash value of transferred property, an assessing officer shall assess that property using the same valuation method used to value all other property of that same classification in the assessing jurisdiction.”

Penalties:

Section 211.27b(1): “If the buyer, grantee, or other transferee in the immediately preceding transfer of ownership of property does not notify the appropriate assessing office as required by section 27a(10), the property’s taxable value shall be adjusted under section 27a(3) and, subject to subsection (9), all of the following must be levied:

(a)Any additional taxes that would have been levied if the transfer of ownership had been recorded as required under this act from the date of transfer.

(b)Interest and penalty from the date the tax would have been originally levied.

(c)For property classified under section 34c as either industrial real property or commercial real property, a penalty in the following amount:

(i)Except as otherwise provided in subparagraph (ii), if the sale price of the property transferred is $100,000,000.00 or less, $20.00 per day for each separate failure beginning after the 45 days have elapsed, up to a maximum of $1,000.00.

(ii)If the sale price of the property transferred is more than $100,000,000.00, $20,000.00 after the 45 days have elapsed.

(d)For real property other than real property classified under section 34c as industrial real property or commercial real property, a penalty of $5.00 per day for each separate failure beginning after the 45 days have elapsed, up to a maximum of one of the following, as applicable:

(i)For property owned and occupied as a principal residence, $200.00. As used in subparagraph, “principal residence” means that term as defined in section 7dd.

(ii)For all other property, $4000.00