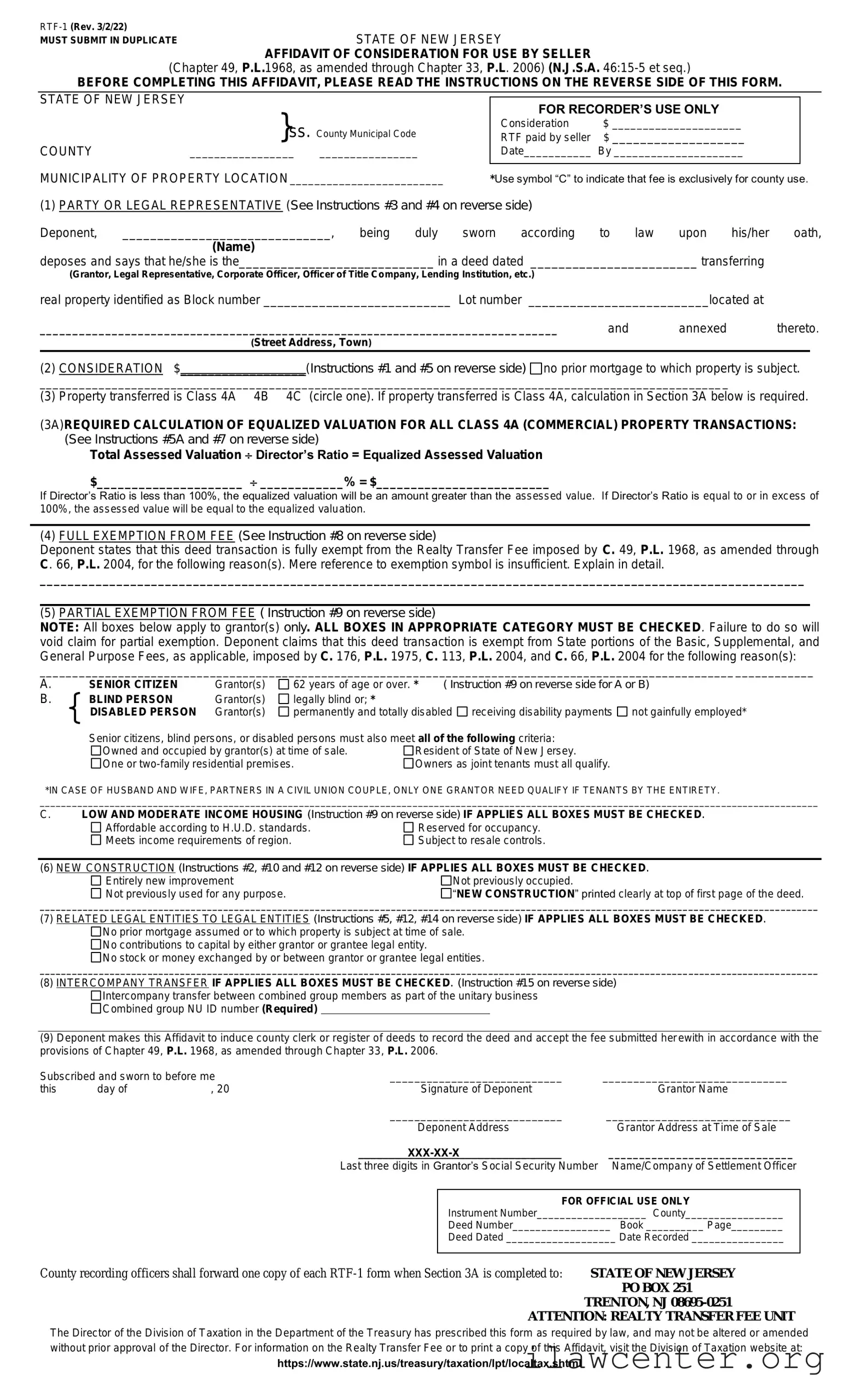

INSTRUCTIONS FOR FILING FORM RTF-1, AFFIDAVIT OF CONSIDERATION FOR USE BY SELLER

1. STATEMENT OF CONSIDERATION AND REALTY TRANSFER FEE PAYMENT ARE PREREQUISITES FOR DEED RECORDING

No county recording officer shall record any deed evidencing transfer of title to real property unless (a) the consideration is recited in the deed, or (b) an Affidavit by

one or more of the parties named in the deed or by their legal representatives declaring the consideration is annexed for recording with the deed, and (c) for

conveyances and transfers of property for which the total consideration recited in the deed is not in excess of $350,000, a fee is remitted at the rate of $2.00/$500 of

consideration or fractional part thereof not in excess of $150,000; $3.35/$500 of consideration or fractional part thereof in excess of $150,000 but not in excess of

$200,000; and $3.90/$500 of consideration or fractional part thereof in excess of $200,000. For transfers of property for which the total consideration recited in the deed

is in excess of $350,000, a fee is remitted at the rate of $2.90/$500 of consideration or fractional part not in excess of $150,000; $4.25/$500 of consideration or fractional

part thereof in excess of $150,000 but not in excess of $200,000; $4.80/$500 of consideration or fractional part thereof in excess of $200,000; $5.30/$500 of

consideration or fractional part thereof in excess of $550,000 but not in excess of $850,000; $5.80/$500 of consideration or fractional part thereof in excess of $850,00

but not in $1,000,000; and $6.05/$500 of consideration or fractional part thereof in excess of $1,000,000, which fee shall be paid in addition to the recording fees

imposed by Chapter 123, P.L. 1965, Section 2 (C. 22A:4-4.1) as amended by Chapter 370, P.L. 2001, through Chapter 66, P.L. 2004, which fee shall be paid to the

county recording officer at the time the deed is offered for recording/transfer. Of these fees, $.75/$500 of consideration or fractional part in excess of $150,000 paid to

the State Treasurer is credited to the New Jersey Affordable Housing Trust Fund.

2. WHEN AFFIDAVIT MUST BE ANNEXED TO DEED

This Affidavit must be annexed to and recorded with all deeds when entire consideration is not recited in deed or the acknowledgement or proof of the execution,

when the grantor claims a total or partial exemption from the fee, Class 4 property that includes commercial, industrial, or apartment property, and for transfers of “new

construction.” (See Instructions #10 and #12 below.)

3. LEGAL REPRESENTATIVE

“Legal representative” is to be interpreted broadly to include any person actively and responsibly participating in the transaction, such as, but not limited to: an

attorney representing one of the parties; a closing officer of a title company or lending institution participating in the transaction; a holder of power of attorney from

grantor or grantee.

4. OFFICER OF CORPORATE GRANTOR/OFFICER OF TITLE COMPANY OR LENDING INSTITUTION

Where a deponent is an officer of corporate grantor, state the name of corporation and officer’s title or where a deponent is a closing officer of a title company or

lending institution participating in the transaction, state the name of the company or institution and officer’s title.

5. CONSIDERATION

“Consideration” means in the case of any deed, the actual amount of money and the monetary value of any other thing of value constituting the entire

compensation paid or to be paid for the transfer of title to the lands, tenements or other realty, including the remaining amount of any prior mortgage to which the transfer

is subject or which is assumed and agreed to be paid by the grantee and any other lien or encumbrance not paid, satisfied or removed in connection with the transfer of

title. (C. 49, P.L. 1968, Section 1, as amended.)

5A. CLASS 4A “COMMERCIAL PROPERTIES” DEFINED

Class 4A “Commercial properties” as defined in N.J.A.C. 18:12-2.2 means “any other type of income-producing property other than property in classes 1, 2, 3A, 3B,

and those properties included in classes 4B and 4C.” A quarterly audit of all Class 4A sales submitted by the municipal assessor through the SR-1A/equalization process

will determine whether a Class 4A transaction was recorded without proper documentation and the required Affidavits of Consideration.

6. DIRECTOR'S RATIO

“Director’s Ratio” means the average ratio of assessed to true value of real property for each taxing district as determined by the Director, Division of Taxation, in

the Table of Equalized Valuations promulgated annually on or before October 1 in each year pursuant to N.J.S.A. 54:1-35.1. The Table is used in the calculation and

apportionment of distributions pursuant to the State School Aid Act of 1954.

7. EQUALIZED VALUE

“Equalized Value” means the assessed value of the property in the year that the transfer is made, divided by the Director’s Ratio. The Table of Equalized

Valuations is promulgated annually on or before October 1 in each year pursuant to N.J.S.A. 54:1-35.1.

(Example: Assessed Value = $1,000,000; Director’s Ratio = 80%. $1,000,000 .80 = $1,250,000)

8. FULL EXEMPTION FROM THE REALTY TRANSFER FEE (GRANTOR/GRANTEE)

The fee imposed by this Act shall not apply to a deed:

(a) For consideration of less than $100; (b) By or to the United States of America, this State, or any instrumentality, agency or subdivision; (c) Solely in order to provide

or release security for a debt or obligation; (d) Which confirms or corrects a deed previously recorded; (e) On a sale for delinquent taxes or assessments; (f) On partition;

(g) By a receiver, trustee in bankruptcy or liquidation, or assignee for the benefit of creditors; (h) Eligible to be recorded as an “ancient deed” pursuant to R.S. 46:16-7; (i)

Acknowledged or proved on or before July 3, 1968; (j) Between husband and wife/civil union partners, or parent and child; (k) Conveying a cemetery lot or plot; (l) In

specific performance of a final judgment; (m) Releasing a right of reversion; (n) Previously recorded in another county and full Realty Transfer Fee paid or accounted for

as evidenced by written instrument, attested to by the grantee and acknowledged by the county recording officer of the county of such prior recording, specifying the

county, book, page, date of prior recording, and amount of Realty Transfer Fee previously paid; (o) By an executor or administrator of a decedent to a devisee or heir to

effect distribution of the decedent’s estate in accordance with the provisions of the decedent’s will or the intestate laws of this State; (p) Recorded within 90 days

following the entry of a divorce/dissolution decree which dissolves the marriage/civil union partnership between grantor and grantee; (q) Issued by a cooperative

corporation, as part of a conversion of all of the assets of the cooperative corporation into a condominium, to a shareholder upon the surrender by the shareholder of all

of the shareholder’s stock in the cooperative corporation and the proprietary lease entitling the shareholder to exclusive oc cupancy of a portion of the property owned by

the corporation.

9. PARTIAL EXEMPTION FROM THE REALTY TRANSFER FEE (C. 176, P.L. 1975; C. 113, P.L. 2003; C. 66 P.L. 2004)

The following transfers of title to real property shall be exempt from State portions of the Basic Fee, Supplemental Fee, and General Purpose Fee, as applicable: 1.

The sale of any one or two-family residential premises which are owned and occupied by a senior citizen, blind person, or disabled person who is the seller in such

transaction; provided, however, that except in the instance of a husband and wife/partners in a civil union couple, no exemption shall be allowed if the property being

sold is owned as joint tenants and one or more of the owners is not a senior citizen, blind person, or disabled person; 2. The sale of Low and Moderate Income Housing

conforming to the requirements as established by this Act.

For the purposes of this Act, the following definitions shall apply:

“Blind person” means a person whose vision in his better eye with proper correction does not exceed 20/200 as measured by the Snellen chart or a person who

has a field defect in his better eye with proper correction in which the peripheral field has contracted to such an extent that the widest diameter of visual field subtends an

angular distance no greater than 20º.

“Disabled person” means any resident of this State who is permanently and totally disabled, unable to engage in gainful employment, and receiving disability

benefits or any other compensation under any federal or State law.

“Senior citizen” means any resident of this State of the age of 62 or over.

“Low and Moderate Income Housing” means any residential premises, or part thereof, affordable according to Federal Department of Housing and Urban

Development or other recognized standards for home ownership and rental costs occupied or reserved for occupancy by households with a gross income equal to 80%

or less of the median gross household income for households of the same size within the housing region in which the housing is located, but shall include only those

residential premises subject to resale controls pursuant to contractual guarantees.

“Resident of the State of New Jersey” means any claimant who is legally domiciled in this State when the transfer of the subject property is made. Domicile is what

the claimant regards as the permanent home to which he intends to return after a period of absence. Proofs of domicile include a New Jersey voter registration, motor

vehicle registration and driver’s license, and resident tax return filing.

10. TRANSFERS OF NEW CONSTRUCTION

“New construction” means any conveyance or transfer of property upon which there is an entirely new improvement not previously occupied or used for any

purpose. On transfers of new construction, the words “NEW CONSTRUCTION” shall be printed clearly at the top of the first page of the deed, and an Affidavit by the

grantor stating that the transfer is of property upon which there is new construction shall be appended to the deed.

11. REALTY TRANSFER FEE IS A FEE IN ADDITION TO OTHER RECORDING FEES

The county recording officer is required to collect the Realty Transfer Fee at the time the deed is offered for recording/transfer.

12. PENALTY FOR WILLFUL FALSIFICATION OF CONSIDERATION AND TRANSFERS OF NEW CONSTRUCTION

Any person who knowingly falsifies the consideration recited in a deed or in the proof or acknowledgement of the execution of a deed or in an affidavit annexed to a

deed declaring the consideration therefor or a declaration in an affidavit that a transfer is exempt from recording fee is guilty of a crime of the fourth degree (Chapter 308,

P.L. 1991, effective June 1, 1992). Grantors conveying title of new construction who fail to subscribe and append to the deed an affidavit to that effect in accordance with

the provisions of subsection c. of section 2 of Chapter 49, P.L. 1968 (C.46:15-6) is guilty of a disorderly persons offense. The Division of Taxation is entitled to review the

Fees collected pursuant to the State Uniform Procedure Law. The Director of the Division of Taxation is authorized to make deficiency assessments to taxpayers who

have, intentionally or mistakenly, underestimated the consideration or sales price of properties on the Affidavit of Consideration attached to deeds and upon which the

Realty Transfer Fee is based.

13. COUNTY/MUNICIPAL CODES

County/Municipal codes may be found at https://www.state.nj.us/treasury/taxation/pdf/lpt/cntycode.pdf.

14. LEGAL ENTITIES TRANSFERRING NEW JERSEY REAL ESTATE TO RELATED LEGAL ENTITIES

Legal entities transferring New Jersey real estate to related legal entities are not exempt from the Realty Transfer Fee if the consideration, as defined in the law, is

$100 or more. Such consideration includes the actual amount of money and/or the monetary value of any other thing of value constituting the entire compensation paid,

such as the dollar value of stock included in the transaction or any enhancement to or contribution to the capital or either legal entity resulting from the transfer, or

remaining balances of any prior mortgage to which the property is subject or which is assumed and agreed to be paid by the grantee and any other lien or encumbrance

not paid, satisfied or removed in connection with the transfer of title.

15. INTERCOMPANY TRANSFER BETWEEN COMBINED GROUP MEMBERS THAT FILE A NEW JERSEY COMBINED RETURN

Transfers of real property that are intercompany transfers between combined group members filing a New Jersey combined return as part of the unitary business of

the combined group are exempt from the grantor and grantee fees. Transfers must indicate the combined group NU identification number assigned by the Division of

Taxation. If the NU number has not been assigned for any reason then the RTF must be paid and a refund may be applied for.