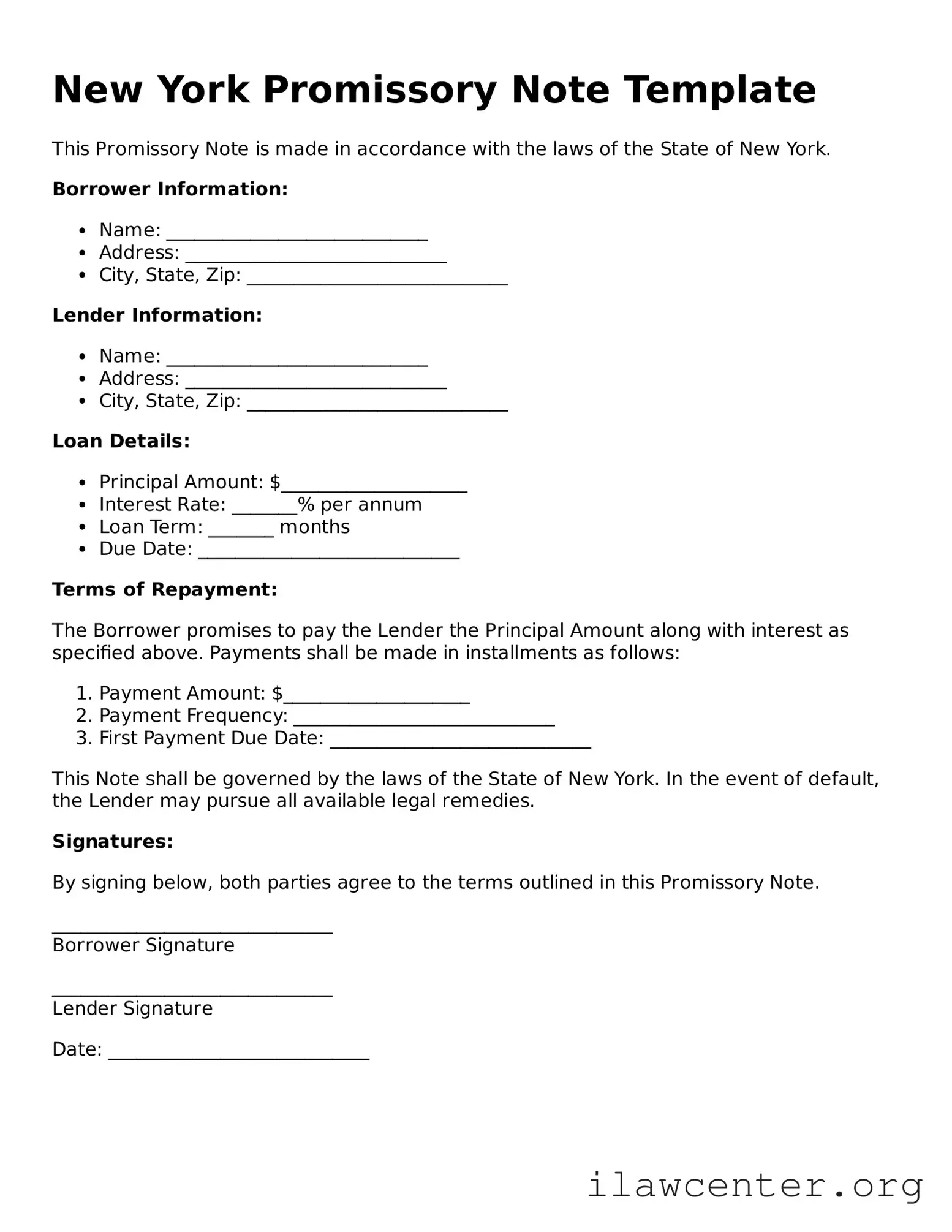

Instructions on Utilizing New York Promissory Note

After you have gathered all necessary information, you are ready to fill out the New York Promissory Note form. This document will require specific details about the loan agreement between the lender and the borrower. Follow these steps carefully to ensure accuracy.

- Title the Document: At the top of the form, write "Promissory Note." This clearly identifies the purpose of the document.

- Fill in the Date: Write the date when the note is being created. This is important for record-keeping.

- Identify the Borrower: Include the full name and address of the borrower. Make sure this information is accurate.

- Identify the Lender: Write the full name and address of the lender. Again, accuracy is key.

- State the Loan Amount: Clearly indicate the total amount of money being borrowed. Use numbers and words for clarity.

- Specify the Interest Rate: If applicable, include the interest rate for the loan. Make sure to specify whether it is fixed or variable.

- Set the Payment Terms: Outline how and when payments will be made. Include the payment frequency (e.g., monthly, quarterly) and the due date.

- Include Late Fees: If there are any late fees for missed payments, specify the amount and the conditions under which they apply.

- Signatures: Both the borrower and lender must sign the document. Include the date of each signature.

- Witness or Notary (if required): Depending on your needs, you may want to have the document witnessed or notarized. This adds an extra layer of security.

Once the form is filled out, review it carefully to ensure all information is correct. Both parties should keep a copy for their records. If you have any questions about the next steps, consider seeking advice from a professional.