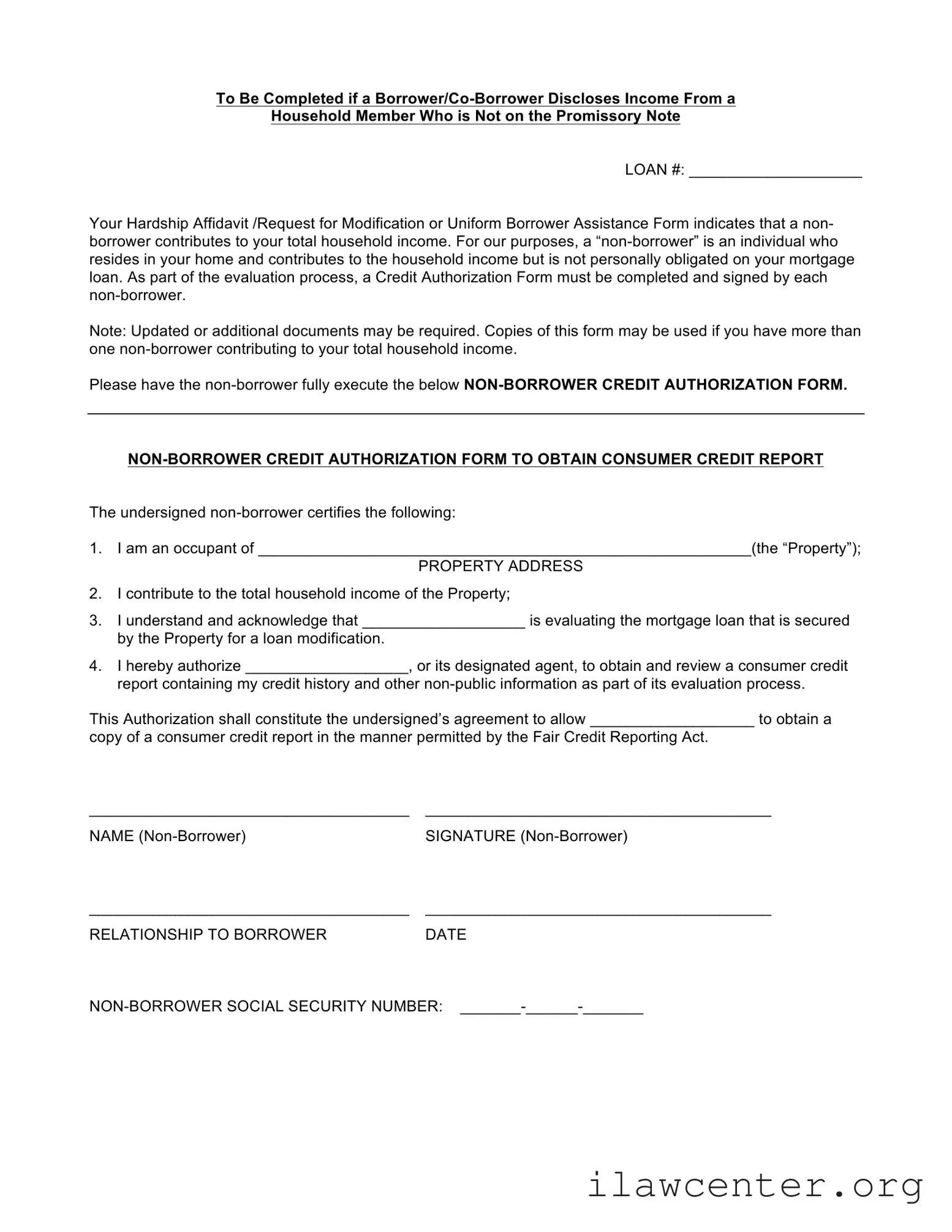

Instructions on Utilizing Non Borrower Credit Authorization

Filling out the Non Borrower Credit Authorization form is a straightforward process. Once completed, this form will help facilitate the evaluation of your mortgage loan modification. Each non-borrower must provide their information and sign the form to authorize the necessary credit checks.

- Start by writing the loan number at the top of the form in the designated space.

- Fill in the property address where the non-borrower resides.

- Confirm that the non-borrower is an occupant of the property and contributes to the total household income.

- Indicate the name of the entity evaluating the mortgage loan in the appropriate blank space.

- Have the non-borrower read the authorization statement carefully. They should understand that they are allowing the lender to obtain their consumer credit report.

- Ask the non-borrower to print their name clearly in the designated area.

- Ensure the non-borrower signs the form in the signature space provided.

- Fill in the relationship of the non-borrower to the borrower in the specified area.

- Enter the date when the non-borrower is signing the form.

- Finally, provide the non-borrower's Social Security number in the format requested.