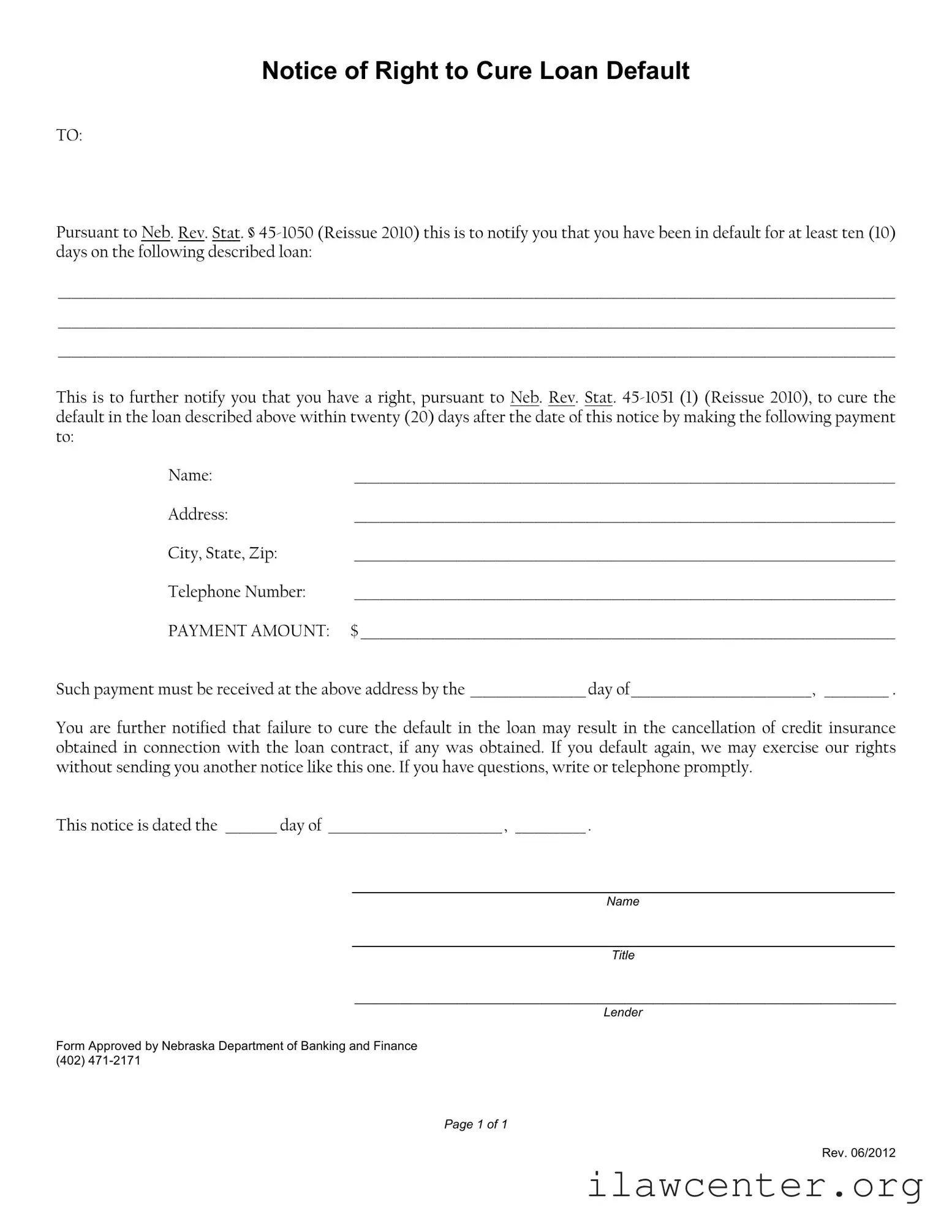

Instructions on Utilizing Notice Of Right To Cure Auto Loan Letter

Filling out the Notice of Right to Cure Auto Loan Letter is straightforward. Once completed, the form serves as an official notification regarding your loan status. Follow the steps below to ensure all necessary information is accurately provided.

- Start by entering the date at the top of the form.

- Fill in the recipient's name and address in the "TO" section.

- Describe the loan in detail, including the loan number and any relevant account information.

- In the next section, provide the lender's name, address, city, state, zip code, and telephone number.

- Specify the payment amount required to cure the default.

- Indicate the deadline for payment by writing the day, month, and year.

- Complete the date of the notice at the bottom of the form.

- Sign the form and print your name and title below the signature.

Once the form is filled out, make sure to send it to the appropriate lender address. Keep a copy for your records. If you have any questions while completing the form, don’t hesitate to reach out to the lender directly.