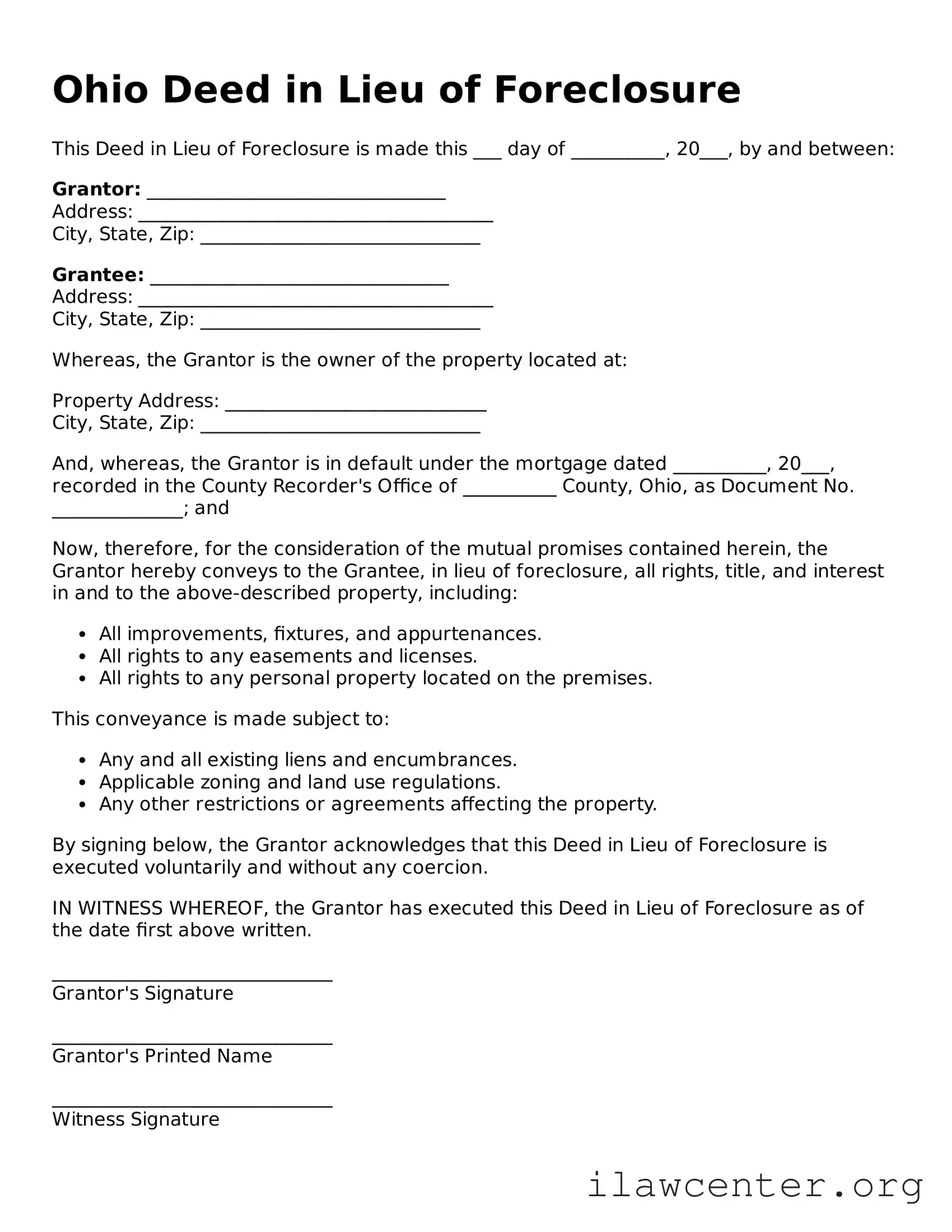

Instructions on Utilizing Ohio Deed in Lieu of Foreclosure

Completing the Ohio Deed in Lieu of Foreclosure form is a crucial step for homeowners looking to transfer their property back to the lender. After filling out the form, it will need to be submitted to the appropriate lender and recorded with the local county recorder's office. This process ensures that the deed is legally recognized and that the property ownership is officially updated.

- Begin by obtaining the Ohio Deed in Lieu of Foreclosure form from a reliable source or your lender.

- Fill in the date at the top of the form, indicating when the deed is being executed.

- Provide the name of the current property owner, ensuring that it matches the name on the original mortgage documents.

- Enter the name of the lender or mortgage holder who will receive the property.

- Include the property address, making sure to specify the street address, city, state, and ZIP code.

- Describe the property in detail, including any relevant legal descriptions or parcel numbers, if available.

- Sign the form in the designated area. The signature should be that of the current property owner.

- Have the signature notarized by a licensed notary public. This step is essential for the validity of the document.

- Make copies of the completed and notarized form for your records.

- Submit the original deed to the lender and ensure it is recorded with the local county recorder's office.