Instructions on Utilizing Ohio Promissory Note

After obtaining the Ohio Promissory Note form, you will need to provide specific information to ensure it is filled out correctly. This document will require details about the parties involved, the amount of money being borrowed, and the repayment terms. Once completed, the form should be signed by all parties to make it legally binding.

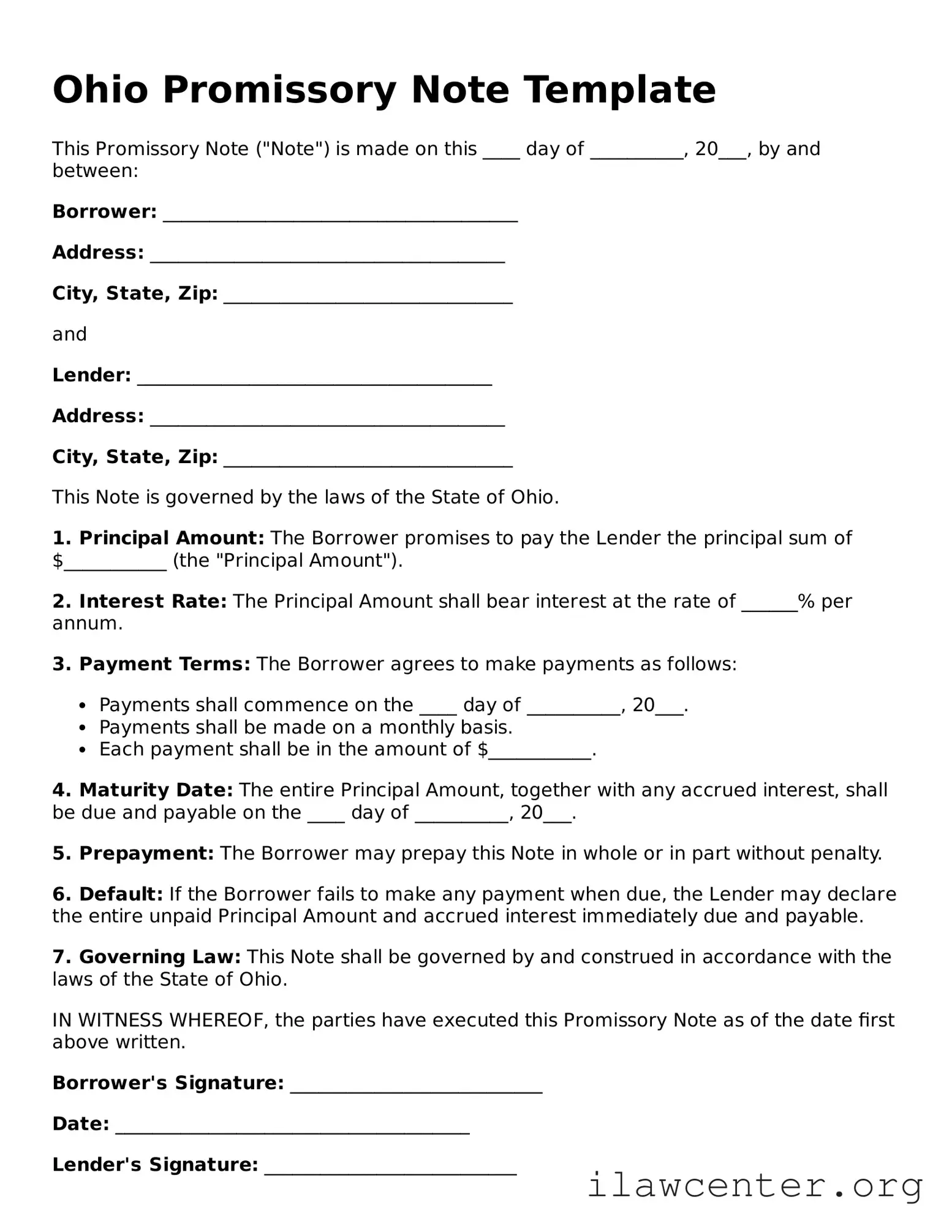

- Begin by entering the date at the top of the form.

- Identify the borrower by writing their full name and address in the designated section.

- Next, provide the lender's full name and address in the corresponding area.

- Clearly state the principal amount being borrowed. This is the total sum that the borrower agrees to repay.

- Specify the interest rate, if applicable. If there is no interest, indicate that the loan is interest-free.

- Outline the repayment terms. Include details such as the payment schedule (e.g., monthly, quarterly) and the final due date.

- If there are any late fees or penalties for missed payments, make sure to include that information.

- Provide space for both the borrower and lender to sign and date the document at the bottom.

After completing these steps, review the form for accuracy. Ensure that all information is correct and that both parties have signed it. Once confirmed, the document can be exchanged between the borrower and lender, establishing the agreement.