Instructions on Utilizing Oregon Promissory Note

After obtaining the Oregon Promissory Note form, it's essential to fill it out accurately to ensure clarity and enforceability. Follow these steps to complete the form correctly.

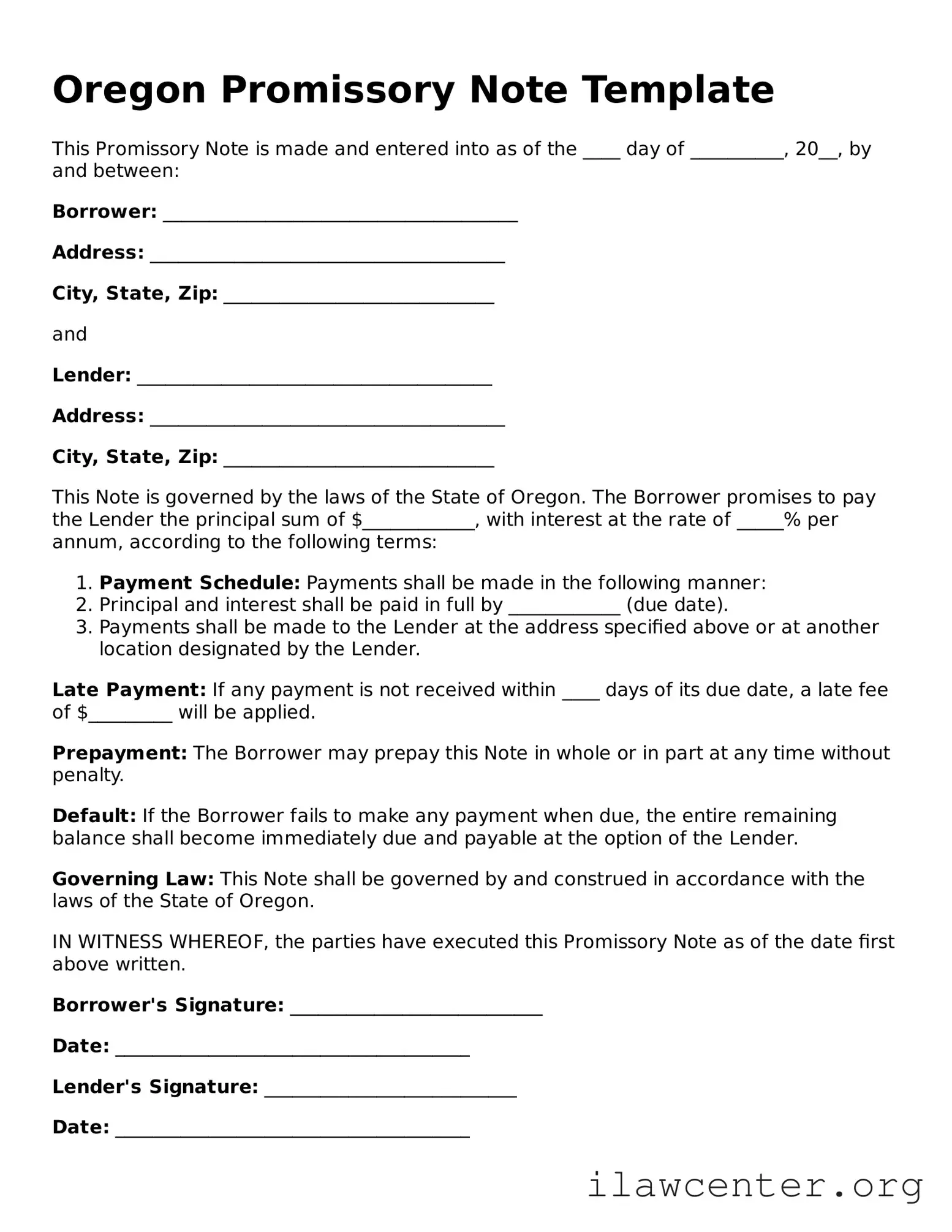

- Identify the Parties: Begin by entering the names and addresses of both the borrower and the lender at the top of the form.

- Specify the Loan Amount: Clearly state the total amount of money being borrowed. This should be written in both numbers and words to avoid any confusion.

- Set the Interest Rate: If applicable, indicate the interest rate that will be charged on the loan. Make sure to specify whether it is fixed or variable.

- Outline the Repayment Terms: Detail how and when the borrower will repay the loan. Include the payment frequency (e.g., monthly, quarterly) and the final due date.

- Include Late Fees: If there are any late fees for missed payments, specify the amount or percentage that will be charged.

- Signatures: Both the borrower and the lender must sign and date the form. This indicates that both parties agree to the terms outlined in the note.

Once the form is completed and signed, ensure that both parties keep a copy for their records. This will provide a clear reference for the terms of the loan in the future.