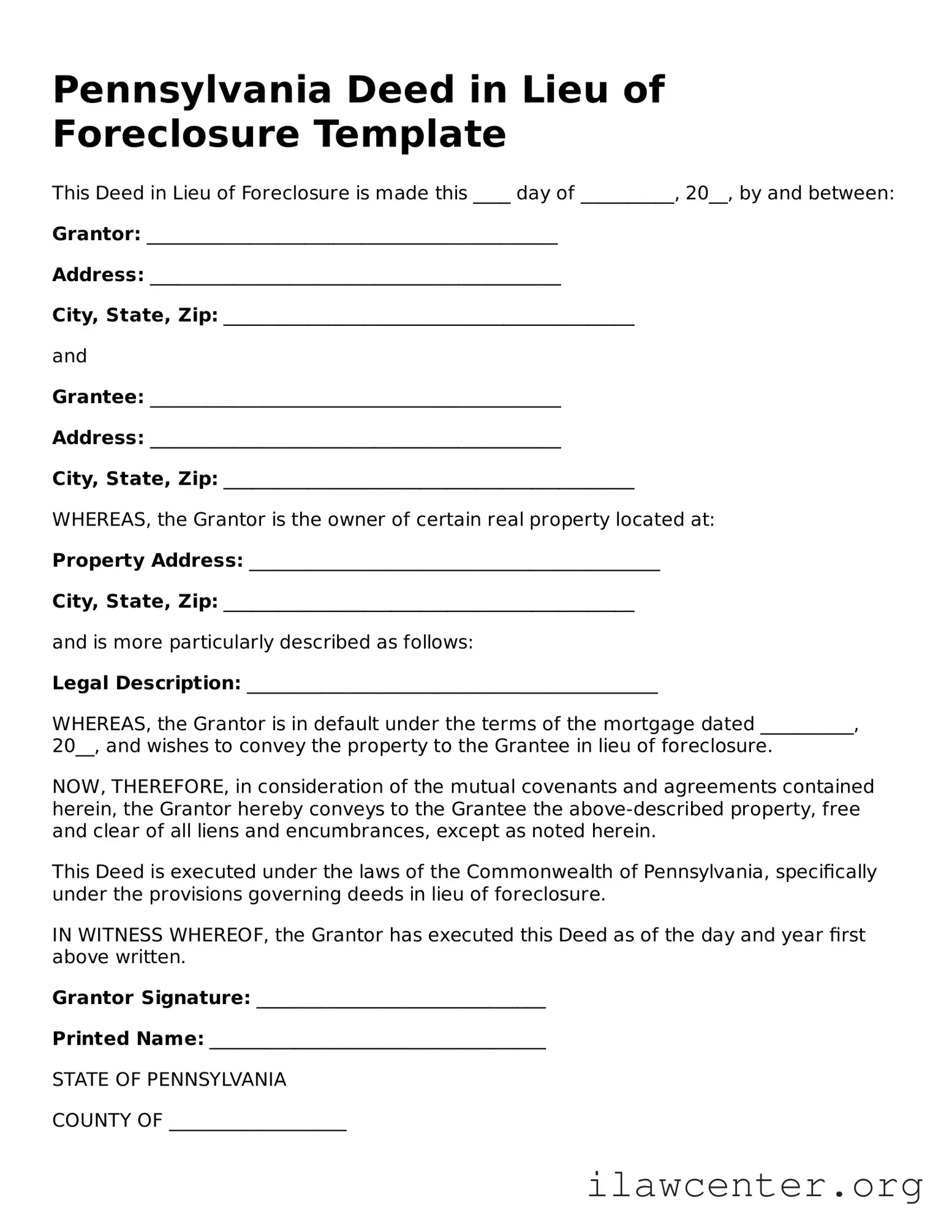

Instructions on Utilizing Pennsylvania Deed in Lieu of Foreclosure

After completing the Pennsylvania Deed in Lieu of Foreclosure form, it is essential to ensure that all parties involved understand the implications of the document. This form facilitates the transfer of property ownership to the lender, allowing the borrower to avoid foreclosure. Follow the steps below to fill out the form correctly.

- Begin by entering the date at the top of the form.

- Provide the name of the borrower as it appears on the mortgage documents.

- Fill in the address of the property being transferred.

- Include the name of the lender who will receive the property.

- Specify the legal description of the property. This is often found in the original deed.

- State the consideration for the deed, typically noted as "for no monetary consideration."

- Sign the form in the designated area. Ensure that the signature is dated.

- Have the form notarized. This step is crucial for legal validity.

- Provide a copy of the completed form to the lender and retain a copy for your records.