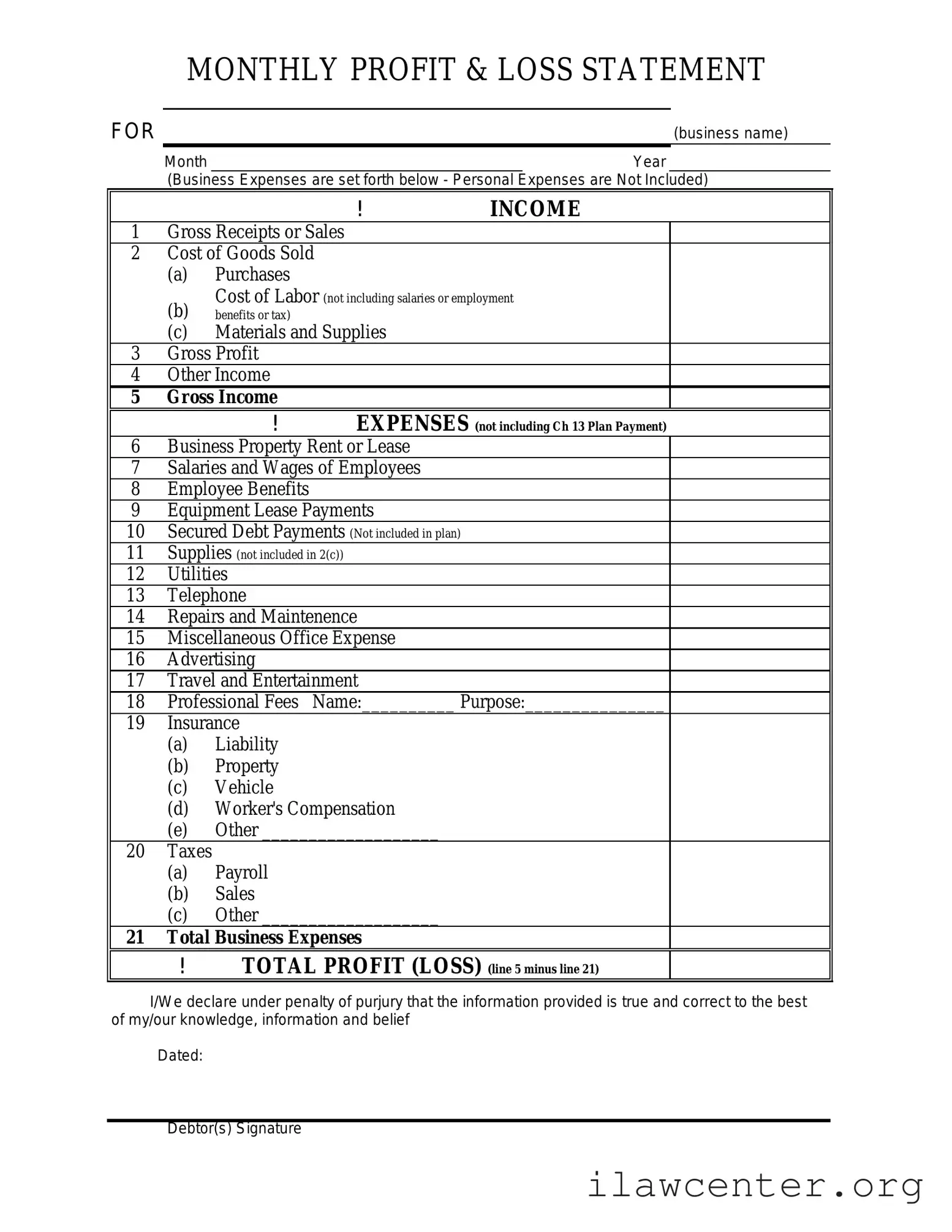

What is a Profit and Loss form?

A Profit and Loss form, also known as an income statement, is a financial document that summarizes revenues, costs, and expenses incurred during a specific period. It helps businesses assess their financial performance by showing whether they made a profit or incurred a loss during that time frame.

Why is the Profit and Loss form important?

This form is crucial for understanding a company's financial health. It provides insights into revenue generation and expense management. Business owners, investors, and stakeholders use this information to make informed decisions about operations, investments, and budgeting.

How often should a Profit and Loss form be completed?

Typically, businesses prepare a Profit and Loss form on a monthly, quarterly, or annual basis. The frequency depends on the size of the business and its financial reporting needs. Smaller businesses may find monthly reports useful, while larger organizations might focus on quarterly or annual summaries.

What information is included in a Profit and Loss form?

A Profit and Loss form generally includes several key components: total revenue, cost of goods sold (COGS), gross profit, operating expenses, and net profit or loss. Each section breaks down income and expenses to provide a clear picture of financial performance.

How do you calculate net profit from the Profit and Loss form?

To calculate net profit, subtract total expenses from total revenue. This includes all operating expenses, taxes, and interest. The resulting figure indicates whether the business has made a profit or incurred a loss during the reporting period.

Can the Profit and Loss form help with tax preparation?

Yes, the Profit and Loss form can be a valuable tool during tax season. It provides a clear overview of income and expenses, which is essential for accurate tax reporting. Business owners can use this information to determine taxable income and identify potential deductions.

Who prepares the Profit and Loss form?

The Profit and Loss form is typically prepared by the accounting department or a financial professional. However, small business owners may also complete it themselves, especially if they use accounting software that simplifies the process.

What should I do if my Profit and Loss form shows a loss?

If the Profit and Loss form shows a loss, it’s important to analyze the reasons behind it. Review revenue streams and expenses to identify areas for improvement. Consider adjusting pricing, cutting costs, or exploring new revenue opportunities to enhance financial performance in the future.