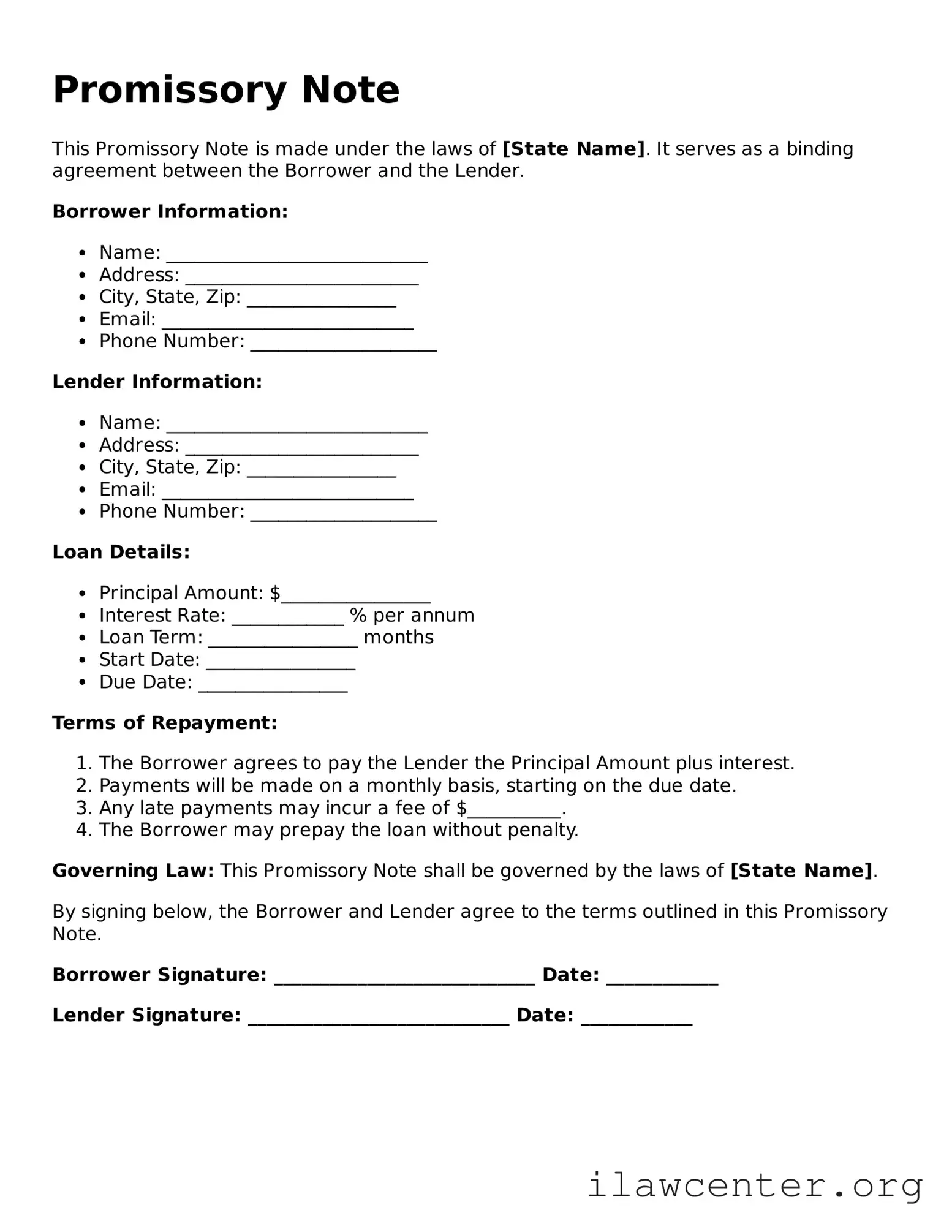

Instructions on Utilizing Promissory Note

After obtaining the Promissory Note form, it is essential to complete it accurately. This document serves as a written promise to pay a specific amount of money under agreed-upon terms. Follow these steps to ensure the form is filled out correctly.

- Begin by entering the date at the top of the form.

- Write the name of the borrower. Include the borrower's full legal name.

- Provide the borrower's address. This should be the current residential address.

- Enter the name of the lender. Use the lender's full legal name as well.

- List the lender's address. This should be the current address of the lender.

- Specify the principal amount. Clearly state the total amount of money being borrowed.

- Indicate the interest rate. Write the percentage that will be applied to the principal amount.

- Detail the repayment terms. Include the schedule for payments, such as monthly or quarterly, and the duration of the loan.

- Include any late fees. Specify the amount that will be charged if a payment is missed.

- Sign the document. The borrower must sign and date the form at the designated area.

- Have the lender sign the document. The lender must also sign and date the form.