Form ST-3 Instructions

Completing the Certicate

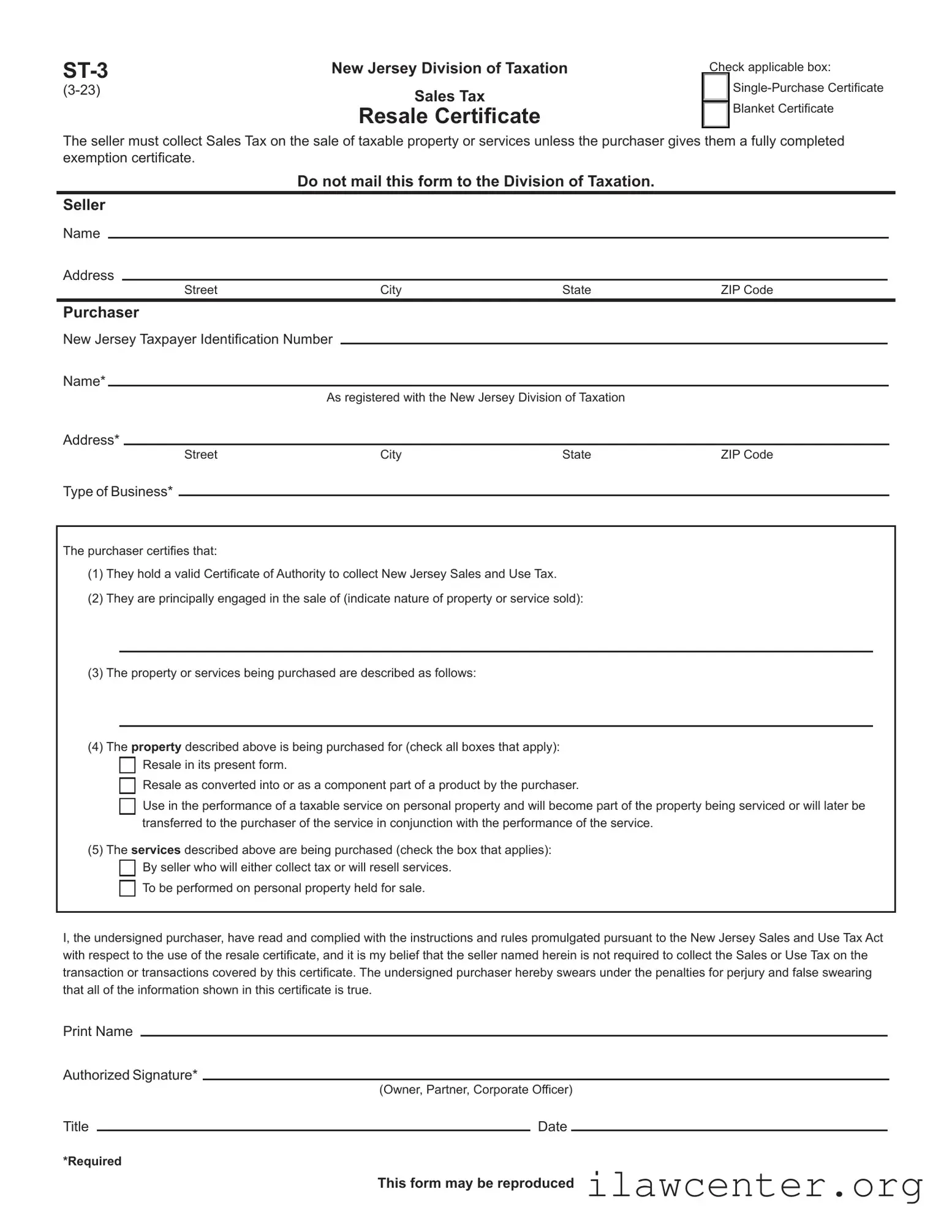

To claim an exemption from Sales Tax on the purchase of taxable property or services, the purchaser must provide a fully completed exemption cer-

ticate to the seller. Otherwise, the seller must collect the tax. The purchaser must provide the following information for the exemption certicate to be

considered fully completed:

• Name and address;

• New Jersey taxpayer identication number;

• Type of business;

• Reason(s) for exemption;

• Signature, if using a paper exemption certicate (including fax).

The seller’s name and address are not required for the exemption certicate to be considered fully completed.

Accepting the Certicate

A seller must be registered to accept an exemption certicate. The seller is relieved of liability for collecting Sales Tax on transaction(s) covered by the

certicate as long as the certicate is fully completed and is received within 90 days of the date of sale. The seller is relieved of liability even if the pur-

chaser improperly claimed the exemption, in which case the purchaser will be held liable for nonpayment of the tax.

Accepting the Certicate in an Audit Situation

If the seller either has not obtained an exemption certicate or has obtained an incomplete exemption certicate, the seller has at least 120 days after

the Division’s request for substantiation of the claimed exemption to either:

1. Obtain a fully completed exemption certicate from the purchaser taken in good faith, which in an audit situation means the exemption:

• Was statutorily available on the date of the transaction(s); and

• Could apply to the property or service being purchased; and

• Is reasonable for the purchaser’s type of business; or

2. Obtain other information establishing that the transaction(s) was not subject to tax.

If the seller obtains this information, the seller is relieved of any liability for the tax on the transaction unless it is discovered through the audit process

that the seller had knowledge or had reason to know at the time the information was provided that the information relating to the exemption claimed was

materially false or the seller otherwise knowingly participated in activity intended to purposefully evade the tax that is properly due on the transaction.

The burden is on the Division to establish that the seller had knowledge or had reason to know at the time the information was provided that the informa-

tion was materially false.

Blanket Certicates

A single exemption certicate may cover additional purchases of the same general type of property by the same purchaser with which the seller has a

recurring business relationship. For purposes of this section, a recurring business relationship exists when a period of no more than 12 months elapses

between sales transactions.

To use this form as a blanket certicate, check the applicable box at the top of the form. Each subsequent sales slip or purchase invoice based on the

blanket certicate must be clearly marked with the purchaser’s name, address, and identication number.

Retention of Certicates

Certicates must be retained by the seller for four years from the date of the last sale covered by the certicate. Certicates must be in the physical

possession of the seller and available for inspection. A seller that enters data elements from paper into an electronic format is not required to retain the

paper exemption certicate.

Examples

Proper Use of Form ST-3

1. A retail appliance store owner issues a resale certicate when purchasing appliances from a supplier for resale.

2. A furniture manufacturer issues a resale certicate when purchasing lumber to be used in manufacturing furniture for sale.

3. A service station operator issues a resale certicate when purchasing auto parts to be used in repairing customers’ cars.

Improper Use of Form ST-3

In the examples below, the seller cannot accept a resale certicate and must collect Sales Tax.

1. A lumber dealer cannot accept a resale certicate from a tire dealer that is purchasing lumber for use in altering its premises.

2. A distributor cannot issue a resale certicate on purchases of cleaning supplies and other materials for its own oce maintenance, even though it

is in the business of distributing such supplies.

3. A retailer cannot issue a resale certicate on purchases of oce equipment for its own use, even though it is in the business of selling oce

equipment.

4. A supplier cannot accept a resale certicate from a service station that purchases tools and testing equipment for use in its business.

5. A contractor cannot issue Form ST-3 for purchases of materials and supplies. If the property being worked on belongs to a qualied exempt orga-

nization, a qualied Urban Enterprise Zone business, or a qualied housing sponsor, see Contractor’s Exempt Purchase Certicate (Form ST-13)

and Contractor’s Exempt Purchase Certicate - Urban Enterprise Zone (Form UZ-4).

For more information, see S&U-6, Sales Tax Exemption Administration, which is available at www.nj.gov/treasury/taxation/pdf/pubs/sales/su6.pdf