DR-835

R. 10/11

Page 3

POWER OF ATTORNEY INSTRUCTIONS

Purpose of this form

A Power of Attorney (Form DR-835) signed by the taxpayer and the

representative is required by the Florida Department of Revenue

in order for the taxpayer’s representative to perform certain acts

on behalf of the taxpayer and to receive and inspect condential

tax information. You and your representative must complete, sign,

and return Form DR-835 if you want to grant Power of Attorney

to an attorney, certied public accountant, enrolled agent, former

Department employee, reemployment tax agent, or any other qualied

individual. A Power of Attorney is a legal document authorizing

someone other than yourself to act as your representative.

You may use this form for any matters affecting any tax administered

by the Department of Revenue. This includes both the audit and

collection processes. A Power of Attorney will remain in effect until

you revoke it. If you provide more than one Power of Attorney with

respect to a tax and tax period, the Department employee handling

your case will address notices and correspondence relative to that

issue to the rst person listed on the latest Power of Attorney.

A Power of Attorney Form is generally not required, if the

representative is, or is accompanied by: a trustee, a receiver, an

administrator, an executor of an estate, a corporate ofcer, or an

authorized employee of the taxpayer.

Photocopies and fax copies of Form DR-835 are usually acceptable.

E-mail transmissions or other types of Powers of Attorney are not

acceptable. Copies of Form DR-835 are readily available by visiting

our Internet site (www.oridarevenue.com/forms).

How to Complete Form DR-835, Power of Attorney

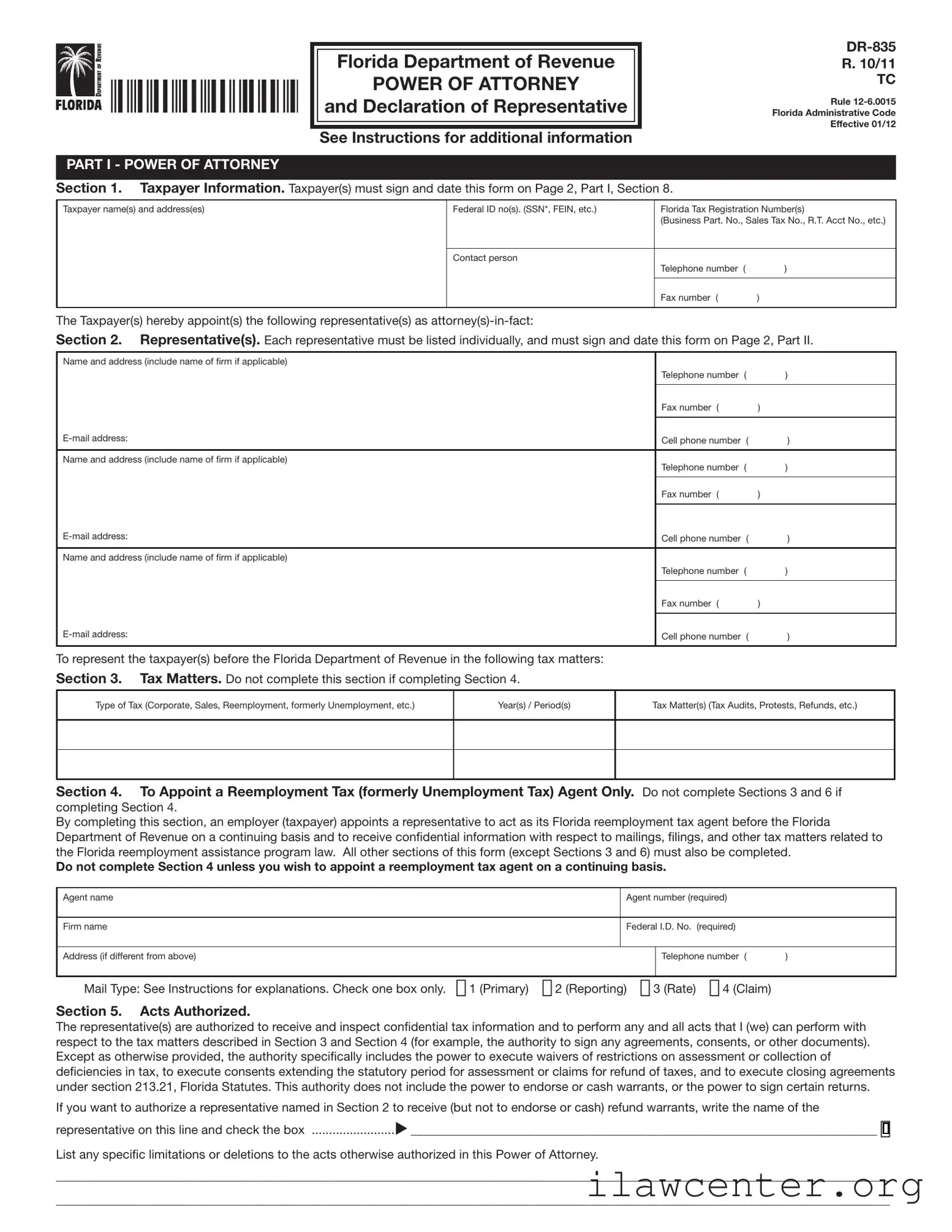

PART I POWER OF ATTORNEY

Section 1 – Taxpayer Information

• For individuals and sole proprietorships: Enter your name,

address, social security number, and telephone number(s) in the

spaces provided. Enter your federal employer identication number

(FEIN), if you have one. If a joint return is involved, and you and

your spouse are designating the same attorney(s)-in-fact, also enter

your spouse’s name and social security number, and your spouse’s

address if different from yours.

• For a corporation, limited liability company, or partnership:

Enter the name, business address, FEIN, a contact person familiar

with this matter, and telephone number(s).

• For a trust: Enter the name, title, address, and telephone

number(s) of the duciary, and name and FEIN of the trust.

• For an estate: Enter the name, title, address, and telephone

number(s) of the decedent’s personal representative, and the name

and identication number of the estate. The identication number

for an estate includes both the FEIN if the estate has one and the

decedent’s social security number.

• For any other entity: Enter the name, business address, FEIN,

and telephone number(s), as well as the name of a contact person

familiar with this matter.

• Identication Number: The Department may have assigned you

a Florida tax registration number such as a sales tax number, a

reemployment tax account number, or a business partner number.

These numbers further assist the Department in identifying your

particular tax matter, and you should enter them in the appropriate

box. If you do not provide this information, the Department may not

be able to process the Power of Attorney.

Section 2 – Representative(s)

Enter the individual name, rm name (if applicable), address,

telephone number(s), and fax number of each individual appointed as

attorney-in-fact and representative. If the representatives have the

same address, simply write “same” in the appropriate box. If you wish

to appoint more than three representatives, you should attach a letter

to Form DR-835 listing those additional individuals.

Section 3 – Tax Matters

Enter the type(s) of tax this Power of Attorney authorization applies to

and the years or periods for which the Power of Attorney is granted.

The word “All” is not specic enough. If your tax situation does not t

into a tax type or period (for example, a specic administrative appeal,

audit, or collection matter), describe it in the blank space provided

for “Tax Matters.” The Power of Attorney can be limited to specic

reporting period(s) that can be stated in year(s), quarter(s), month(s),

etc., or can be granted for an indenite period. You must indicate

the tax types, periods, and/or matters for which you are authorizing

representation by your attorney-in-fact.

Examples:

Sales and Use Tax First and second quarter 2008

Corporate Income Tax 7/1/07 – 6/30/08

Communications Services Tax 2006 thru 2008

Insurance Premium Tax 1/1/06 – 12/31/08

Technical Assistance Advisement Request dated 8/6/08

Claim for Refund 3/7/07

Section 4 – To Appoint a Reemployment Tax Agent

Complete this section only if you wish to appoint an agent for

reemployment taxes on a continuing basis. You should not complete

Section 3 or Section 6, but you must complete the remaining sections

of Form DR-835.

Enter the agent’s name. It must be the same name as found in

Section 2. Enter the rm name and address. You do not need to

complete the address line if you reported that information in Section 2.

1. Enter the agent number. The agent number is a seven-digit

number assigned by the Department of Revenue.

2. Enter the federal employer identication number. The FEIN is a

nine-digit number assigned to the agent by the Internal Revenue

Service.

3. Select the mail type.

Primary Mail. If you select primary mail, the agent will receive

all documents fr

om the Department of Revenue related to this

reemployment tax account, and will be authorized to receive

condential information and discuss matters related to the tax and

wage report, benet information, claims, and the employer’s rate.

Reporting Mail. If you select reporting mail, the agent will receive

the Employer’s Quarterly Report (Form RT-6), certication, and

correspondence related to reporting. The agent will be authorized to

receive condential information and discuss the tax and wage report,

certication, and correspondence with the Department.

Rate Mail. If you select rate mail, the agent will receive tax rate

notices and correspondence related to the rate and will be authorized

to receive condential information and discuss the employer’s rate

notices and rate with the Department.

Claims Mail. If you select claims mail, the agent will receive the

notice of benets paid, and will be authorized to receive condential

information and discuss matters related to benets.

Note: Duplicate copies of certain computer-generated notices and

other written communications cannot be issued due to current system

constraints and therefore, these communications will be sent only to

the representative.