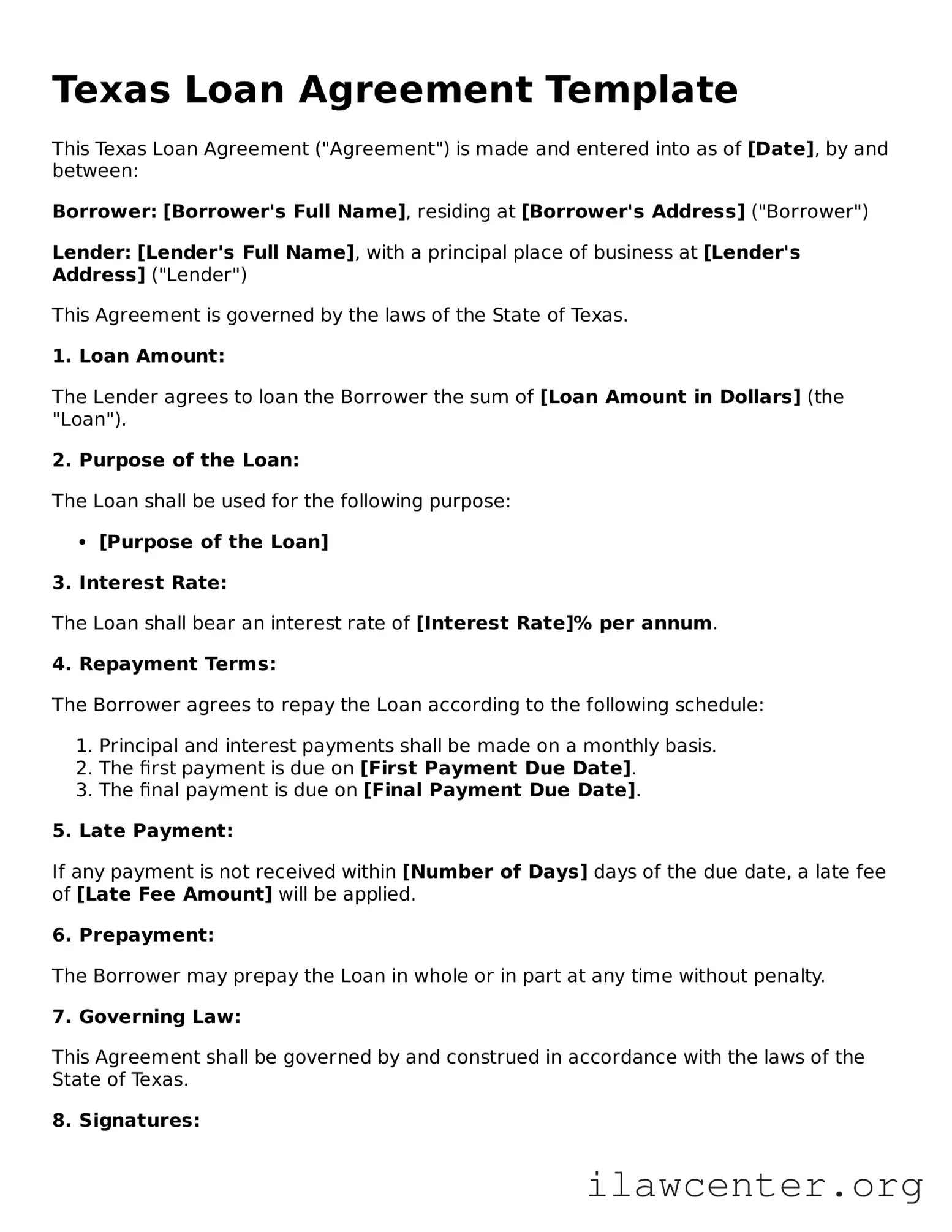

Instructions on Utilizing Texas Loan Agreement

Filling out the Texas Loan Agreement form is an important step in formalizing a loan between parties. Completing this form accurately ensures that both the lender and the borrower understand their obligations and rights. Here’s how to fill it out correctly.

- Begin by entering the date at the top of the form.

- Provide the names and addresses of both the lender and the borrower in the designated sections.

- Clearly state the loan amount in the appropriate field. Make sure this amount is accurate and reflects the agreed terms.

- Specify the interest rate, if applicable. This should be clearly noted to avoid any misunderstandings later on.

- Detail the repayment terms. Include the payment schedule, whether it’s monthly, quarterly, or another arrangement.

- Indicate any late fees or penalties for missed payments. This section helps clarify the consequences of not adhering to the repayment schedule.

- Include any collateral, if applicable. If the loan is secured by an asset, describe it in this section.

- Sign and date the agreement at the bottom. Both parties should do this to validate the agreement.

- Consider having a witness or notary public sign the document for added legal protection.

After completing the form, both parties should retain a copy for their records. This ensures that everyone has access to the agreed-upon terms in the future.