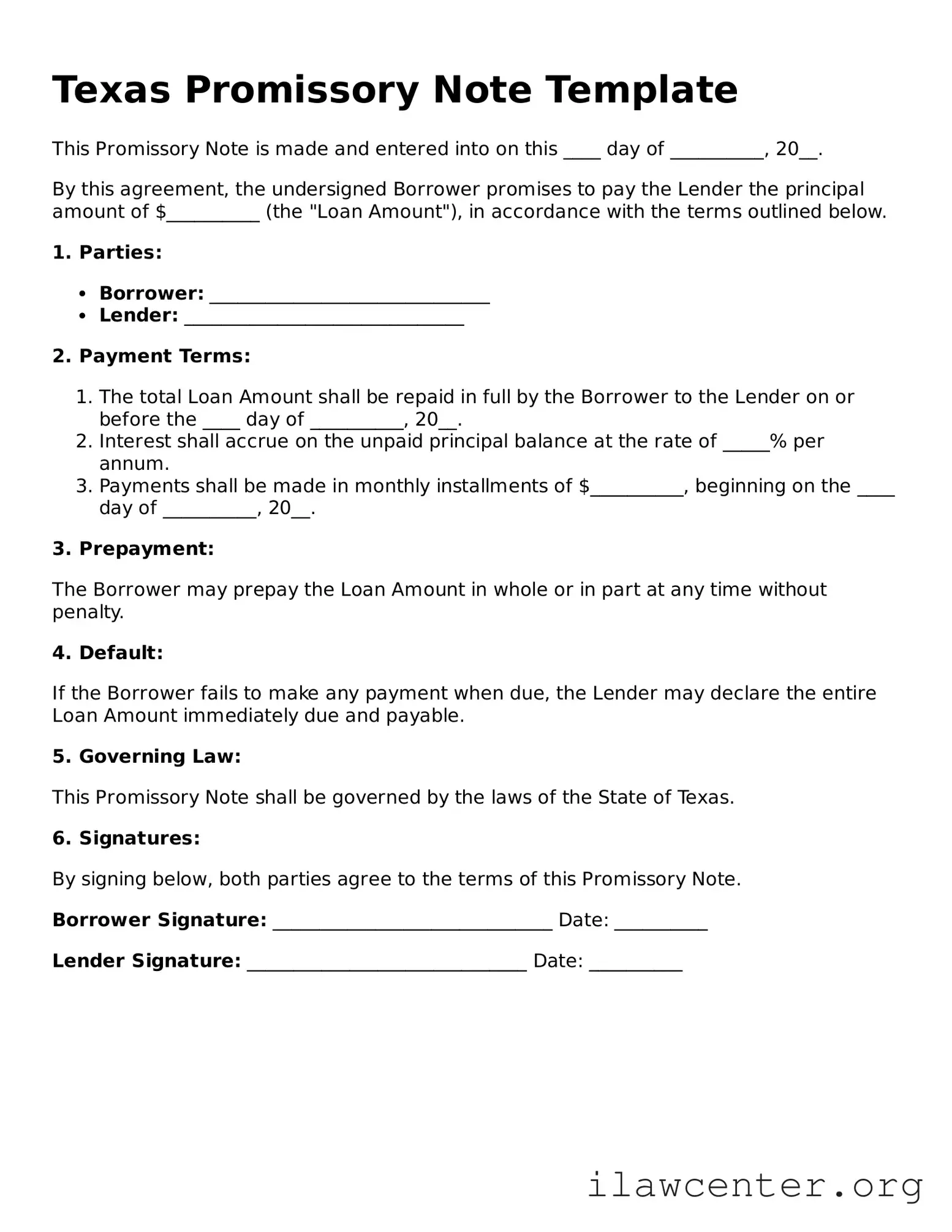

What is a Texas Promissory Note?

A Texas Promissory Note is a legal document in which one party promises to pay a specific amount of money to another party at a designated time. This note outlines the terms of the loan, including the interest rate, payment schedule, and consequences for non-payment. It serves as a written record of the borrowing agreement between the lender and the borrower.

Who can use a Texas Promissory Note?

Individuals, businesses, and organizations can utilize a Texas Promissory Note. Whether you are lending money to a friend, financing a business venture, or entering into a formal loan agreement, this document can provide clarity and legal protection for all parties involved.

What are the key components of a Texas Promissory Note?

A typical Texas Promissory Note includes several essential elements: the names and addresses of the borrower and lender, the principal amount borrowed, the interest rate, the repayment schedule, any late fees, and the signatures of both parties. Additionally, it may outline the consequences of default and any collateral involved in the loan.

Is a Texas Promissory Note legally binding?

Yes, a properly executed Texas Promissory Note is legally binding. Once signed by both parties, it creates an enforceable obligation for the borrower to repay the loan under the agreed-upon terms. However, both parties must ensure that the note complies with Texas laws to maintain its validity.

Can a Texas Promissory Note be modified?

Yes, a Texas Promissory Note can be modified if both the borrower and lender agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended note. This practice helps prevent misunderstandings and preserves the enforceability of the agreement.

What happens if the borrower defaults on the loan?

If the borrower defaults on the loan, the lender may take various actions as outlined in the promissory note. These may include charging late fees, accelerating the loan (demanding full payment), or pursuing legal action to recover the owed amount. The specific remedies available will depend on the terms of the note and applicable Texas laws.

Is notarization required for a Texas Promissory Note?

Notarization is not strictly required for a Texas Promissory Note to be enforceable. However, having the document notarized can provide an additional layer of authenticity and may be beneficial in case of a dispute. It helps establish that the signatures were made voluntarily and that the parties entered into the agreement knowingly.

Can a Texas Promissory Note be secured or unsecured?

A Texas Promissory Note can be either secured or unsecured. A secured note is backed by collateral, such as property or assets, which the lender can claim if the borrower defaults. An unsecured note does not have collateral backing it, making it riskier for the lender. The choice between secured and unsecured depends on the agreement between the parties involved.

Where can I obtain a Texas Promissory Note form?

Texas Promissory Note forms can be obtained from various sources, including legal stationery stores, online legal document providers, and attorney offices. It is crucial to ensure that the form complies with Texas laws and is tailored to your specific situation. Consulting a legal professional may provide additional guidance in selecting the appropriate document.