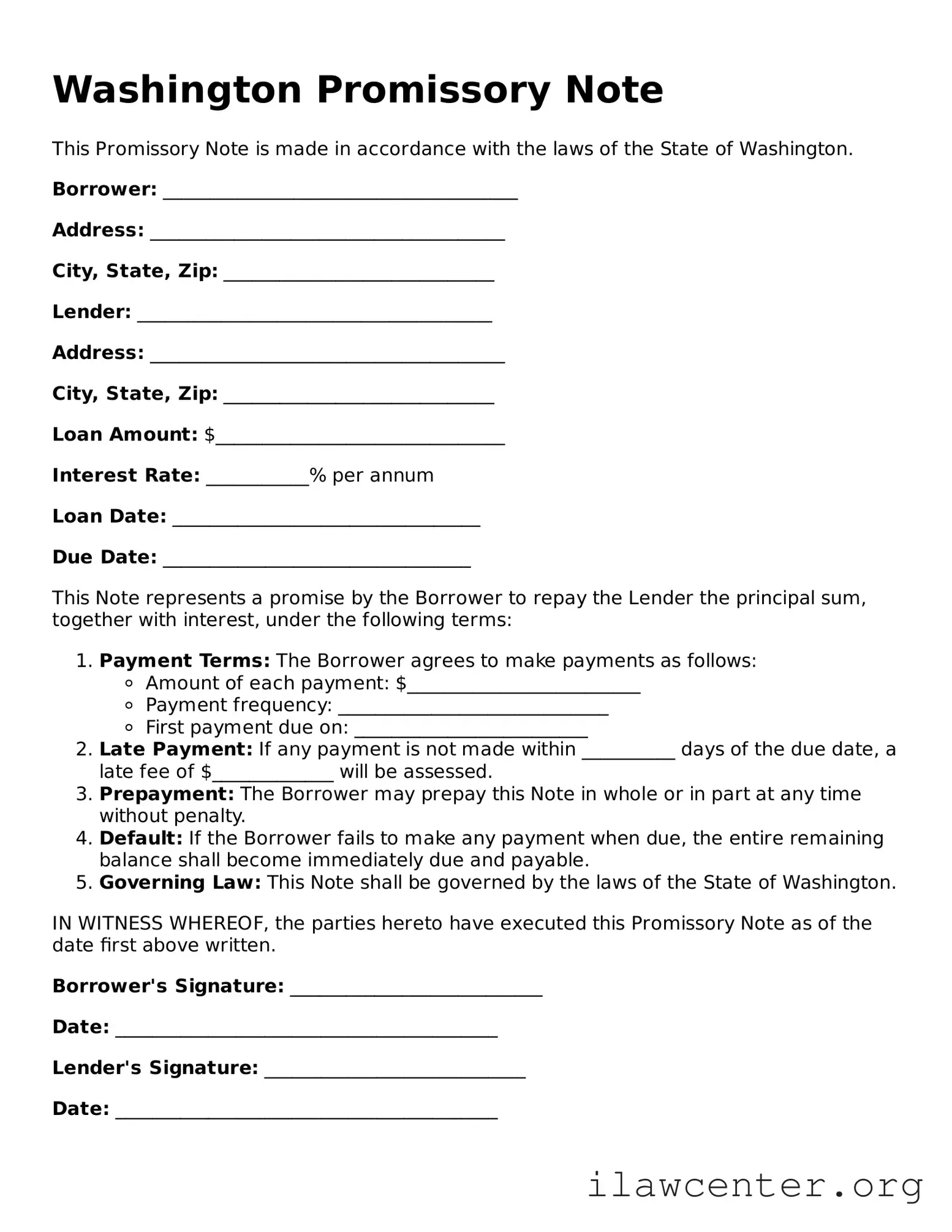

What is a Washington Promissory Note?

A Washington Promissory Note is a legal document that outlines a borrower's promise to repay a specific amount of money to a lender under agreed-upon terms. This document serves as evidence of the debt and includes details such as the loan amount, interest rate, repayment schedule, and any collateral involved.

Who can use a Promissory Note in Washington?

Any individual or business can use a Promissory Note in Washington. It is commonly used in personal loans, business loans, and real estate transactions. Both parties must agree to the terms outlined in the note for it to be enforceable.

What information should be included in a Washington Promissory Note?

A comprehensive Promissory Note should include the following information: the names and addresses of the borrower and lender, the principal amount of the loan, the interest rate, the repayment schedule, any late fees, and the signatures of both parties. Additional terms may also be included to clarify the agreement.

Is it necessary to have a Promissory Note notarized in Washington?

While notarization is not required for a Promissory Note to be legally binding in Washington, it is highly recommended. Notarization adds an extra layer of verification and can help prevent disputes regarding the authenticity of the signatures and the agreement.

What happens if the borrower defaults on the Promissory Note?

If the borrower defaults, the lender has the right to take legal action to recover the owed amount. This may include filing a lawsuit or pursuing collection efforts. The terms outlined in the Promissory Note will dictate the specific remedies available to the lender in case of default.

Can a Promissory Note be modified after it is signed?

Yes, a Promissory Note can be modified if both parties agree to the changes. It is advisable to document any modifications in writing and have both parties sign the revised agreement to ensure clarity and enforceability.

Where can I obtain a Washington Promissory Note form?

Washington Promissory Note forms can be obtained from various sources, including legal stationery stores, online legal document services, or through an attorney. Ensure that the form complies with Washington state laws to avoid any issues.